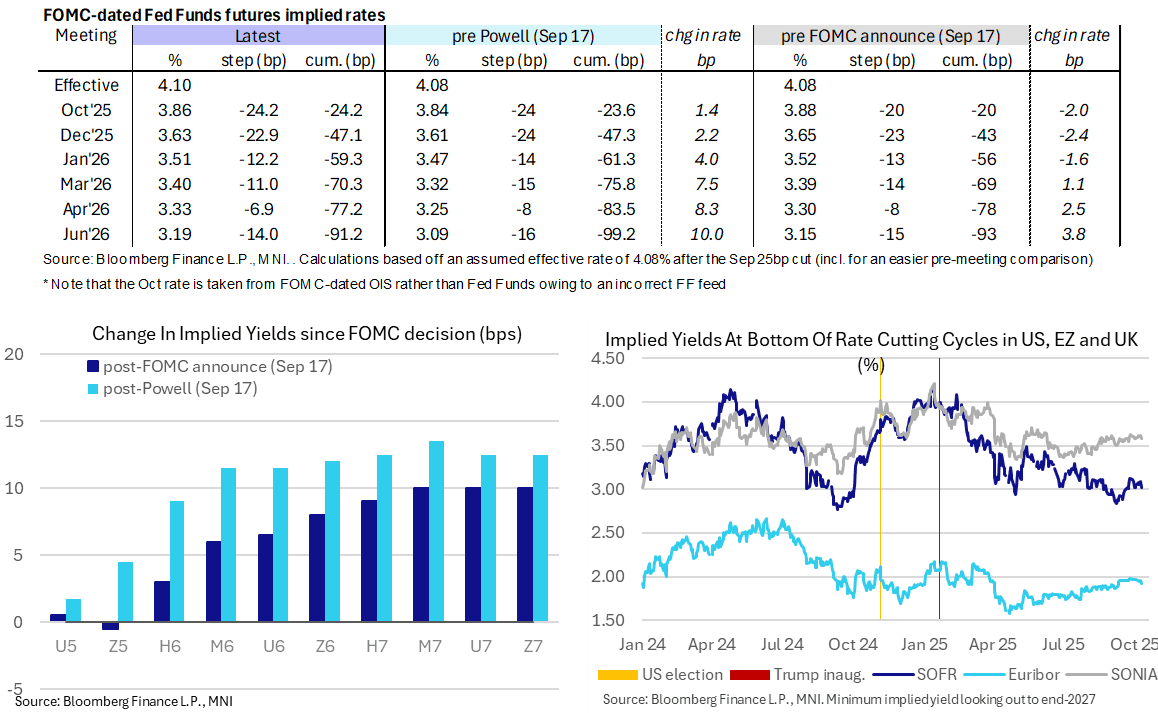

STIR: 110bp Of Fed Cuts Seen Ahead As Trump-China Tensions Set The Tone

Oct-10 2025 16:43

- US rates markets have pared some of their rally on Trump threatening more extensive tariffs on China and possibly withdrawing from his face-to-face meeting with Xi, certainly to a greater degree than has been the case in equities.

- It still clearly sets the tone for the day though, with Fed Funds implied rates 2bp lower on the day for Dec, 5bp lower for Mar and 7bp lower for Jun.

- Cumulative cuts from 4.10% effective: 24bp Oct, 47bp Dec, 59.5bp Jan, 70.5bp Mar, 77bp Apr and 91bp Jun.

- SOFR futures trade between 2.5 ticks higher for the Z5 through to +7.5 in U7 and Z7.

- It sees the implied terminal yield 6.5bp lower on the day at 3.02% (SFRH7), which if maintained would be back to the 3.025% close seen after last week’s soft ADP report. It roughly points to 110bps of cuts ahead.

- Still to come, St Louis Fed’s Musalem (’25 voter, hawk) who we have down as likely one of the six FOMC members who penciled in no further cuts to year-end following the 25bp cut at last month’s FOMC meeting.

