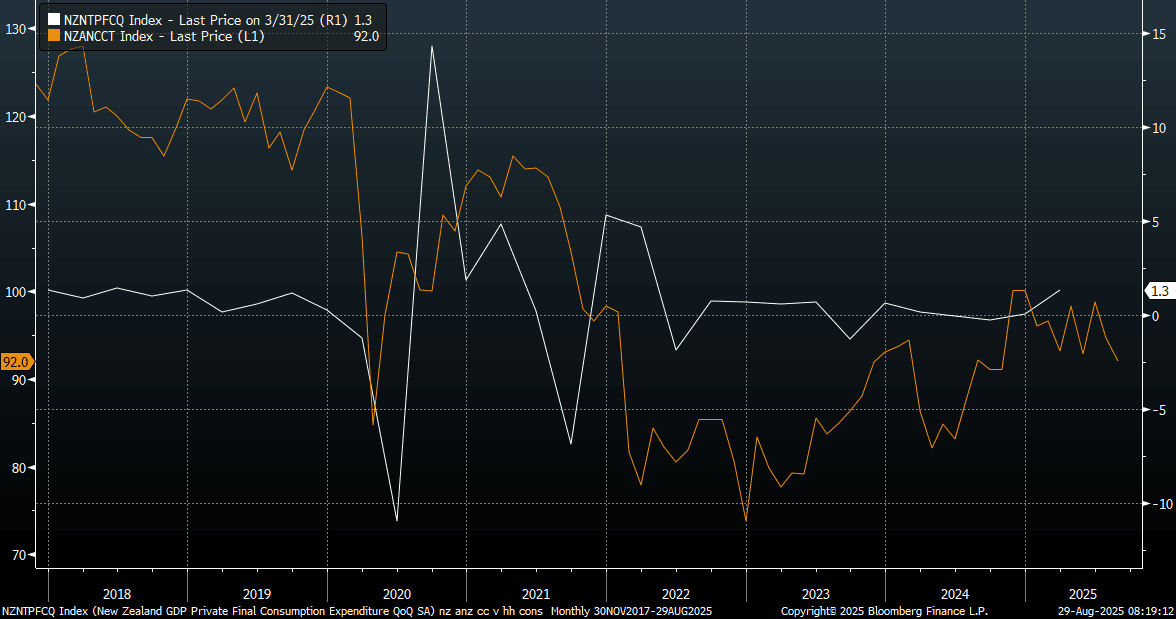

NEW ZEALAND: ANZ Consumer Confidence Measure Falters, Back To Late 2024 Levels

The ANZ August consumer confidence print fell by 2.9% to 92.0. This is back to levels from late last year. The chart below plots the headline consumer confidence measure against NZ private consumption growth from the national accounts. The current sentiment backdrop is not implying a dramatic lift in spending trends, although we have seen divergences in the past.

- Outside of the family finances year ahead outlook, all the sub categories of the index fell versus the July read. Time to buy a major household item eased to -12 from -8 prior.

- ANZ noted, via BBG: "Consumers are facing a number of headwinds which have been outweighing the positive impetus from falling real interest rates; ANZ

- “But in good news for households, the RBNZ has now pivoted to being more focused on medium-term downside risks for inflation, rather than the near-term upside risks”"

Fig 1: ANZ NZ Consumer Confidence & NZ Private Consumption Growth Q/Q

Source: ANZ/Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

NZD: NZD/USD - Consolidates Around 0.6550, Awaits FOMC

The NZD/USD had a range overnight of 0.5943 - 0.5970, Asia is trading around 0.5955. The pair found some demand around 0.5950 and has consolidated around here as we await the FOMC tomorrow morning. There is lots of event risk coming up this week that could all impact the risk backdrop significantly. Support now seen back towards the 0.5850/0.5900 area.

- MNI MACRO OUTLOOK: IMF Increases US and China Growth F'casts, But Risks To Downside. The International Monetary Fund on Tuesday boosted U.S. and China growth forecasts, citing a de-escalation of tariffs and increased fiscal stimulus while warning global growth is at risk because of trade disputes.

- "NZ'S WILLIS APPROVES KIWIBANK PARENT CO. UP TO NZ$500M RAISING" - BBG

- Bloomberg - China and the US will continue discussing the terms of a tariff truce extension, with Donald Trump making the final call, Scott Bessent said. Adding an extra 90 days from the Aug. 12 deadline is one option, he noted after two days of talks in Stockholm.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6000(NZD395m). Upcoming Close Strikes : 0.5965(NZD474m July 31). - BBG

- CFTC Data shows Asset Managers again reduced their newly built longs in NZD +5034(Last +8192), the Leveraged community added slightly to their shorts last week -7328(Last -6744).

