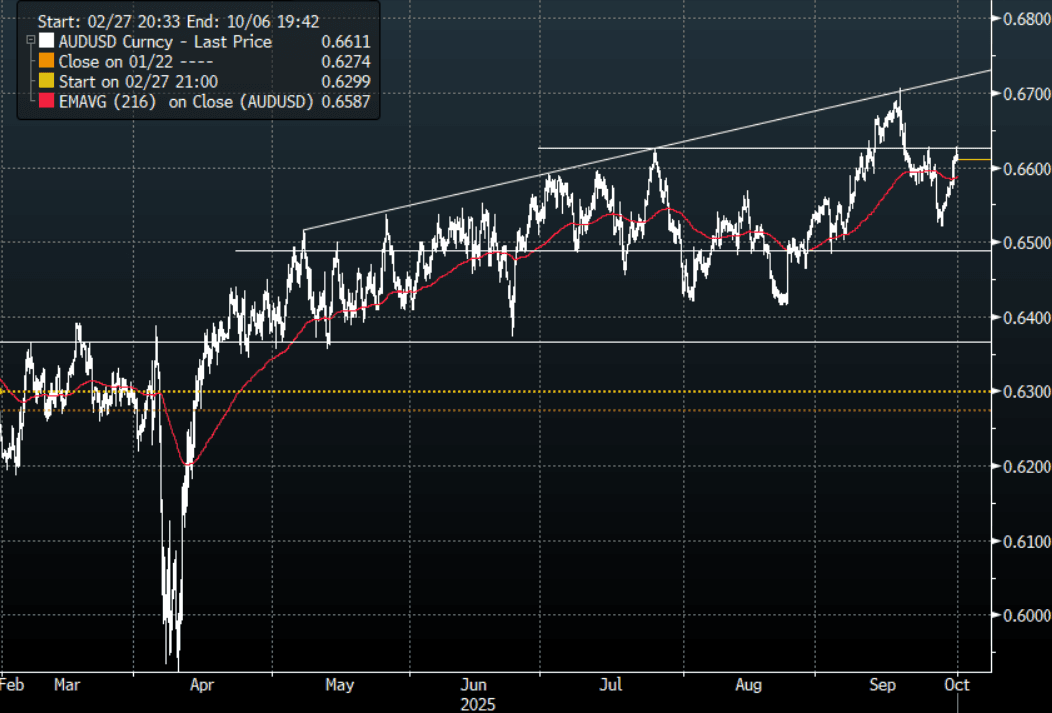

AUD: AUD/USD - Probes 0.6625, Needs The USD To Break Lower To Test 0.6700 Again

The AUD/USD had a range overnight of 0.6576-0.6629, Asia is trading around 0.6610. US stocks continue to shrug off the potential shutdown, the USD though has remained under pressure into month-end. The AUD has drifted higher in sympathy, helped by the RBA yesterday. Price action has stalled towards 0.6625 initially, the fate of the USD will determine if this move higher can gain the momentum to have another look toward the pivotal 0.6700 area. The Payrolls data this week was to be critical so should we not get it due to a shutdown the ADP print tonight could take on larger significance.

- MNI RBA WATCH: Bullock Declines To Confirm Easing Bias. Governor Michele Bullock declined to say whether the Reserve Bank of Australia retains an easing bias after the Board held the cash rate at 3.6% on Tuesday, stressing that future moves will depend on incoming data, with the current level still viewed as slightly restrictive.

- (Bloomberg) -- Australian home prices posted their strongest monthly gain in nearly two years with an expanded government incentive for first home buyers expected to further intensify buyer demand at a time of already tight supply and declining borrowing costs.

- “The Reserve Bank of Australia isn’t in a rush , and it’s not done easing, writes Bloomberg Economics. But a resilient labor market and hotter-than-expected near-term inflation reinforce our view that the easing cycle — while having much further to run — will be a very gradual and drawn-out affair.” - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6500(AUD742m), 0.6600(AUD983m), 0.6700(AUD1.64b). Upcoming Close Strikes : 0.6600(AUD1.55b Oct 3), 0.6600(AUD1.74b Oct 2), 0.6700(AUD1.06b Oct 6) - BBG

- CFTC Data last week shows Asset managers added back to their recently reduced shorts, -48580(Last -41095). The Leveraged community did likewise, -6358(Last -1519).

