EU TRANSPORTATION: Airlines

Jun-13 08:20

Typical for equities to fall on middle-east escalation. Re if this is sentiment or fundamental impact, likely more of the former for now;

- Fuel is ~20-30% of cost base for airlines (30-40% for low-cost carriers) and was down circa -18% over 1Q (airlines would have reported less as sustainable aviation fuel requirements kicking in). Oil has now risen +17% this month leaving but is still circa -9% y/y.

- Our commodities analyst notes thus far attacks targeted on nuclear (not Oil) facilities. He notes based on the recent past, without sustained attacks including on Oil facilities, prices generally recede from spikes.

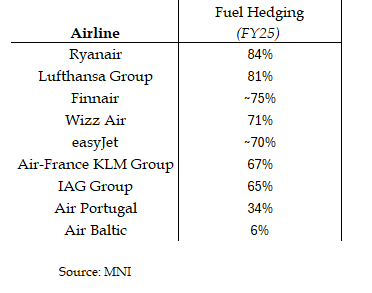

- Hedging levels are healthy in the industry; on 75% hedged and 25% of costs in fuel (typical among the larger airlines), 20% increase in fuel prices is effectively a 1.25% increase in costs or ~100bp headwind on margins.

Biggest equity movers: Wizz (-4.5%), IAG (-4%), Air-France (-4%)

Credit: Lufty/AFFP hybrids +15bps, Lufty seniors up to +5bps

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EURIBOR OPTIONS: Ratio Put Fly

May-14 08:14

ERH6 98.0625/97.9375/97.8125p fly 1x2.5x1.5p fly, bought for flat in 4.8k.

RIKSBANK: Dovish Feel To Riksbank Minutes Even If Rate Guidance Lacking

May-14 08:09

Although the Riksbank Executive Board were non-committal with respect to the timing of any future rate cuts, the lean of the May meeting minutes was dovish, perhaps more so than the policy statement portrayed.

- Although some members highlighted that the overall risks to inflation may be two-sided, the recent union wage bargaining round (Breman, Bunge, Thedeen) and stronger krona (Breman, Bunge, Jansson, Thedeen) were cited several times as inflation dampeners.

- Meanwhile, growth risks are clearly tilted to the downside. Breman highlighted Riksbank research concluding that uncertainty leads to “poorer development in the real economy”, while Jansson noted that “increased uncertainty can certainly lead to lower growth, but this will probably happen primarily via a reduction in aggregate demand, leading to falling, not rising, inflation. This is, of course, a development that is easier to manage in monetary policy, especially if inflation is already elevated at the outset”.

- Alongside tracking tariff developments and hard data, several Board members emphasised the importance of monitoring company price plans in the Economic Tendency Indicator, and the next Riksbank Business Survey.

CROSS ASSET: Bund edges to session high, Some selling emerging in the Dollar

May-14 08:05

- The German Bund has edged back towards the intraday high, after finding support at the 129.28 level (129.29 low), but the range is still a very contained 22 ticks in Low Volumes.

- Yesterday's high in Bund is at 129.71, but better resistance is seen at 129.86.

- Looking across assets, the Dollar is seeing some small selling, at session low against the EUR, GBP, TWD, CAD, NOK, SEK, MXN, ZAR and PLN, but aside from the USDJPY wider range, most G10s trade within contained ranges.