EM CREDIT SUPPLY: Affin Bank (AFFBNK, A3/NR/NR) - FV Estimate

"*IPT: AFFIN BANK BERHAD 5Y $BMARK REG S BOND, T+135BP AREA" - BBG

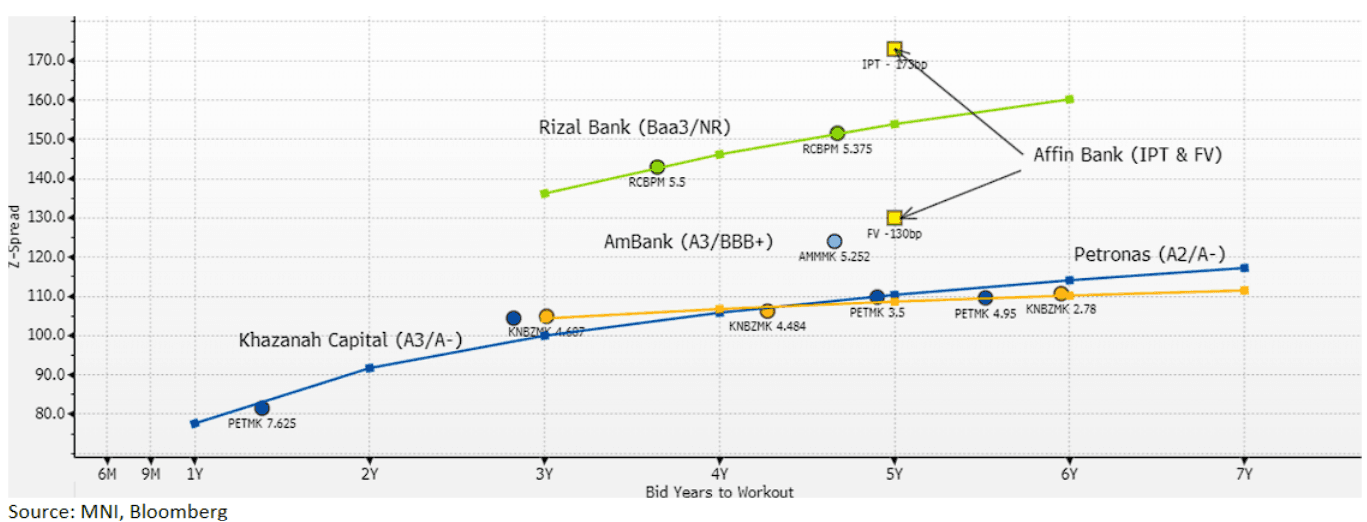

New Issue: $benchmark 5y

IPT: T+135bp area (c. z+173bp)

FV: T+92bp (c. z+130bp)

• Malaysian bank, Affin Bank, which is 31% owned by the State of Sarawak, has come to the market with a new $benchmark 5y deal.

• The Moody's A3 rating notes that asset quality and capital adequacy are relatively good. Profitability is low, but the banks standalone rating (Baa3) is boosted 3 notches due to the likely support of the State of Sarawak (A3 stable) if needed.

• The company reported Q1 results recently, with net income +8% YoY to RM544m and a net interest margin of 1.47% (1.44% 1Q24). Overall net impaired loans were 1.21% in the quarter, marginally better QoQ (1.25%). Capital adequacy was improved versus the prior quarter (13.22%) with a CET 1 capital ratio of 13.54%.

• In terms of relative value we compare Affin Bank to similarly rated AmBank (A3/BBB+), as well as to Petronas (A2/A-) and Khazanah Capital (A3/A-) for a guide on the curves. The AmBank $ 1/30 trades around 15bp wide to Petronas, and we believe the new Affin Bank 5y could trade a little wider (up to another 5bp), given the better credit quality of AmBank (Q1 NIM 1.94%, CET1 14.8% - Standalone Baa2).

• Fair value is therefore estimated at z+130bp (T+92bp)

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUD: A$ Softens As Equity Markets Lacklustre

As the US dollar strengthens (BBDXY +0.1%), risk-averse currencies are marginally outperforming today given lower US equity futures and subdued China/HK indices. AUDUSD is down 0.2% to 0.6379, close to the intraday low, after a high of 0.6407 earlier in the session, but is not finding support from PBoC comments that it will cut rates and RRR. The pair continues to struggle to hold gains above 64c. There has been little news today with the focus on Wednesday’s Q1 CPI data.

- AUDJPY is down 0.2% to 91.69 but off the intraday low of 91.59. AUDEUR is 0.2% lower at 0.5620 down from 0.5640 earlier. AUDGBP is -0.1% to 0.4802. AUDNZD though is little changed at 1.0723 off the intraday trough of 1.0705.

- Equities are mixed with the ASX up 0.9% and Topix +1.0%, CSI 300 flat but Hang Seng down 0.1% and S&P e-mini -0.4%. Oil prices are lower with WTI -0.2% to $62.92/bbl. Copper is down 0.9% and iron ore around $98/t.

- Later US April Dallas Fed manufacturing and UK April Nationwide house prices are released. ECB’s de Guindos presents ECB’s 2024 Annual Report.

CHINA: Bond Futures Up as Equities Down

- China’s bond futures were up modestly on Monday as equities were marginally down.

- The 10Yr bond future is up +0.09 to 108.895; moving above the 20-day EMA of 108.70.

- The 2Yr bond future is up +0.02 to 102.33 and remains firmly below all major moving averages, the nearest being the 20-day EMA of 102.44.

- Despite this morning’s move, all major moving averages for the 2Yr are pointing downwards, a sign that the bearish momentum remains in place.

- China’s bond market has come off the back of a very quiet week last week, with limited movement and the CGB 10Yr is -1bp lower in this morning's trading at 1.65%

- The week ahead the focus is on the PMI’s tomorrow.

AUSSIE BONDS: Richer & At Bests On A Data-Light SEssion

ACGBs (YM +3.0 & XM +5.5) are richer and at Sydney session highs on a data-light day.

- Cash US tsys are slightly mixed, with a flattening bias, in today’s Asia-Pac session after Friday’s solid.

- “The Australian economy will expand 1.9% in 2025, 2.3% in 2026 and 2.5% in 2027, according to a survey conducted by Bloomberg News. The chance of a recession happening over the next 12 months is 15 percent, according to 14 respondents. 2025 CPI forecast at +2.5% y/y versus prior survey +2.6%. RBA Central Bank Rate seen at 3.85% by end-2Q25, current rate is 4.10%.”

- Cash ACGBs are 4-7bps richer with the AU-US 10-year yield differential at -7bps.

- Swap rates are 6-8bps lower, with the 3s10s curve flatter.

- The bills strip has bull-flattened, with pricing -2 to +3.

- RBA-dated OIS pricing is flat to 6bps softer across meetings today. A 50bp rate cut in May is given a 12% probability, with a cumulative 118bps of easing priced by year-end (based on an effective cash rate of 4.09%).

- The AOFM plans to sell A$1200mn of the 2.75% 21 June 2035 bond on Friday.