- Data/Event: S&P Global Australia PMI Mfg

Fig 1: AUD/USD spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

USD: Goldmans Sachs On USD Outlook - Ingredients For More Depreciation

The global bank on USD outlook, it sees ingredients for a more sustained depreciation, see below for details.

Goldman Sachs: "USD: A licking that keeps on ticking. The broad Dollar was relatively range-bound over July and August—a summer of carry, after all—but we think the forces that weighed on the Dollar in H1 are still active, and we increasingly see the required ingredients for a more sustained depreciation. We see the softening labor market as confirmation of the main thrust behind our view that the Dollar should fall further; the US is not outperforming the way it has for much of the last decade, and that warrants a weaker currency. More salient tariff effects will likely continue to weigh on US activity, and our economists expect more subpar growth ahead. Next week’s payrolls report will be an important marker to gauge the extent of the slowdown so far and the likely policy response ahead. Fed speakers have taken some understandable solace from the steady unemployment rate, and this will be the most important factor for the initial market reaction next week (we think a rise above 4.40 is likely required to meaningfully jostle rates- and recession-sensitive crosses like EUR/USD and USD/JPY). But, with the market already having moved some way to reflect this shifting outlook, we see two FX-specific developments that in our view help reinforce the Dollar downtrend. First, global asset allocators dealing with the Dollar dominance in their portfolios are likely to continue to seek ways to hedge the FX risk that has contributed a large portion of the variance in international portfolios this year. This is especially true under swirling institutional governance concerns that often have negative FX implications in part because they reduce global investor appetite. Second, we think recent CNY management changes reveal an important policy preference that has broad FX implications given the Renminbi’s important role as both a regional anchor and global benchmark. We have argued that, for Dollar depreciation to continue, it is likely that other regions will need to take the baton from the Euro, and that process now looks to be under way."

ASIA: Coming Up In Asia Pac Markets On Monday

| 2345BST | 0645HKT | 0845AEST | New Zealand July Building Permits |

| 0000BST | 0700HKT | 0900AEST | Australia Aug F S&P PMI Mfg |

| 0050BST | 0750HKT | 0950AEST | Japan Q2 Capex |

| 0100BST | 0800HKT | 1000AEST | South Korean August Trade Data |

| 0130BST | 0830HKT | 1030AEST | Japan Aug F S&P PMI Mfg |

| 0130BST | 0830HKT | 1030AEST | South Korea Aug S&P PMI Mfg |

| 0200BST | 0900HKT | 1100AEST | Australia Aug Melbourne Institute Inflation |

| 0230BST | 0930HKT | 1130AEST | Australia Q2 Company Profits |

| 0230BST | 0930HKT | 1130AEST | Australia Q2 Inventories |

| 0230BST | 0930HKT | 1130AEST | Australia July Building Approvals |

| 0230BST | 0930HKT | 1130AEST | Australia Aug ANZ-Indeed Job Ads |

| 0245BST | 0945HKT | 1145AEST | China Aug RatingDog PMI Mfg |

Source: Bloomberg Finance L.P/MNI

USDCAD TECHS: Trades Through The 50-Day EMA

- RES 4: 1.4019 38.2% retracement of the Feb 3 - Jun 16 bear leg

- RES 3: 1.3925 High Aug 22 and the bull trigger

- RES 2: 1.3868 High Aug 26

- RES 1: 1.3794 20-day EMA

- PRICE: 1.3735 @ 20:28 BST Aug 29

- SUP 1: 1.3722 Low Aug 7

- SUP 2: 1.3709 61.8% retracement of the Jul 23 - Aug 22 bull cycle

- SUP 3: 1.3658 76.4% retracement of the Jul 23 - Aug 22 bull cycle

- SUP 4: 1.3637 Low Jul 25

A bull cycle in USDCAD that started mid-June remains in play. However, the latest corrective pullback has resulted in a breach of support at the 50-day EMA, at 1.3777. A clear break of this handle signals scope for a deeper retracement and exposes 1.3722, the Aug 7 low. Moving average studies have recently crossed and are in a bull-mode position, highlighting an uptrend. The bull trigger has been defined at 1.3925, the Aug 22 high.