- Data/Event : ANZ Activity Outlook & Business Confidence

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

AUSSIE 10-YEAR TECHS: (U5) Fades Through Thursday

- RES 3: 96.501 - 76.4% of the Mar 14 - Nov 1 ‘23 bear leg

- RES 2: 96.207 - 61.8% of the Mar 14 - Nov 1 ‘23 bear leg

- RES 1: 95.960 - High Apr 7

- PRICE: 95.655 @ 17:36 BST Jul 29

- SUP 1: 95.415/95.300 - Low May 15 / Low Jan 14

- SUP 2: 95.275 - Low Nov 14 (cont) and a key support

- SUP 3: 94.707 - 1.0% 10-dma envelope

Aussie 10-yr futures traded under pressure for much of last week, keeping prices subdued and within range of the recent pullback lows. Next support undercuts at 95.420 (pierced), the Feb 13 low, ahead of 95.275, the Nov 14 low and a key support. Clearance of this level would strengthen a bearish condition. To the upside, a recovery of recent losses would shift attention to resistance at 96.207, a Fibonacci retracement point.

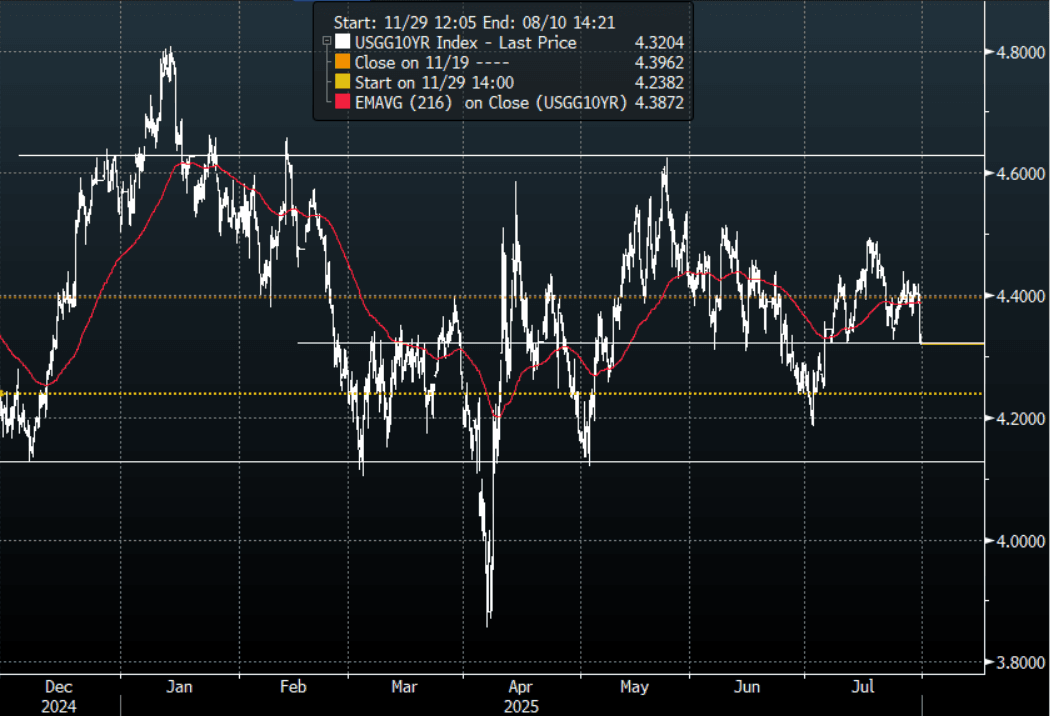

US TSYS: Yields Move Sharply Lower, Led By The Long-End

TYU5 reopens at 111-12, up 0-00+ from closing levels in today’s Asia-Pac session.

- Overnight the US 10-year yield had a range of 4.3204% - 4.4178%, closing around 4.32%.

- Treasury yields ended much lower overnight; led by the long-end causing the yield curve to flatten (2s10s -2.84 at 44.945, 5s30s -3.18 at 95.528).

- MNI US DATA: Hire Rates Extend Push Lower In A Net Dovish JOLTS Report. The JOLTS report for June was soft across the board. The ratio of openings to unemployed continued to show signs of stabilization rather than deterioration, broadly holding levels seen for the past year, but hire rates in particular cooled further. The latter leaves greater susceptibility to any slowdown in economic activity.

- (Bloomberg) - As if foreshadowing a coming increase in asset volatility, the 30-year bond declined 10 bps Tuesday in the run-up to tomorrow’s FOMC decision. The data deluge starting Wednesday could put an end to the recent market calm.

- “Trade deals are picking up, lowering worries about inflation from an extended trade war. Meanwhile, the market could be facing a squeeze due to short positioning ahead of what may be a dovish Fed meeting Wednesday, and a month-end and quarterly refunding announcement that’s likely to show no increase in long-term debt. All that acts to underpin Treasury prices.” - BBG

- The 10-year yield has moved back towards its pivot within the wider range 4.10% - 4.65%, decent supply was seen around 4.30/35% first up. A decent bounce was seen off this support but the move has failed to follow through above 4.40% for now. The Data this week should hopefully provide more clarity going forward. A Clear break of the support opens a potential move to the bottom end of the range.

Fig 1: 10-Year US Yield 120min Chart

Source: MNI - Market News/Bloomberg Finance L.P