AUSSIE BONDS: ACGB Dec-34 Supply Well Absorbed But With Less Demand

Expectations of strong pricing at auctions were confirmed, with the latest ACGB Dec-34 supply achieving a weighted average yield that printed 0.40bp through prevailing mids (per Yieldbroker). However, the cover ratio decreased to 2.1033x from 3.1708x.

- As highlighted in our auction preview, the current outright yield was 20bps higher than at the previous auction, but around 40bps below the late-2024 peak.

- The 3s/10s yield curve was around 10-15bps flatter than the level at the last auction and sat 40bps below its April peak — the steepest level since late 2021.

- The auction did come amid improving sentiment toward long-term global bonds, with the line’s inclusion in the XM basket also likely enhancing its relevance for benchmark-driven accounts.

- The ACGB Dec-34 cash line and the XM futures contract are slightly richer in post-auction dealings.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CHINA: Weekly Preview: The Macro, Valuation, Sentiment, Technicals Lens

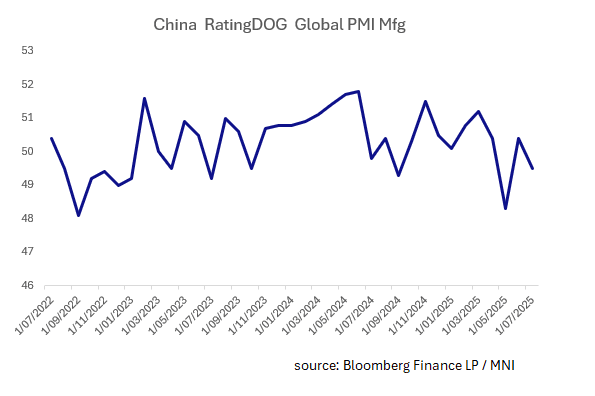

Macro: last week saw China's Industrial Profits in July decline, marking a third consecutive month. China Industrial Profits YoY contracted -1.5%, following -4.3% in June. This is the seventh monthly decline out of the prior 12. Over the weekend the official PMIs were released with the Manufacturing remaining in contraction at 49.4 (from 49.3 prior) and non manufacturing edging up to 50.3 from 50.1. For the week ahead we have the RatingDog China PMI Manufacturing and Services (formerly CAIXIN), as the key release. The PMI Manufacturing had contracted below 50 in July and markets will be looking for a bounce back as signs the economy is recovering from the trade war.

