FISCAL: IMF Fiscal Monitor Eyes Bleak Medium-Term Outlook

Oct-23 17:22

The IMF's October Fiscal Monitor (link) paints a fairly bleak outlook for developed market government finances over the rest of the decade.

- Advanced economy government balances (in this context, deficits) are seen narrowing from -5.2% of GDP on average in 2024, to -4.2% in 2024-29, but that's substantially larger than the -3.1% pre-pandemic (2012-19) average. That's in spite of primary balances consolidating from -2.7% in 2024 to -1.5%, the latter not far from the -1.0% pre-pandemic norm, because higher interest costs vs earlier years (1.5% of GDP in 2015-29 to 2.4% in 2024-29) will weigh heavily, particularly on the US outlook.

- The US's pre--pandemic average overall government balance was -5.1% of GDP, but that's seen rising to -6.7% in 2024-29 - France (-3.6% to -5.9%) and Germany (+0.9% to -1.1%) are other standouts in terms of expected deterioration.

- Average revenue as a % of GDP is set to remain at roughly 36% through end-2029 (46% for the eurozone, 35-36% for the G7 as a whole). While that's in line with pre-pandemic levels, expenditure is seen stubbornly above 40%, vs 38-39% pre-pandemic (49% for eurozone vs 47-48% pre-2020, 41% for the G7 vs 39% pre-2020).

- The upshot: average gross gov't debt rose from 102% of GDP in 2019, to 122% in 2020, back to 109% in 2023-24 - but that's the end of the improvement, with the trajectory putting average 2029 debt at 114%. Net debt is lower (to 87% end-decade from 82% now) but follows a similar trajectory.

- Either way, as the teaser report released last week pointed out, globally, "Cumulative fiscal adjustment of 3.0–4.5 percent of GDP, on average, is needed to stabilize or reduce debt with high probability" - that is a major and likely unrealistic adjustment and "almost twice the size of past adjustments".

- IMF Directors were concerned that "mediocre medium‑term growth and rising debt trajectories increase the risk that the global economy will become entrenched in a low-growth, high-debt environment".

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

SECURITY: Israel's "Proactive" Operation Lays Groundwork For "Next Phases"

Sep-23 17:17

Wires carrying comments from Israeli Defence Forces' Chief of Staff, Herzi Halevi, stating on today's IDF airstrikes targeting Hezbollah infrastructure and personnel in Lebanon: "This morning we launched a proactive offensive operation targeting combat infrastructure, we are striking targets and preparing for the next phases."

- Reuters notes that Halevi said: "Essentially, we are targeting combat infrastructure that Hezbollah has been building for the past 20 years. This is very significant. We are striking targets and preparing for the next phases," he said in a statement, giving no details but adding that he would "elaborate shortly".

- Israeli Defense Minister, Yoav Gallant, said a short time ago: "In the last day, we have been destroying what Hezbollah has been building for twenty years. [Hezbollah Leader Hassan] Nasrallah has been left alone at the top, entire units of the Radwan force were taken out and tens of thousands of rockets were destroyed."

- The New York Times reports: "Air-raid sirens are blaring throughout Haifa, in northern Israel, warning of a rare rocket attack from Lebanon on Israel’s third-largest city."

- Local sources reporting that the Israeli government has approved a "special situation" throughout the country, but hasn't appeared to issue any new guidance for citizens.

- The Pentagon said in a statement, "in light of increased tensions in the Middle East and out of an abundance of caution, we are sending a small number of additional US military personnel forward to augment forces already in the region. For operations security reasons, we won't comment on or provide specific details."

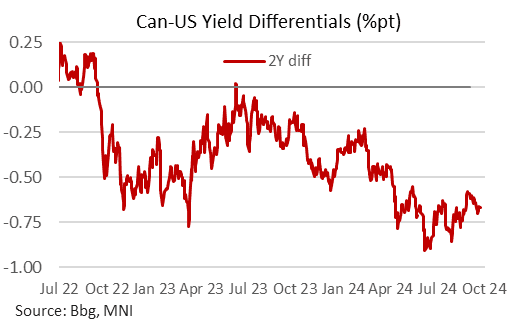

CANADA: Can-US 2YY Differential Within Range, Macklem Speaks Tomorrow

Sep-23 17:06

- GoCs have seen a sizeable reversal of earlier selling pressures, with 2Y yields ~4bps below session highs.

- GoC yields are 2.5bp (2s) to 1.5bp (30s) lower today, with the Can-US 2Y yield differential 0.5bp lower on the day to remain within recent ranges at -67bps - see below chart.

- We have mentioned today another strong wage settlement (15% over two years) and a sizeable uplift in consumer confidence, but moves appear US-led after selling off with strong price components in the flash PMIs for about 30 minutes before more than reversing the move mainly on geopolitics risk-off.

- BoC-dated OIS has been unaffected, pricing a 38bp cut for Oct 23 as the market continues to weigh an upsizing after three consecutive 25bp cuts.

- Tomorrow sees flash mfg sales for August at 0830ET after a solid retail sales advance last week. It’s followed by BoC Gov. Macklem in a fireside chat at 1310ET - text will be made available at 1255ET but, unusually, seemingly with no media lock-up for it.

BONDS: EGBs-GILTS CASH CLOSE: German 2s10s Disinverts As PMIs Come In Weak

Sep-23 17:04

European curves steepened Monday as weak PMIs showed a pullback in regional economic momentum.

- Eurozone (incl each of France and Germany) and UK flash September PMIs came in below expectations across the board on both Manufacturing and Services, adding further impetus to near-term ECB and BoE rate cut expectations.

- An October ECB is now priced at 10bp (40% prob of 25bp), vs 5bp prior.

- Against this backdrop, the German curve bull steepened, with 2s10s disinverting for the first time since Aug 2022. The UK's twist steepened.

- OATS underperformed again (10Y/Bund +2.5bp), weighed down by continued political uncertainty and an FT report that France has requested a further delay in submitting its budget plans to the EC.

- Periphery EGB spreads widened modestly, having reversed early session wides. Note that futures rallied through the cash close.

- Tuesday's schedule includes September German IFO data and appearances by ECB's Muller, Nagel, and Escriva.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is down 8.1bps at 2.149%, 5-Yr is down 6.7bps at 2%, 10-Yr is down 5.2bps at 2.156%, and 30-Yr is down 2.8bps at 2.481%.

- UK: The 2-Yr yield is down 1bps at 3.915%, 5-Yr is up 1bps at 3.754%, 10-Yr is up 2bps at 3.923%, and 30-Yr is up 2.6bps at 4.496%.

- Italian BTP spread up 0.5bps at 135.2bps / Spanish up 0.8bps at 79.7bps