CNH: USD/CNH Eyeing Downside 7.1500 Test, Trade Optimism Boots Sentiment

USD/CNH tracks near 7.1515/20 in early Thursday dealings. The CNH posted a solid 0.27% gain for Wednesday's session, which slightly outperformed broader USD softness (DXY and BBDXY indices fell by a little over 0.20%). Spot USD/CNY finished up at 7.1543, while the CNY CFETS basket tracker fell a further 0.16% to 95.71 (per BBG).

- For USD/CNH, we are close to earlier July lows at 7.1501. A clean break sub this level is likely to see focus shift to a test under 7.1000, which were levels last seen in early Nov. The 20-day EMA resistance point is back above around 7.1725.

- Broader USD sentiment remains on the backfoot, with global equities rallying on Wednesday amid optimism around trade deals. US Tsy Secretary stating that negotiations with China are on track also providing a tailwind. This comes ahead of further talks in Stockholm next week. In remarks this morning US President Trump stated: "*TRUMP: IN PROCESS OF COMPLETING CHINA DEAL" - BBG.

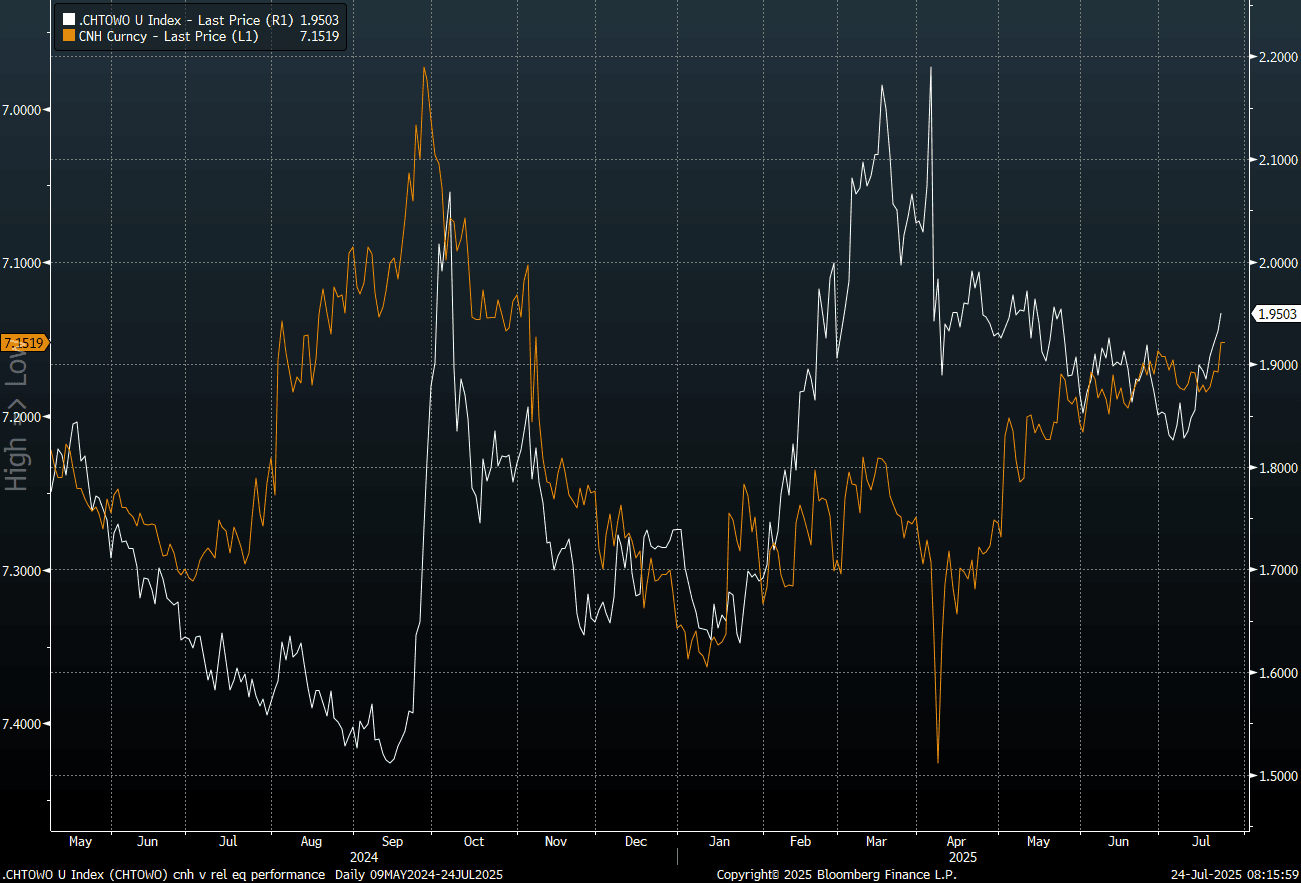

- Onshore China equities lost momentum in late trade yesterday, with the CSI 300 finishing close to flat. Trends in the Golden Dragon index in US trade were better, rising 0.75%. The China to world equity ratio is at fresh highs since May, see the chart below, which is the white line (note USD/CNH is inverted on the chart, the orange line).