- Today’s U.Mich consumer survey, the sole data release for the day, didn’t move the needle, nor have reports of “substantial” federal layoffs beginning under the shutdown.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US OUTLOOK/OPINION: Nomura Nudge Headline CPI Estimate Higher After PPI

Sep-10 2025 16:43

- Giving a sense of the scope for potential revisions to analyst estimates for both CPI and PCE, we note a minor upward tweak in Nomura’s headline CPI estimate but no change in core CPI ahead of tomorrow’s release.

- Nomura now see headline CPI at 0.37% M/M instead of 0.34 on stronger than expected PPI residential electricity prices whilst their core CPI estimate is unchanged at 0.336% M/M.

- Their core PCE tracking has been revised just 1bp higher to 0.35% M/M.

- A reminder that both their core CPI and core PCE estimates were marginally higher than our take on the analyst median, which stood at 0.32% M/M for core CPI and 0.31% M/M for core PCE in our CPI preview published yesterday.

FOREX: AUDUSD Trades to Fresh 10-Month Highs Following Soft US PPI

Sep-10 2025 16:39

- Despite the dovish adjustment for US yields in the aftermath of the US PPI report, the impact on the USD index has been more muted, with just a 0.05% move lower on the session. Major pairs such as EURUSD and USDJPY have held relatively contained ranges as we await the August CPI report to follow on Thursday.

- With that said, firmer equity sentiment and higher oil prices have notably buoyed riskier currencies, with AUD, NZD and NOK clearly outperforming in G10.

- AUDUSD has breached a key resistance point, trading up to a fresh 10-month high of 0.6636 in the process and strengthening the underlying bullish trend. The next targets for the move are 0.6688 (Nov 07 high) and 0.6700, the 76.4% retracement of the Oct-Apr selloff.

- In contrast, lingering French political risks and geopolitical developments between Russia/Poland have relatively weighed on the Euro, allowing EURAUD to extend its recent depreciation. Despite being a slow burner, EURAUD has respected the breach of trendline support (drawn from the year’s lows) and the cross briefly slipped through the July 31 lows and bear trigger at 1.7674. Targets on the downside include 1.7462 (Jun 10 low) and 1.7248 (May 14 low).

- Oil strength compounded the performance for NOK on the back of the higher-than-expected underlying Norwegian CPI print (3.1% Y/Y vs. Exp. 2.9%). As a result, EURNOK has traded steadily lower, clearing the September lows. The cross has also shown through 61.8% retracement for the upleg posted off the June low, opening next support into 11.5416.

- During Thursday’s APAC session, RBNZ Governor Hawkesby will speak, before Australia consumer inflation expectations. The focus will then turn to the ECB rate decision/press conference and the key US CPI release.

