FOREX: USD - BBDXY Pulls Back As Risk Rebounds In Asia, How Far Can It Extend ?

The BBDXY has had a range today of 1218.27 - 1220.60 in the Asia-Pac session; it is currently tradin...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

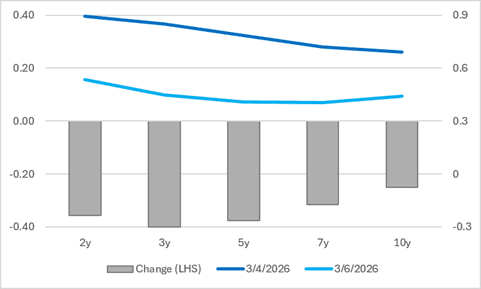

AUSSIE BONDS: Has ACGBs Outperformance Vs. US Tsys Run Its Course?

ACGBs have outperformed Us tsys across the curve over the past two months, as Australian yields have declined on reduced expectations of further RBA tightening while US yields have risen amid a scaling back of Fed easing expectations.

- The move in Australian rates has been broadly consistent with recent RBA messaging. Governor Bullock recently noted that three consecutive rate hikes have provided the Board with “space” to assess incoming data and developments. However, given the heightened degree of uncertainty, the Board remains open-minded, suggesting a pause at the 16 June meeting is a distinct possibility.

- The move in Australian rates has been broadly consistent with recent RBA messaging. Governor Bullock recently noted that three consecutive rate hikes have provided the Board with “space” to assess incoming data and developments. However, given the heightened degree of uncertainty, the Board remains open-minded, suggesting a pause at the 16 June meeting is a distinct possibility.

- In its May forecasts, the RBA judged inflation risks to be skewed to the upside and incorporated additional policy tightening in 2026. Even under that assumption, trimmed mean inflation was not projected to return to the target band until the second half of 2027.

- Against this backdrop, the strong period of ACGB outperformance may have largely run its course, at least from the Australian side of the equation.

- Further support for this view came from yesterday’s Fair Work Commission decision to raise the minimum wage by 4.75%, an outcome that exceeded market expectations and adds to concerns around domestic wage and inflation pressures.

Figure 1: AU-US Spreads Across Curve – Now Vs. Early April

Bloomberg Finance LP / MNI

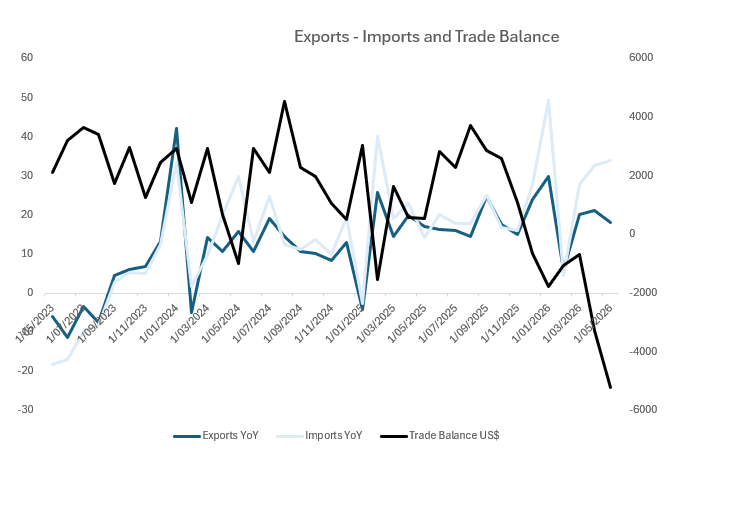

ASIA: Vietnam: Energy Costs Weighing Heavy on Imports

- Vietnam recorded a monthly trade deficit of USD $5.21 billion for May, a sharp expansion from the USD $3.28 billion deficit recorded in April as a massive surge in the cost of imports bites. For the January–May period, Vietnam’s total trade deficit has widened significantly to USD $13.8 billion. This marks a huge structural shift for an economy that traditionally relies on a strong trade surplus to support its currency and foreign reserves.

- May imports soared 33.8% YoY to USD $52.14 billion. Energy commodities are driving this surge; refined petroleum product imports jumped 81.6% in value despite only a 15% increase in volume, while liquefied gas imports rose 40.6% in value

- May exports rose a healthy 18% year-on-year to USD $46.93 billion. However, this marks a deceleration from the 21% annual growth recorded in April, signaling that global demand or logistics constraints are beginning to cap outbound capacity. Rice exports remained a bright spot, gaining 19.3% in volume to reach 925,000 tons for the month.