- On the data front today we have June SWIFT global payments in CNY, the prior outcome was 2.89%.

Fig 1: USD/CNH (Inverted) Versus China To World Equity Ratio

Source: Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUD: AUD/USD - Big Reversal Off Support

The AUD had a range overnight of 0.6373 - 0.6463, Asia is opening around 0.6470. A combination of some dovish Fed speak and a muted and well contained Iranian response to the US bombings have seen “turnaround Tuesday” come early. Quite the reversal and a big daily shadow on the charts shows how quickly the market is to return to its favoured trade of selling the USD. "TRUMP: ANNOUNCES 12 HOUR CEASEFIRE BETWEEN IRAN AND ISRAEL" - BBG. This should add to the momentum as risk opens positively in our session, ESU5 +0.35%, NQU5 +0.48%.

- AUSTRALIA: May CPI Prints On Wednesday. In a data light week, the focus will be on Wednesday’s CPI for May which consensus expects to ease to 2.3% from 2.4%. Trimmed mean ticked up to 2.8% in April and has been around 2.7-2.8% since December suggesting a stalling in disinflation. The next RBA meeting is July 7-8.

- (Bloomberg) - "Australian banks are set to face a leap in impaired loans next year, based on asset-backed securities' (ABS) deteriorating credit metrics, combined with much higher business insolvencies. NAB's problem loans in business and small enterprises spiked in March, while auto ABS saw a big uptick in delinquencies, according to analysis."

- From looking vulnerable to a collapse, down around 1.2% at 1 point then ending positive on the day is quite the feat.

- The AUD/USD bounced hard off its support and is now back in the middle of its recent range.

- Price remains in the wider 0.6350 - 0.6550 range for now. After failing to break lower and risk looking like it can extend higher can the AUD have another go back towards the 0.6550 area ?

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.6500(AUD1.41b June 26), 0.6450(AUD553m June 26).

- CFTC Data shows Asset managers maintaining their shorts, the Leveraged community though again added to their shorts.

- Data/Event: CPI Tomorrow

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

AUSSIE 10-YEAR TECHS: (U5) Bear Cycle Remains Intact For Now

- RES 3: 96.501 - 76.4% of the Mar 14 - Nov 1 ‘23 bear leg

- RES 2: 96.207 - 61.8% of the Mar 14 - Nov 1 ‘23 bear leg

- RES 1: 95.960 - High Apr 7

- PRICE: 95.800 @ 15:19 BST Jun 23

- SUP 1: 95.415/95.300 - Low May 15 / Low Jan 14

- SUP 2: 95.275 - Low Nov 14 (cont) and a key support

- SUP 3: 94.707 - 1.0% 10-dma envelope

Aussie 10-yr futures rallied well on the RBA rate decision, reversing a small part of recent weakness. Recent price action pressured prices through to new pullback lows last week. Next support undercuts at 95.420 (pierced), the Feb 13 low, ahead of 95.275, the Nov 14 low and a key support. Clearance of this level would strengthen a bearish condition. To the upside, a recovery of recent losses would shift attention to resistance at 96.207, a Fibonacci retracement point.

US TSYS: Front-End Leads Yields Lower

TYU5 reopens at 111-06+, down 0-08 from closing levels in today’s Asia-Pac session.

- Overnight the US 10-year yield had a range of 4.2886% - 4.4028%, closing around 4.35%.

- Treasury yields ended lower overnight, Goolsbee and Bowman dovish comments saw the front-end lead the move causing the yield curve to steepen(2s10s +1.49 at 48.017, 5s30s +3.32 at 96.029).

- MNI FED: Bowman And Waller Setting Up For A July Dissent. Though both Gov Waller and Vice Chair Bowman have come out after the June meeting and declared tentative support for a rate cut in July, this still appears to be a minority view. They might be the two biggest doves on 2025 rates. While the SEP is not a perfect guide to guessing policy preferences, there were two.

- MNI US DATA: More Warning Signs In Housing Despite Existing Home Sales Pickup. Existing home sales unexpectedly ticked up in May to a 4.03M seasonally-adjusted annual pace, from 4.00M in April (and vs 3.95M survey). While the lack of further deterioration is a slightly brighter note for a beleaguered housing market, existing sales were down 0.7% Y/Y and remain well below pre-pandemic levels.

- The 10-year yield attempted to break below its 4.30% support overnight, it failed on its first attempt but a sustained move back below there would likely see the move pick up momentum. 10-year yields would need to get back above 4.45/505 again to alleviate this downward pressure.