Fig1: China RatingDog (formerly CAIXIN) PMI Manufacturing

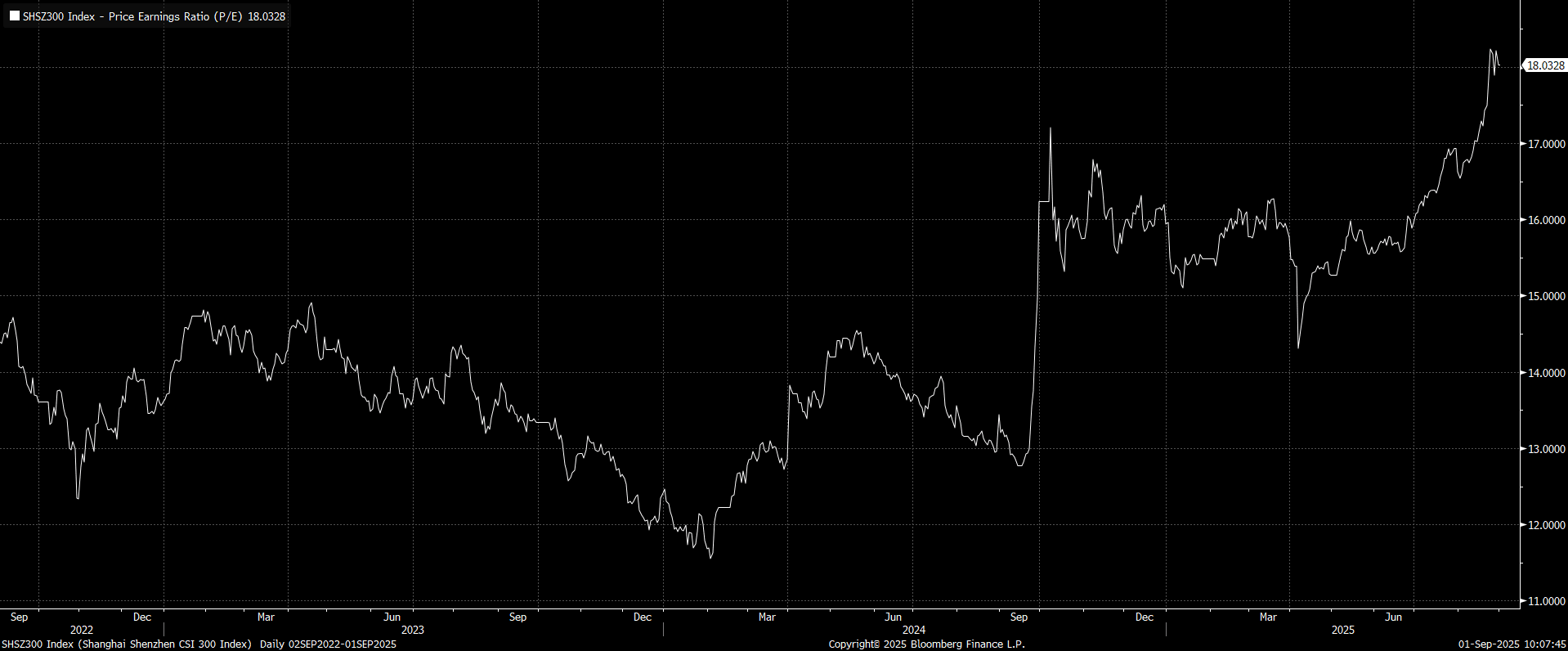

Valuations: the run up in equities of late has been strong with anecdotal evidence of retail account opening for new equity investors growing strongly and flows out of fixed income products increasing. The performance of the CSI 300 has been strong and P/Es now are looking at top end of the three year ranges, though with some economic data suggesting growth is stabilizing to improving, these valuations could have some further to run.

Fig2: CSI 300 Price to Earnings

Sentiment: as evidenced by the flow of funds into equity, sentiment has been on an improving trend. After a multi year decline in housing, investors are seeking investment sources to invest in and with the data suggesting that the economy is not falling any further and perhaps has some upside potential, the asset allocation into equities is strong.

