EM LATAM CREDIT: ARGENTINA: Bailout Agreement With U.S.

ARGENTINA: Economy Minister Caputo Said To Have Finalised Bailout Agreement With US

MNI Macro

• Infobae reports that after lengthy meeting this week, Economy Minister Caputo and US Treasury Secretary Bessent have finalised an agreement for the US to provide support to Argentina. The report says that if there are no last-minute changes then President Trump will announce the bailout during his meeting with President Milei at the White House on Oct 14.

• Infobae says that the bailout will revolve around the previously discussed $20bn swap which will be granted through the US’ Exchange Stabilisation Fund. The US will reportedly use $20bn of its SDRs from the IMF, which will be deposited at the Fed and transferred to the BCRA to be used as needed.

• The article says that the BCRA will then transfer the funds to the Argentinian Treasury through non-transferable bills to be used to purchase sovereign bonds to reduce country risk. It says that three banks are interested in participating.

• Meanwhile, Milei and Caputo are also expected to meet with IMF managing director Kristalina Georgieva at the IMF annual meetings next week.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

PIPELINE: Corporate Bond Update: $1.5B Raymond James 2Pt Launched

- Date $MM Issuer (Priced *, Launch #)

- 09/09 $2.5B #Repsol E&P Capital $500M 3Y +130, $1B 5Y +160, $1Y 10Y +190

- 09/09 $2.05B *NCL Corp $1.025B each: 5.25NC2 5.875%, 8NC3 6.25%

- 09/09 $2B #Turkiye Govt International Bond 10Y 7%

- 09/09 $1.5B #Raymond James $650M 10Y +85, $850M 30Y +95

- 09/09 $1B *Korea Development Bank 5Y SOFR+64

- 09/09 $750M #Huntington Bancshares PerpNC5 6.25%

- 09/09 $650M #NBN Co 5Y +60

- 09/09 $600M UWM Holdings 5.5NC2.5

- 09/09 $500M #Met Tower 5Y +65

- 09/09 $Benchmark Stellantis 3Y +145, 3Y SOFR+169, 5Y +180

- 09/09 $Benchmark DTE Energy 3Y +57, 10Y +102

- Expected Wednesday:

- 09/10 $3B KFW 3Y SOFR+33a

- 09/10 $1B Federal Home Loan 2Y +4

- 09/09 $Benchmark IDA (International Development Association) 7Y SOFR+57a

BONDS: EGBs-GILTS CASH CLOSE: Rally Takes A Breather Ahead Of ECB

European yields rose modestly Tuesday, with some of the bull flattening seen over the past week taking a breather.

- Gilt and Bund yields gapped higher on the open, but largely traded within recent ranges in the morning session. Gilts outperformed Bunds early, in part helped by a strong 20Y UK auction.

- With European data (including French industrial production and UK BRC shop sales) not proving impactful, attention was on US benchmark payroll revisions.

- The latter delivered a bigger downward revision to payrolls through Q1 2025, triggering a rally for global core FI upon release (10Y Gilt yields briefly hit a fresh post-Aug 14th low).

- But the move slowly reversed as the revision was within a broad range of analyst forecasts and attention swiftly turned to US inflation data coming Wednesday and Thursday.

- Both the German and UK curves bear steepened modestly, with periphery/EGB spreads mixed (OATs outperformed).

- The week's European focus is Thursday's ECB decision. MNI's preview went out today (here): there appears to be little to no appetite for a September rate cut amongst ECB Governing Council members but we suspect there still an underlying easing bias.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 1.5bps at 1.941%, 5-Yr is up 1.6bps at 2.225%, 10-Yr is up 1.7bps at 2.659%, and 30-Yr is up 1.6bps at 3.28%.

- UK: The 2-Yr yield is up 1.1bps at 3.914%, 5-Yr is up 1.4bps at 4.037%, 10-Yr is up 1.8bps at 4.623%, and 30-Yr is up 1.8bps at 5.477%.

- Italian BTP spread down 0.8bps at 82.1bps / French OAT down 2.6bps at 81.0bps

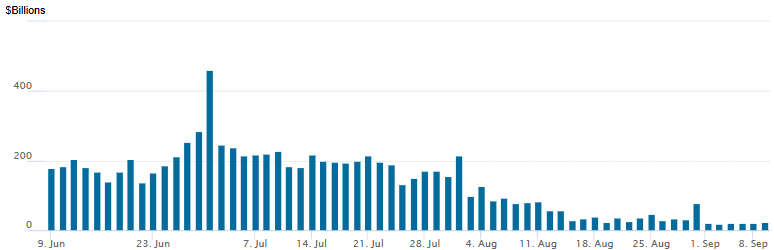

US: FED Reverse Repo Operation

RRP usage rebounds to $22.915B with 15 counterparties this afternoon from $19.416B Monday. Compares to $17.923B on Wednesday, Sep 3 - the lowest levels since early April 2021. This year's high usage of $460.731B occurred on June 30.