EM LATAM CREDIT: Argentina Next Stage of Reforms

From MNI EM Markets Analyst:

ARGENTINA: Next Stage Of Reforms Will Feature Tax Cuts, More Flexible Labour Market

• In a speech yesterday, President Milei said that the next stage of reforms after the upcoming elections will first feature a cut in taxes, followed by measures to make the labour market more flexible and to open the economy. Milei said that the sequencing of reforms is important and warned voters against choosing moderate options in the election as they will slow down change.

• Meanwhile, members of the government, including the sister of President Milei, were forced to leave a campaign march yesterday because of conflicts among protestors. The clashes between pro and anti-government groups came after the President had to abandon a campaign rally earlier this week after being attacked with stones.

• The tensions come ahead of the Buenos Aires provincial election on Sept 7, which is seen as a key indicator of the administration's support before the national midterms in October.

• In other news, the government will start increasing fuel taxes from Sept 1, according to a decree published in the official gazette. The hikes will impact both gasoline and diesel prices.

• No macro data are due today, with government tax revenue figures for August the next release in the calendar on Monday.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Early SOFR/Treasury Option Roundup

Rather mixed/two-way SOFR & Treasury option flow overnight, underlying futures mildly weaker (TYU5 -1 at 111-10.5) ahead of ADP data, FOMC annc this afternoon. Projected rate cut pricing largely steady vs. late Tuesday (*) levels: Jul'25 at -0.5bp, Sep'25 at -16.9bp, Oct'25 at -29.1bp, Dec'25 at -46.6bp (-46bp). Year end projection well off early July level of appr -65.0bp.

- SOFR Options:

- 4,300 SFRZ5 96.12 straddles ref 96.105

- 2,000 SFRU5 95.75/95.68 put spds ref 95.845

- Block/screen, 5,500 SFRV5 95.81/SFRZ5 95.62 put spds, 1.0 +Oct

- Block, +8,000 SFRV5 95.68/95.81 2x1 put spds, 1.0

- over 5,000 SFRZ5 95.62/96.87 strangles ref 96.105

- 4,000 SFRZ5 95.50/95.62/95.75 put flys, 1.5 ref 96.105 to -.11

- 2,000 0QQ5 96.93/97.06 call spds

- +1,000 SFRU5 96.12/96.25 call spds, 0.75 vs. 95.90/0.04%

- Block/screen, +12,000 SFRV5 96.12/96.25 call spds 1.0 over 95.81/95.93 put spds ref 96.105

- Treasury Options:

- +7,500 TYU5 114 calls, 5 ref 111-10

- +1,500 TYU5 111 straddles, 118 vs. 111-14.5/0.16%

- 5,450 USU5 116 calls, 49 last

- 2,500 USU5 117 calls

- 2,000 Wednesday wkly TY 110.75 puts, 1 ref 111-14, expire today, OI 12,561

- 1,200 FVU5 110.25 calls ref 108-14

- +3,000 TYX5 112/116 1x2 call spds vs. 110 puts, 5-6/call spd ovr

- over 4,200 TYU5 110.5 puts, 19 ref 111-11 to -10

- 2,000 wk1 TY 110.25/110.5 put spds, 2 ref 111-11.5 (exp 8/1)

- appr +3,000 TYU5 111.5/112.5 1x2 call spds

TARIFFS: Trump Says India Will Face Tariffs of 25% and a Penalty From Aug. 1

Trump on Truth Social: "Remember, while India is our friend, we have, over the years, done relatively little business with them because their Tariffs are far too high, among the highest in the World, and they have the most strenuous and obnoxious non-monetary Trade Barriers of any Country. Also, they have always bought a vast majority of their military equipment from Russia, and are Russia’s largest buyer of ENERGY, along with China, at a time when everyone wants Russia to STOP THE KILLING IN UKRAINE — ALL THINGS NOT GOOD! INDIA WILL THEREFORE BE PAYING A TARIFF OF 25%, PLUS A PENALTY FOR THE ABOVE, STARTING ON AUGUST FIRST. THANK YOU FOR YOUR ATTENTION TO THIS MATTER. MAGA!"

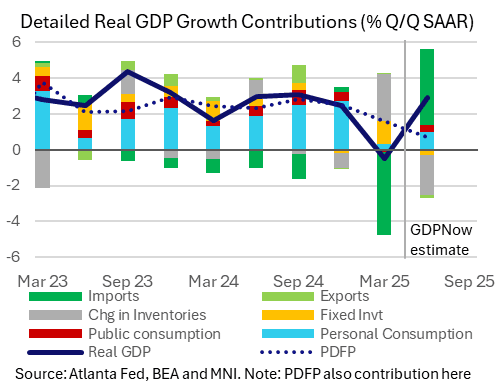

US OUTLOOK/OPINION: Q2 GDP Seen Bouncing But With Softer Private Demand (0830ET)

- Real GDP growth is seen bouncing in Q2 with Bloomberg consensus of 2.6% annualized for the flash release at 0830ET, after -0.5% in Q1 and 2.4% in Q4.

- The Atlanta Fed’s GDPNow eyes a 2.9% increase, revised higher from 2.4% tracking after yesterday’s trade and inventory data. That said, last quarter’s advance release didn’t appear to fully reflect trade data that had been captured in a then-weak GDPNow from the day beforehand, and it’s possible we see the opposite effect today.

- Starting with the more volatile components after particularly large swings in Q1, GDPNow has net exports adding 4.0pp to Q2 real GDP growth after -4.6pps in Q1, whilst changes in inventories are seen dragging -2.2pp after +2.6pps.

- For indications of underlying demand, private domestic final purchases are seen adding just 0.7pp to GDP growth after 1.6pp in Q1, for what would be the softest quarter since 4Q22.

- Within that, personal consumption is seen increasing 1.5% annualized (for a 1.0pp contribution) by both GDPNow and Bloomberg consensus.

- As for core PCE inflation, Bloomberg consensus of 2.3% annualized for Q2 after 3.5% in Q1 appears to reflect the unrounded estimates we had seen for June (averaging 0.28% M/M) ahead of tomorrow’s monthly release. Indeed, a 0.28% M/M reading with no revisions would see a 2.30% increase whilst May could have been revised up marginally judging by PPI data.