FED: Bessent To Start Fed Chair Interviews On Friday - WSJ

The WSJ reported earlier that US Tsy Secretary Bessent will reportedly start Fed Chair Interviews this Friday.

- It notes: "There are 11 contenders for the job, according to Bessent and his advisers. Among them are Fed governors Christopher Waller and Michelle Bowman, National Economic Council Director Kevin Hassett and former Fed governor Kevin Warsh. Following the interviews, Bessent plans to recommend a final list of candidates to President Trump." per WSJ

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Cash Open

TYU5 is trading 112-10+, up 0-04 from its close.

- The US 2-year yield opens around 3.66%, down 0.02 from its close.

- The US 10-year yield opens around 4.206%, down 0.1 from its close.

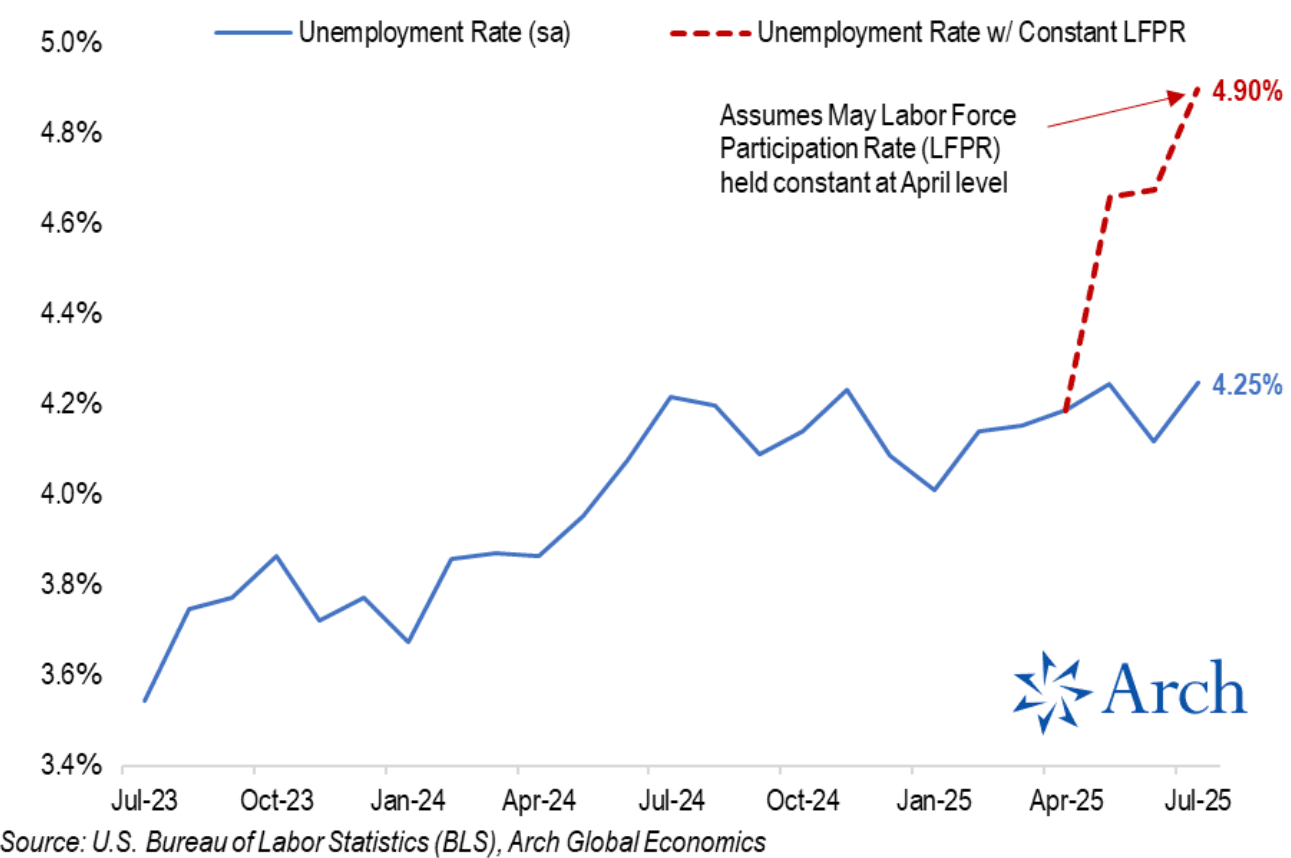

- Daily Chartbook on X: "If not for collapsing labor force participation since April, unemployment would've climbed to 4.9% [yesterday] instead of 4.25%." @Econ_Parker. See Graph Below.

- Brian Sullivan on X: “Goldman Sachs notes that the recent 2 month job revisions were the largest outside recessionary times since … 1968. Goldman expects more large revisions next month.”

- MNI BRIEF: Fed Hammack: Jobs Bear Watching, Inflation To Rise. "Disappointing signs" in the July jobs report bear careful watching, but the U.S. labor market remains largely in balance, Federal Reserve Bank of Cleveland President Beth Hammack said Friday after Bureau of Labor Statistics data showed a sharp slowdown in hiring over the past few months. "It looks like a healthy labor market that's still well in balance, but with some disappointing signs that we should watch very carefully," she told Bloomberg Television.

- The 10-year yield had a powerful move lower in reaction to the NFP data, breaking below its 4.30% pivot within the wider range 4.10% - 4.65%. This now turns momentum lower in yields and you could expect buyers of treasuries on bounces back towards 4.30/35% now looking to initially test the 4.10% area. The move was even more aggressive in the 2-year which has rejected the move back towards 4% and now looks to target the pivotal 3.50% area.

- Data/Events: Factory Orders, Durable Goods

Fig 1: US Unemployment

Source: MNI - Market News/@dailychartbook/Arch Capital

AUSTRALIA: June Consumption Growth Forecast To Rise

In a week of second tier data, the focus is likely to be on Tuesday’s June household spending data which will now replace retail sales, which had its last print last week. The Q2 chain volume measure is also out. Bloomberg consensus expects June consumption values to rise 0.8% m/m to be up 4.9% y/y after 4.2% in May. The ABS noted that discounting in the month had boosted June retail sales.

- Today, the July Melbourne Institute inflation gauge is released. It printed at 2.4% y/y in June above headline CPI at 1.9%.

- Tuesday sees the final services and composite S&P Global PMIs for July. The preliminary print saw a 2 point rise in the composite to 53.6 suggesting a pickup in growth at the start of Q3.

- June trade data are released on Thursday. The trade surplus is forecast to widen to $3.25bn from $2.24bn.

- In terms of the RBA, Head of Payments Policy Connolly participates in a panel at the ACCC/AER regulatory conference at 1045 AEST on Thursday.

JGBS: Eyeing Positive Spill Over From US Tsys, 10yr Auction Tomorrow

The Sep 10yr future finished up post Tokyo trade at 138.72, +.64 versus settlement levels. This is fresh highs back to early July for the contract, as global fixed income markets were jolted by the weaker than expected US data on Friday, led by the US NFP outcome.

- The early bias today is for higher US futures (10yr up +04), which may see further positive spill over to the JGB space. The first important resistance to watch is 141.48, the May 2 high. A break of this level would be viewed as an early bullish signal. A return lower would signal scope for an extension towards 136.57, a Fibonacci projection.

- On the data front today we just have the July monetary base figures, which won't shift market sentiment. Greater focus is likely to rest on Wednesday's June labour cash earnings figures.

- Note tomorrow also brings a 10yr bond sale.

- The 10yr JGB yield ended last week just under 1.56%, while the 10yr swap rate was at 1.285%.