EM LATAM CREDIT: Banco do Brasil: U.S. Moraes Sanctions - Neutral

(BANBRA; Ba1/BB/BB)

Major Brazil bank stocks fell yesterday due to fears of escalation in the conflict between the Brazil courts and the U.S. government over how to handle the sanction of Brasil Supreme Court justice Alexandre Moraes.

Banco do Brasil has said they will comply as always with all regulations where it is doing business and we believe that. We see broader sanctions applied in countries like Russia that invaded another country and Venezuela that has been accused of being narco traffickers and not holding democratic fair elections but Brazil is not in that same boat so talk of broader sanctions and blocking use of the SWIFT transaction system seem overblown.

Only one individual has been sanctioned but the concern is that more sanctions could be imposed on individuals and financial institutions so making it difficult for Brazil banks to conduct business in the U.S. Increasing the exposure for Banco do Brasil is that it is a government-controlled entity so any violation would be that much more severe.

We don't think this issue has legs but is more of a casualty from the ongoing political conflict between Brazil and the U.S. with President Trump showing support for beleagured ex-President Bolsonaro who is charged with engineering an attempted coup January 2023 shortly after Lula was elected President.

The U.S. government slapped Brazil imports with a 50% tariff and has so far declined efforts to negotiate despite the fact that the U.S. has a trade surplus with Brazil so the tariff has been deemed to be at least politically motivated.

We don't see much impact on senior debt of the major banks, including BANBRA. BANBRA 8.748% perps are showing some weakness, down about 1/2 point yesterday, better offered according to a market source, and down another 1/4 point today. Part of that is from the fallout from disappointing 2Q earnings resulting from persistent weakness in the agricultural loan book.

There are some questions about whether the perps will be called in October with the company saying on the 2Q earnings conference call that a decision hasn't been made yet. The bank could save on interest expense by replacing that debt with more senior debt but could they replace it with a similar junior subordinated type instrument and save anything?

With the pressure of maintaining proper capitalization given their loan book problems we think they need to keep that Tier 1 capital on their balance sheet and couldn't replace the issue at a lower coupon in the market right now, though maybe by September that could change. Also keep in mind that they need regulator approval to call the perps with 30 days notice so we will know more next month.

Its a government controlled bank with problems in its loan book that are not expected to improve going into next quarter so less likely regulators would approve calling the issue unless they could replace it with something equivalent.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GILTS: Two Gilt lines worth £21mln to be Cancelled Due to Donation

"*UK'S DEBT MANAGEMENT OFFICE TO CANCEL TWO GILTS DUE TO DONATION" - bbg

Full DMO release on that is here, it's the 4⅛% Treasury Gilt 2027 and 0⅜% Index-linked Treasury Gilt 2062 that are to be cancelled, with a £14mln and £7.8mln nominal holding per line. The cancellation is as a result of "a donation to the Donations and Bequests Account made during the financial year ending 31 March 2025": https://www.dmo.gov.uk/media/hicb4is2/sa210725.pdf