- YoY consumer inflation accelerated to 5.6% in May (up from 5.46% in April), driven primarily by the soaring costs of imported fuel, energy, and supply chain logistics.

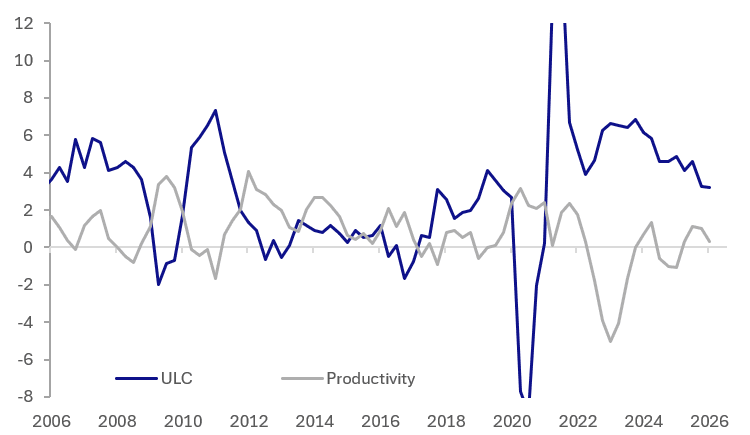

AUSTRALIA DATA: Average Compensation & ULC Ease, Productivity Problem Persists

The RBA is likely to be reassured by the easing in unit labour cost and compensation growth as well as inflation across key sectors based on implicit price deflators. However, Australia’s productivity problem continues with it recording its weakest quarter since Q3 2024. The next Board decision is 16 June and it is likely to be on hold after 75bp of tightening as it monitors data and events.

Australia productivity vs ULC y/y%

Source: MNI - Market News/ABS

- Unit labour costs rose 0.8% q/q in Q1 with annual growth moderating 0.1pp to 3.2% y/y, the lowest since Covid-impacted Q1 2021. With wages to rise 4.75% for around 21% of the workforce on 1 July, ULC trends in H2 are likely to be watched closely especially for any indirect effects from the Fair Work Commission decision.

- In terms of inflation risks, weak productivity makes it more important that 4.75% doesn’t become a benchmark for wage demands. Q1 productivity fell 0.6% q/q to be up only 0.3% y/y after Q4’s flat & +1.0% outcomes. The 1.0% q/q rise in hours worked after Q4’s 0.9%, driven by the market sector, is pressuring productivity with output not keeping up.

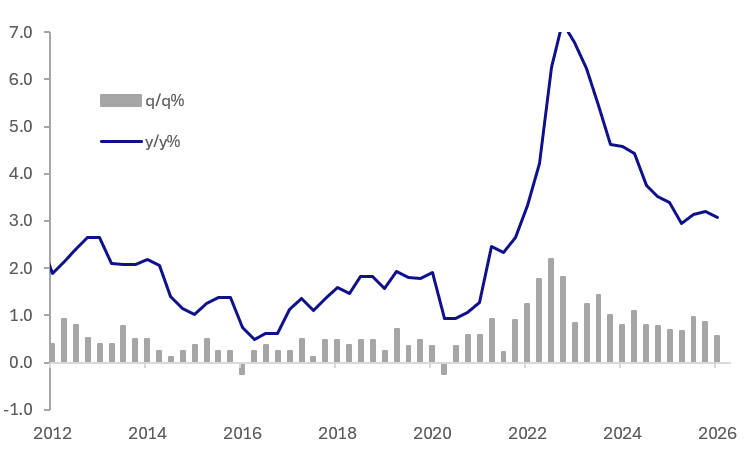

- The easing in average compensation in Q1 is helpful for the inflation outlook. It rose 0.6% q/q in Q1, the lowest rise since Q3 2024, bringing annual growth to 4.3% from 4.9%, but still above Q2 2025.

- GDP IPD moderated 0.7pp to 2.4% y/y, but still above Q1 2025’s 2.2%. Private consumption inflation has been hovering above the top of the 2-3% band for three quarters with Q1 0.1pp lower at 3.1% y/y. However, it remains above pre-Covid rates.

Australia household consumption IPD %

Source: MNI - Market News/ABS