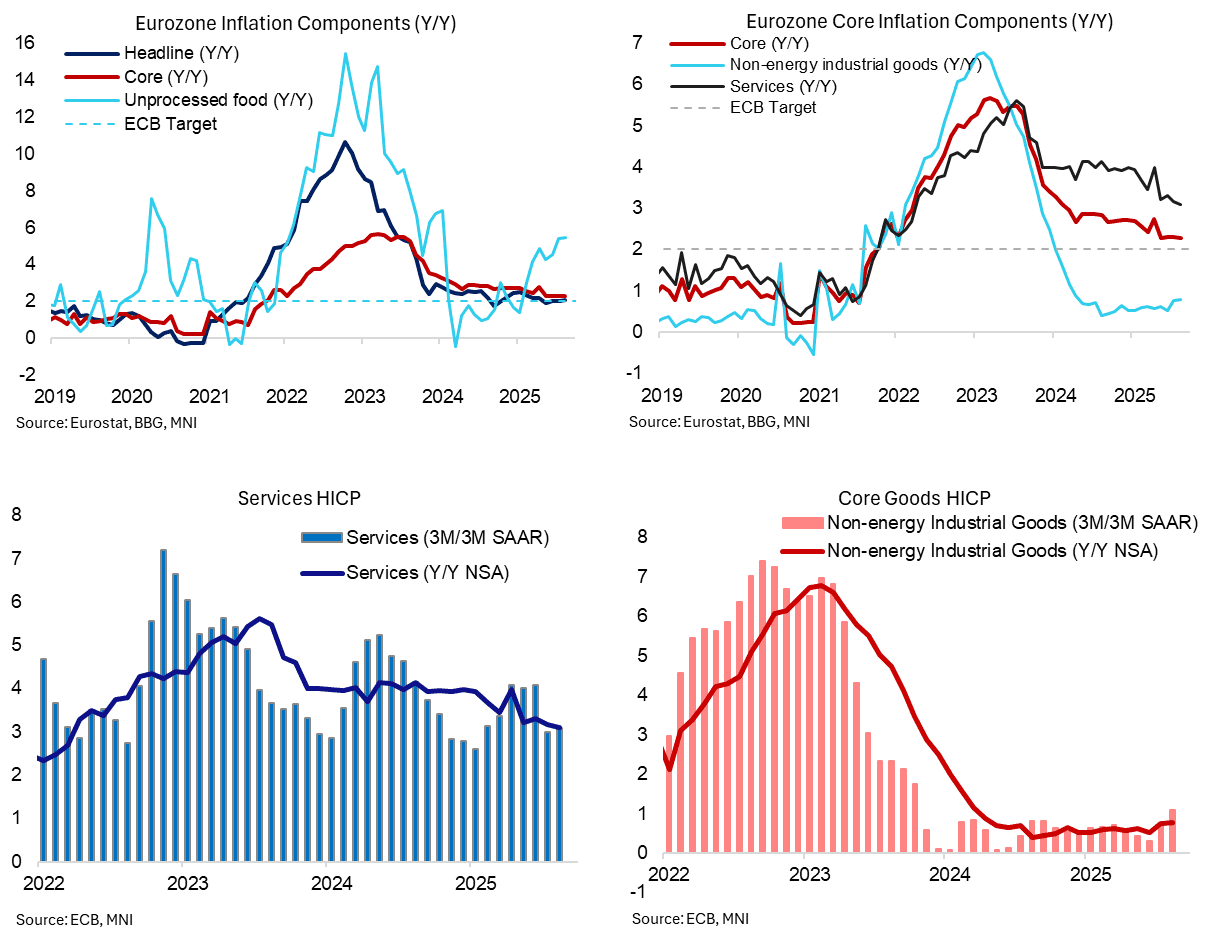

ECB: Macro Since Last ECB: Inflation - HICP At Target, Core Still A Little Above

Sep-10 2025 16:35

- The two months of HICP data have been mixed from a headline inflation perspective whilst core inflation has continued to track at a near identical Y/Y pace to that ahead of the July ECB decision.

- Specifically, July headline inflation came in on the high side of analyst expectations at 2.04% Y/Y (Bloomberg median 1.9) before only just rounding to the 2.1% expected in the preliminary flash release at 2.05% Y/Y.

- Core inflation ticked down to 2.27% Y/Y in August as it continues some stabilization after two months at 2.31% through June-July and 2.28% in May.

- The much-eyed services component has seen some disinflation however, with 3.10% Y/Y in August and 3.15% in July after the 3.32% Y/Y in June known ahead of the July meeting.

- As for 3m/3m momentum metrics using the ECB’s seasonally adjusted data, core momentum firmed from 2.2% in July to 2.4% annualized in August but remains below the 2.7% seen in June. Similarly, services inflation momentum currently stands at 3.1% annualized in August after 3.0% in July, still elevated but at least comfortably below the >4% readings seen the three months prior.

- One area we’ll be watching is whether there is a more widespread discussion around the continued re-acceleration of food inflation, as noted by Schnabel, with something similar seen in BOE commentary in the UK.