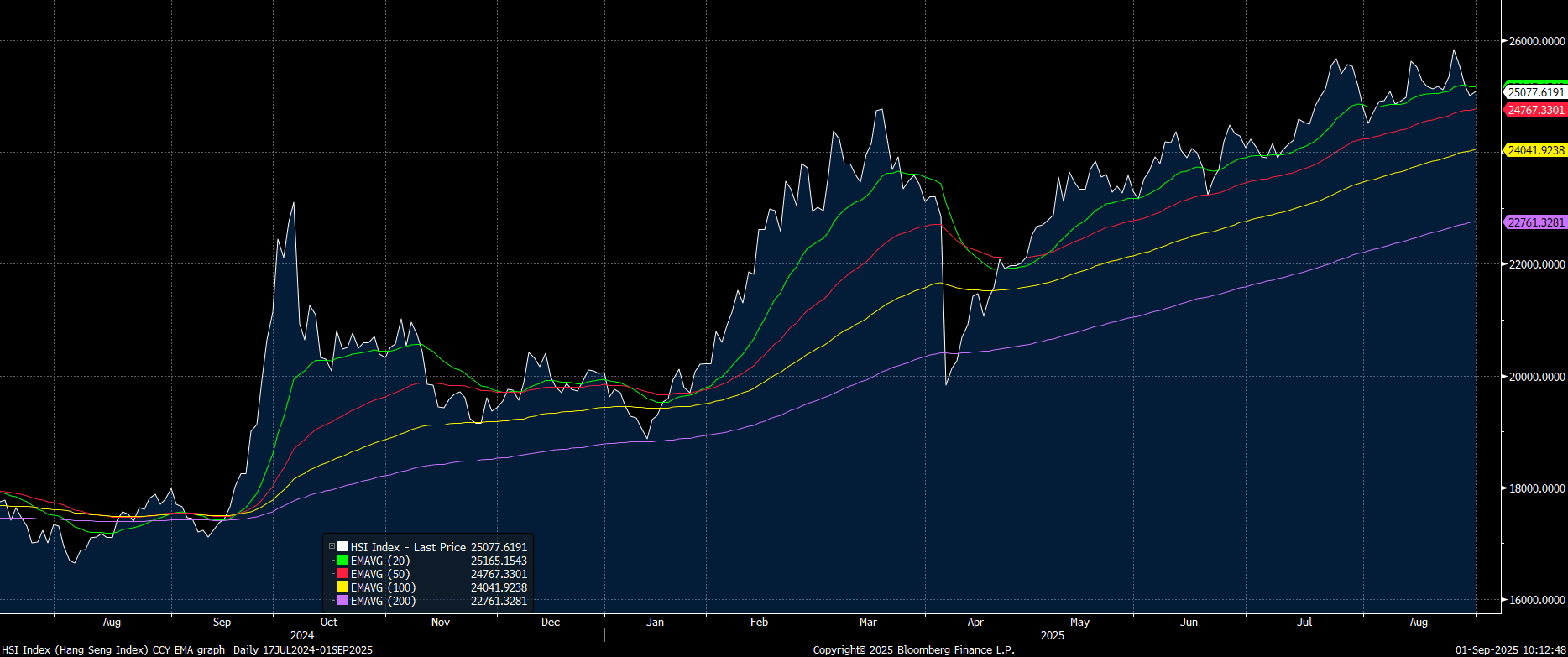

Technicals: the Hang Seng has underperformed its onshore equivalents and currently sits below the 20-day EMA, whereas the CSI 300 is significantly above its 20-day EMA. The event to watch would be for any performance in the Hang Seng to emulate the onshore bourses and test the 20-day EMA.

Fig 3: Hang Seng vs 20, 50, 100 and 200-day EMA

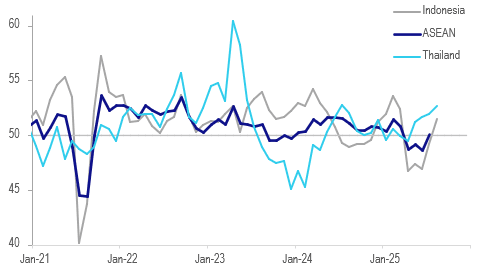

ASIA: ASEAN Manufacturing PMIs Show Growth In August

August S&P Global manufacturing PMIs for ASEAN released today were all in growth territory signalling stronger growth in activity in the month. Also confidence in the outlook improved as uncertainty around global trade began to ease in July. The ASEAN aggregate is released on Wednesday. Thailand was the outperformer amongst the countries printing today with the PMI rising to 52.7 from 51.9 and Indonesia returned to growth at 51.5 after 49.2. Political turmoil in both could impact the next print.

- Thailand’s increase in manufacturing growth to its highest in over a year was driven by higher domestic new orders while export orders fell for the first time since April. This drove destocking and increased purchasing activity but staffing levels were stable due to resignations rather than an unwillingness to hire. Business confidence rose to its highest in close to two and a half years due to new products and business expansion, according to S&P Global.

- Thai cost inflation fell slightly due to discounting but it was passed onto customers driving a moderate increase in selling prices.

- Indonesia’s manufacturing sector returned to growth for the first time since March as higher production and orders, both domestic and export, drove a pickup in hiring and purchasing. Input cost inflation was driven higher by increased imported inflation from a stronger USD and was passed on driving selling price inflation to its highest since July 2024.

- The Philippines manufacturing PMI was little changed at 50.8 but confidence reached a new 2025 high. There was a small rise in orders but external demand was its highest since the start of 2025.

ASEAN S&P Global manufacturing PMIs sa

Source: MNI - Market News/Bloomberg Finance L.P.

FOREX: Mixed Positioning Shifts, Asset Managers Still Prefer EUR, JPY - CFTC

FX positioning shifts, per CFTC, were once again mixed in the week ending the 26th of August (last Tuesday), see the table below.

- On the leveraged side, there was very little net change in the majors, with modest JPY, EUR selling, but some GBP buying. AUD and NZD also saw some buying in the leveraged space, with NZD almost back to a net long position. The other standout in this space was the addition of net longs for MXN.

- On the asset manager side, longs in EUR and JPY were added to, but mostly net selling was evident elsewhere. GBP and AUD shorts were added to, likewise for CAD.

- These mixed trends reflect broader USD moves, where aggregate indices remain within recent ranges. Asset managers prefer JPY and EUR over the USD though, which has been a consistent theme for a while. AUD shorts may also be challenged if we can push above 0.6600.

Table 1: CFTC Positioning Change & Outright Position By Major Currency

| Leveraged Contracts | Asset manager Contracts | |||

| Weekly Change | Outright Position | Weekly Change | Outright Position | |

| JPY | -1427 | -52275 | 5382 | 76761 |

| EUR | -1123 | 8588 | 5162 | 403059 |

| GBP | 1906 | 27578 | -7475 | -74850 |

| AUD | 1371 | -6447 | -5854 | -78758 |

| NZD | 3779 | -225 | -1545 | -4743 |

| CAD | -2480 | -38314 | -4211 | -69988 |

| CHF | 27 | 289 | -807 | -39506 |

| MXN | 6738 | 28529 | 2208 | 33242 |

Source: Bloomberg Finance L.P./MNI