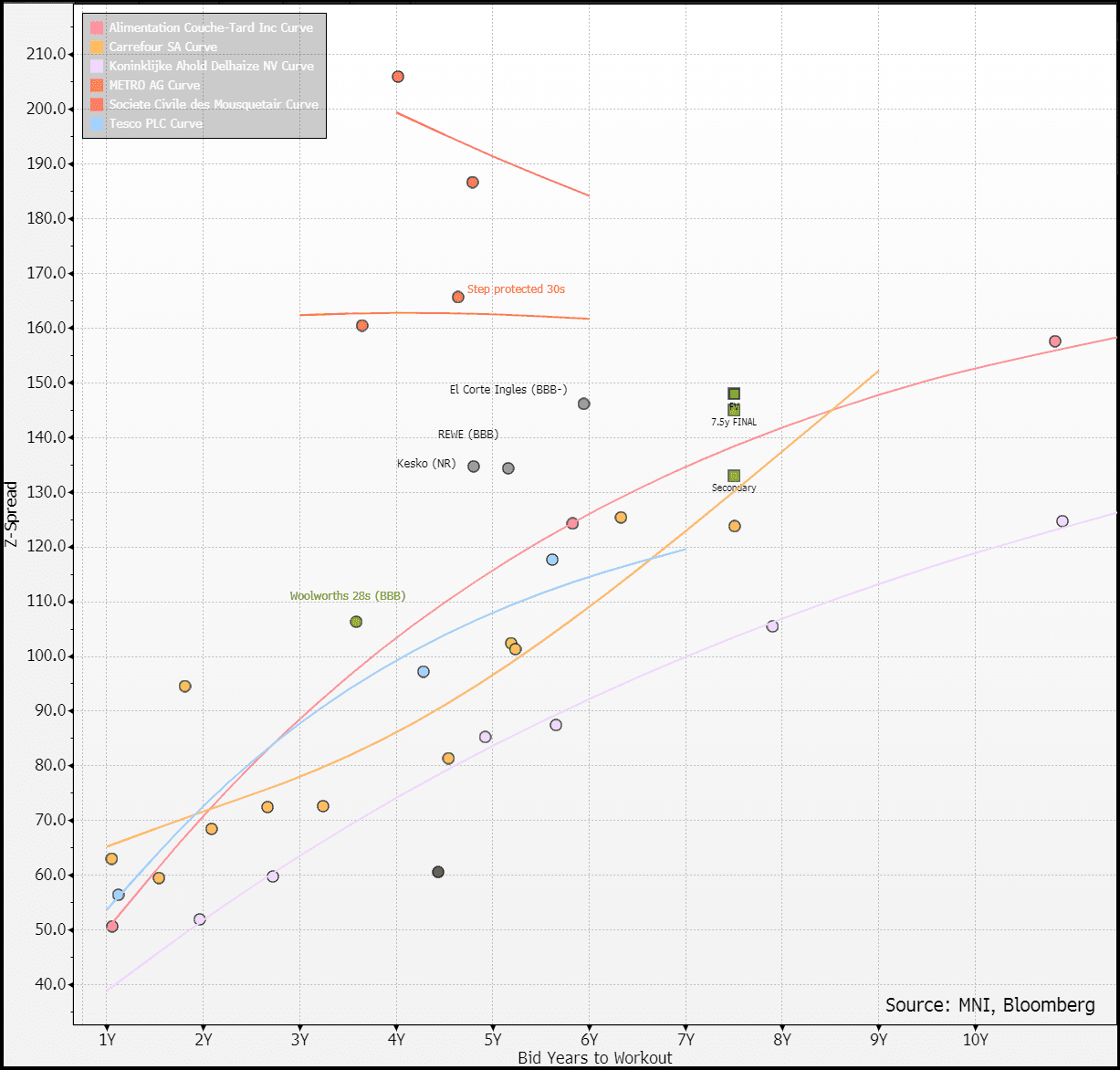

EU CONSUMER STAPLES: Woolworths: Secondary

(WOWAU; Baa2/BBB; Stable)

- Mids at +135, -10 inside final. Its impressive pricing and the single-line liquidity/Aussie discount looks small here.

- We don't see value on it and prefer to wait for 3Q earnings (to March) in two weeks to revisit that view. Still carry/longer term investors who are happy to sit through any weakness/near-term vol may still see value in diversifying out CAFP/Tesco exposure.

- Reminder we have had a unch value view on the 28s since ACCC/regulator completed its investigation in late March - it is +2 since vs. index +18 and we still see some value there. Small selling emerged through the mandate.

Transurban with 8.0x cover and -20 tighter since, Woolworths 6.4x and already -10 tighter.

Wesfarmers will get a warm reception if it decides to come.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US 10YR FUTURE TECHS: (M5) Support Remains Intact

- RES 4: 113-04+ 2.0% 10-dma envelope

- RES 3: 112-13 1.500 proj of the Jan 13 - Feb 7 - Feb 12 price swing

- RES 2: 112-01/02 High Mar 4 / 1.382 proj of Jan 13-Feb 7-12 swing

- RES 1: 111-25 High Mar 11

- PRICE: 110-24+ @ 10:35 GMT Mar 17

- SUP 1: 110-12+/110-00 Low Mar 6 & 13 / High Feb 7

- SUP 2: 109-31+ 50-day EMA and a key near-term support

- SUP 3: 109-13+ Low Feb 24

- SUP 4: 108-21 Low Feb 19

The trend condition in Treasury futures remains bullish and the current consolidation marks a pause in the uptrend. A bull theme is reinforced by MA studies that are in a bull-mode condition, highlighting a dominant uptrend and positive market sentiment. Recent gains have resulted in a print above 111-22+, the Dec 3 ‘24 high. A clear breach of this level would open 112-02 and 112-13, Fibonacci projections. Firm support is 110-00, the Feb 7 high.

MNI: RPT INVITATION: MNI Connect VC With ECB's Olli Rehn On Mar 18

You are invited to listen to a Livestreamed MNI Connect Video Conference with Olli Rehn, Governor of the Bank of Finland & Member of the Governing Council, Europe.

Details below:

- TOPIC OF DISCUSSION: ‘Eurozone economy and ECB monetary policy’

- DATE: Tuesday 18 March

- TIME: 09:00 - 10:15 GMT

- This event will be run as a Zoom Webinar and is a public, on-the-record event.

To register please go to: MNI Webcast Registration

EUROPEAN INFLATION: Italy Final Feb HICP Confirms Flash; Insurance Eases

Italian final February HICP inflation confirmed flash estimates at 1.7% Y/Y (1.74% unrounded, vs 1.66% prior). Core measures were also confirmed, with HICP excluding food, energy, alcohol and tobacco at 1.52% Y/Y (vs 1.79% prior) and HICP excluding energy and unprocessed foods at 1.75% (vs 1.84% prior).

- Looking into the details of important services components: Insurance inflation continued to decelerate to 6.29% Y/Y (vs 6.72% in Jan, 7.07% in Dec), as did restaurants and hotels (2.77% vs 2.95% prior) and recreation and culture (1.73% vs 2.19% prior). Meanwhile, transport services were pulled down by the volatile airfares component (-1.0% Y/Y vs 4.5% prior).

- Within core goods, clothing and footwear inflation dropped sharply to -0.64% Y/Y (vs 0.94% prior). The monthly rate of -2.90% M/M was well above last year’s -1.36% reading, but remains above the 2015-2019 average of -4.48% M/M.

- MNI’s inflation breadth metrics indicate that the proportion of sub-components with annual inflation rates between 1-3% Y/Y rose to 42% (vs 38% prior), the highest since May 2024.