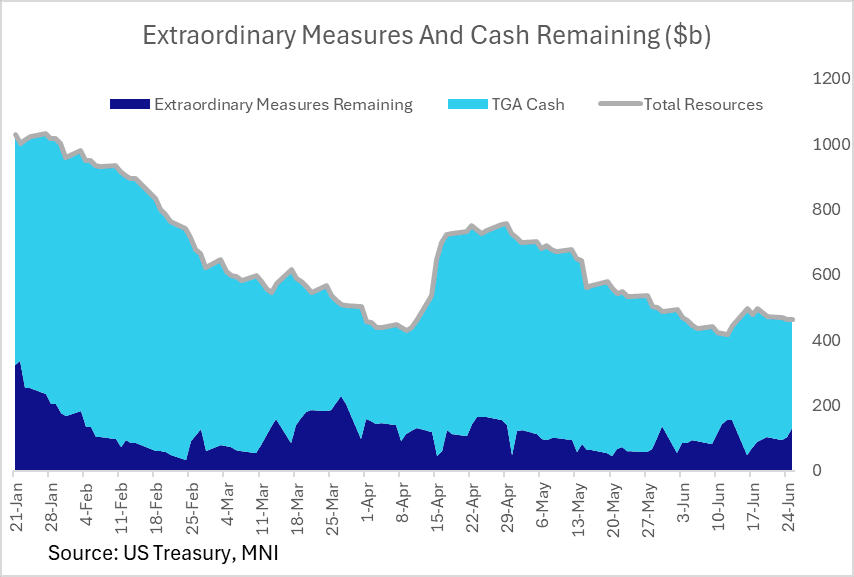

US FISCAL: Available "Extraordinary" Measures To Ward Off X-Date Pick Up

Treasury reported Friday that as of Jun 25 it had $130B in remaining "extraordinary" measures (of a total $378B available) to ward off an "x-date" of running out of resources before defaulting. That's the highest in 2 weeks.

- Combined with $334B cash as of Jun 25 (after a bit of a buildup after the mid-June tax deadline), that's a total of roughly $465B in total resources available.

- We noted earlier this week that Treasury told Congress that it was required to extend its debt issuance suspension period from Jun 27 to Jul 24, in effect prolonging the use of extraordinary measures while we await a resolution to the debt limit impasse, probably through the fiscal legislation currently going through Congress.

- Realistically, fiscal dynamics so far this year point to potential for Treasury to get into September without running out of cash + extraordinary measures. That seems to be the broad market expectation.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: US Roll Pace Update: All But Done

A final update on estimated June/Sept futures rolls which are all but complete:

- TUM/TUU - 2 Yr. . .95.3%

- FVM/FVU - 5 Yr. . .94.4%

- TYM/TYU - 10 Yr. . .91.7%

- USM/USU - 30 Yr. . .96.5%

- WNM/WNU - Ultra. . .97.7%

- UXYM/UXYU - 10Y Ultra... 92.9%

USDCAD TECHS: Trend Remains Bearish And Gains Appear Corrective

- RES 4: 1.4200 Round number resistance

- RES 3: 1.4111 High Apr 4

- RES 2: 1.3977/1.4016 50-day EMA / High May 12 and 13

- RES 1: 1.3875 20-day EMA

- PRICE: 1.3819 @ 16:47 BST May 27

- SUP 1: 1.3686 Low May 26

- SUP 2: 1.3643 Low Oct 9 ‘24

- SUP 3: 1.3579 1.500 proj of the Feb 3 - 14 - Mar 4 price swing

- SUP 4: 1.3503 1.618 proj of the Feb 3 - 14 - Mar 4 price swing

A downtrend in USDCAD remains intact and short-term gains are considered corrective. The pair has recently traded through support at 1.3751, the May 6 low. This confirmed a resumption of the downtrend and has maintained the sequence of lower lows and lower highs. Scope is seen for an extension towards the 1.3600 handle while further out, the move down opens 1.3420, the Sep 25 ‘24 low. Initial resistance is 1.3875, the 20-day EMA.

US TSYS: Modestly Weaker Having Held Key Round Levels

Cash Treasuries weakened Wednesday after three flat/positive sessions, with some light bear steepening in the cash curve.

- Treasury-negative headlines/macro developments were actually limited (a long-end Japanese bond auction went softly overnight), with yields moving lower in early trade before pushing sharply higher in late morning.

- At that point Tsys, found a bid as 30Ys touched 5.00% with 10Ys just under 4.50%. Overall, trade was mostly within Wednesday's ranges.

- The session featured a very solid 5Y Note auction, which saw a 0.4bp trade-through and a record-high takedown for 5s by indirect bidders (and one of the lowest-ever primary dealer takeups), helping yields consolidate into the close.

- The May FOMC meeting minutes cast a lightly hawkish tone in MNI's view, with little to no emphasis on the possibility of tariff-driven inflation proving to be a one-off shock. However the accounts were seen as relatively stale given developments in the last 3 weeks, and met with limited market reaction.

- In data, regional Fed surveys (Dallas services, Richmond manufacturing and services) were mixed but generally saw some stabilization in May, while Redbook retail sales continued to indicate resilient consumer activity into late May.

- Latest cash levels: 2-Yr yield is up 0.9bps at 3.9901%, 5-Yr is up 3bps at 4.0635%, 10-Yr is up 3.2bps at 4.4753%, and 30-Yr is up 2.1bps at 4.9717%.

- Note that with the Jun/Sep futures roll all but complete (all contracts 90+% through), September becomes the front contract.

- Thursday's schedule includes the 2nd reading of Q1 GDP alongside weekly jobless claims, with appearances by Fed's Barkin, Goolsbee. Kugler, and Daly.