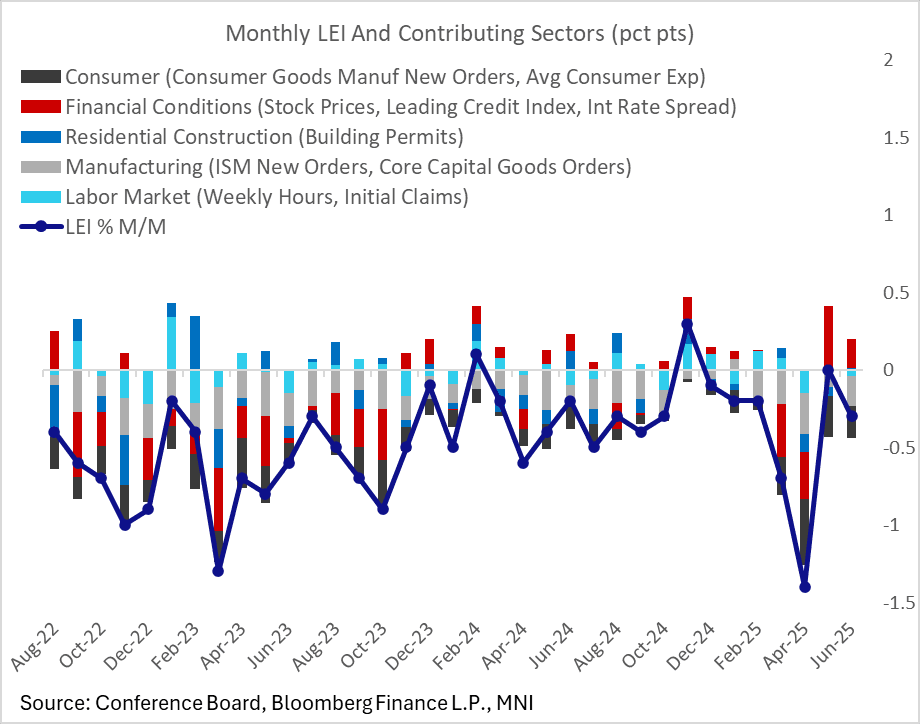

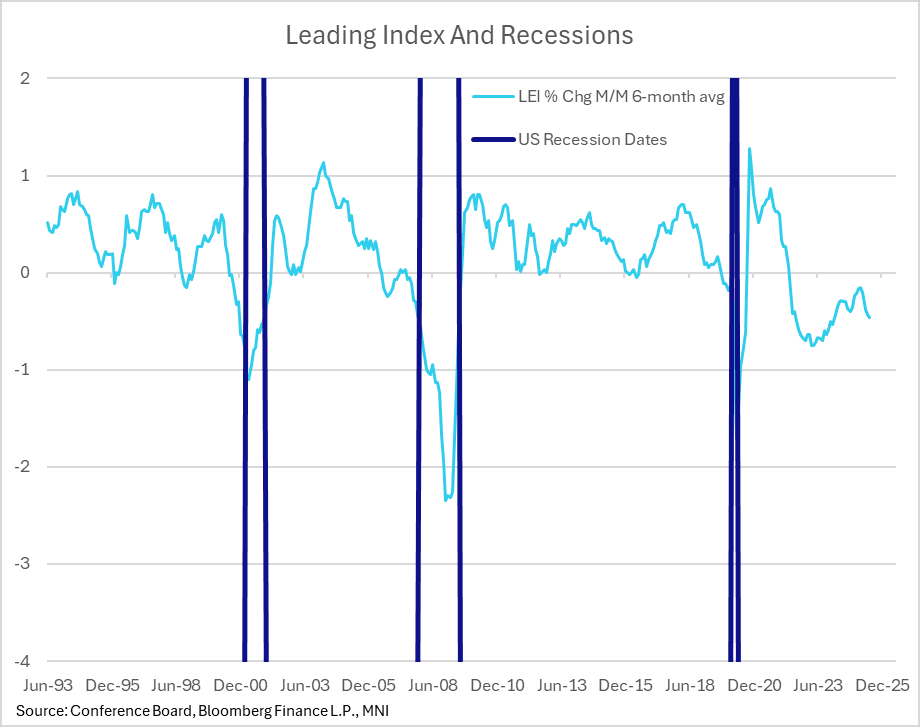

US DATA: Leading Economic Indicators Continue To Point To Weak Industrial Growth

June's Conference Board US Leading Economic Index (LEI) fell by 0.3% M/M as expected in June, pulling back from 0.0% prior (upward rev from -0.1%).

- This index has been negative the vast majority of the time for the last few years despite solid economic growth measured by GDP, so we take its signal of outright economic dynamics with some skepticism. Indeed we take the LEI mainly as a signal of manufacturing momentum as it is extremely heavily weighted toward cyclicality in manufacturing, and in this regard the pullback the last few months suggests only a limited industrial recovery over the rest of the year.

- The composition of the latest negative reading is broadly weak however: our own categorization of the LEI components point to only one positive segment: financial conditions (+0.2pp contribution) which exactly offset weaker manufacturing (-0.2pp, on ISM New Orders and Core Capital Goods orders). In turn the financial conditions reading is almost entirely stock driven by stock prices, though rate spreads and the leading credit index were both positive as well.

- From a broader economic perspective, we take note of the pullback in consumer activity in the LEI (composed of Consumer Goods Manuf New Orders, Avg Consumer Exp) which while recovering from April's extreme confidence-driven lows remains soft in part due to a tepid recovery in new orders for consumer goods.

MNI: BOC OUTLOOK SURVEY: FUTURE SALES GROWTH BALANCE OF OPINION +6

- MNI: BOC OUTLOOK SURVEY: FUTURE SALES GROWTH BALANCE OF OPINION +6

- BANK OF CANADA BUSINESS OUTLOOK SURVEY OVERALL INDICATOR -2.42

- BOC: CONSUMERS SEE INFLATION AT 3.82% NOW, 4.04% IN 1 YEAR