FED: Board-Bound Miran Has Signaled He'd Support Rate Cuts

Temporary Fed Board Governor-designate Miran hasn't spoken too much about monetary policy lately though today critiqued Fed participants generally for "tariff derangement syndrome" and in the past has been critical of the Fed's decision-making (though was critical of the Fed's rate cuts last year). MNI's Policy Team has interviewed him this year, and he clearly sees room for monetary easing going forward even amid what he sees as solid economic growth and broader policy-driven tailwinds for the economy.

- As had been speculated early this week, the administration may have preferred a well-qualified candidate that had already gone through the Senate confirmation process, so that a swift process to be named to the Board would be much easier to achieve - particularly important for a position that only lasts a few months.

- Though with the Senate from recess returning on Sep 2 it may be too tight for him to be confirmed before the September 16-17 meeting. It's unclear whether he Trump can appoint him to the vacancy in the interim, which doesn't appear to be possible under the Senate confirmation process in recess, but is a possibility which appears to be mentioned in the Federal Reserve Act - MNI is trying to confirm. If not, it means he would only participate in 3 FOMC meetings before his temporary term expires at end-January: Oct, Dec, and Jan.

- In June he told MNI that it's possible that the US could achieve GDP growth of 3% over the last 3 quarters of the year: "could we be running at a 3% annualized rate in the second half, or for the last three quarters of the year? It's possible. If we get the tax bill done on time, and we start making trade deals on schedule, it's very possible that we hit that rate for the for the last three quarters of the year annualized. But of course we have to wait and see that happen."

- And on inflation, he said at that time of tariffs that "there's just no evidence of any material inflationary impact". "Consumer inflation is is not only contained, it's at the lowest annual rate since March of 2021. CPI is running at a 1.5% annualized rate since the President took office. So, not only is there no evidence of that thus far, but things look pretty decent in terms of non-inflationary, strong growth. Could signs of it develop? Sure, possible. There's reasons for thinking that - there's reasons for imagining that as a possibility, but there's no evidence of it thus far. The burden of proof is on the people claiming that that could happen." He's repeated that message since our interview.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

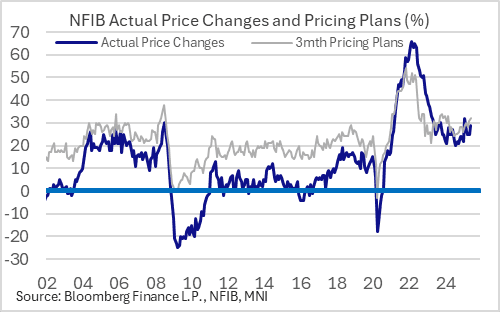

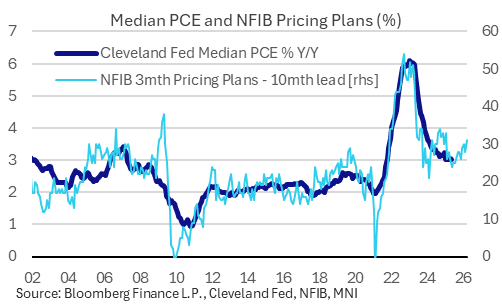

US DATA: Price Pressures Growing For Small Businesses (1/2)

The NFIB Small Business Optimism index ticked slightly lower in June (0.2pp to 98.6m exactly in line with consensus), resembling many surveys stabilizing after a tariff-related drop earlier in the year. But as usual with this report, the details were more interesting than the headline reading.

- The first standout was an increase in the main inflationary gauges which both appear to have bottomed out late last year.

- The net % raising selling prices (vs 3 months earlier) rose to 29% from 25%, the highest since February.

- And planned price increases (3-month ahead) picked up to a 15-month high net 32%, from 31% prior.

- These levels are consistent with underlying PCE inflation steadying out above 3% over the next 10 or so months (see chart).

- Small businesses are arguably under more pressure to absorb rising tariff costs than their larger corporate counterparts, so this bears watching over the coming months.

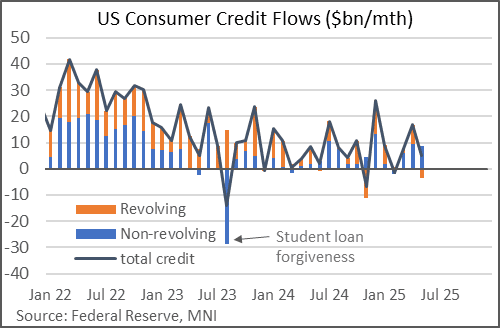

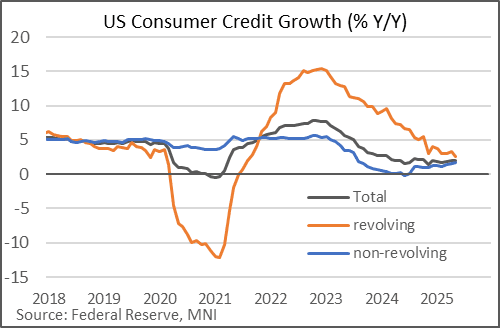

US DATA: Revolving Credit Growth Gradually Softening

Total consumer credit rose by $5.1B in May, about half of the consensus expectation and well below the $16.9B in April (downward rev from $17.9B). This was the lowest since February's $1.3B contraction.

- But the composition was also noteworthy: revolving credit (largely made up of credit cards) fell $3.5B (was +$7.5B prior), the first drop since November 2024 and only the 3rd fall in the last 17 months. Nonrevolving credit (which includes auto and student loans) flows remained strong, rising $8.6B (was +$9.4B prior).

- These series are very volatile on a month-to-month basis but broader trends are emerging. Revolving credit flows are now growing at the slowest rate (2.6% Y/Y) since August 2021, having gradually receded from double-digit growth in 2022 (which followed a sharp contraction in 2021).

- Conversely, nonrevolving growth has ticked up on that basis to 1.8% Y/Y, highest since August 2023.

- This represents a deleveraging in real terms given nominal GDP growth of 4-5% (was 4.7% in Q1). Indeed total credit outstanding remains below levels seen late last year.

- While sustained employment income gains have been the key underpinning of consumption in the last couple of years even as Covid-related government transfers have faded, slowing revolving credit growth and pickup in household savings suggests that credit may be going from a modest tailwind to something more neutral.

- That said, despite May's weakness, April's strong credit flow suggests a firmly positive credit impulse (3M/3M change vs year before), and other indicators (including the latest Dallas Fed banking and Fed Senior Loan Officer surveys) suggest consumer credit conditions are holding in.

USDCAD TECHS: Southbound

- RES 4: 1.3920 High May 21

- RES 3: 1.3862 High May 29

- RES 2: 1.3798 High Jun 23

- RES 1: 1.3690/3766 High Jul 8 / 50-day EMA

- PRICE: 1.3675 @ 16:47 BST Jul 8

- SUP 1: 1.3557 Low Jul 03

- SUP 2: 1.3540 Low Jun 16 and the bear trigger

- SUP 3: 1.3503 1.618 proj of the Feb 3 - 14 - Mar 4 price swing

- SUP 4: 1.3473 Low Oct 2 2024

Short-term gains in USDCAD are considered corrective and bears remain in the driver’s seat. Pivot resistance at the 50-day EMA, at 1.3766, is intact. A clear break of the average would signal scope for a stronger recovery. Sights are on key support and the bear trigger at 1.3540, Jun 16 low. Clearance of this level would resume the downtrend and open 1.3503, a Fibonacci projection.