FED: US TSY 4W BILL AUCTION: HIGH 4.290%(ALLOT 1.54%)

Jul-31 15:32

- US TSY 4W BILL AUCTION: HIGH 4.290%(ALLOT 1.54%)

- US TSY 4W BILL AUCTION: DEALERS TAKE 29.42% OF COMPETITIVES

- US TSY 4W BILL AUCTION: DIRECTS TAKE 3.14% OF COMPETITIVES

- US TSY 4W BILL AUCTION: INDIRECTS TAKE 67.44% OF COMPETITIVES

- US TSY 4W AUCTION: BID/CVR 2.63

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OPTIONS: Larger FX Option Pipeline

Jul-01 15:32

- EUR/USD: Jul03 $1.1550(E2.1bln), $1.1600(E3.8bln), $1.1625(E1.2bln), $1.1650-60(E1.8bln), $1.1700(E2.6bln), $1.1720-25(E1.1bln), $1.1775(E2.0bln), $1.1800(E4.7bln), $1.1900(E1.2bln); Jul07 $1.1770(E1.6bln)

- USD/JPY: Jul03 Y142.00($1.1bln), Y143.95-00($980mln), Y145.00-10($1.2bln)

- AUD/USD: Jul04 $0.6500(A$1.2bln), $0.6600(A$2.6bln)

- USD/CAD: Jul03 C$1.3600($1.2bln)

- USD/CNY: Jul03 Cny7.4000($3.0bln)

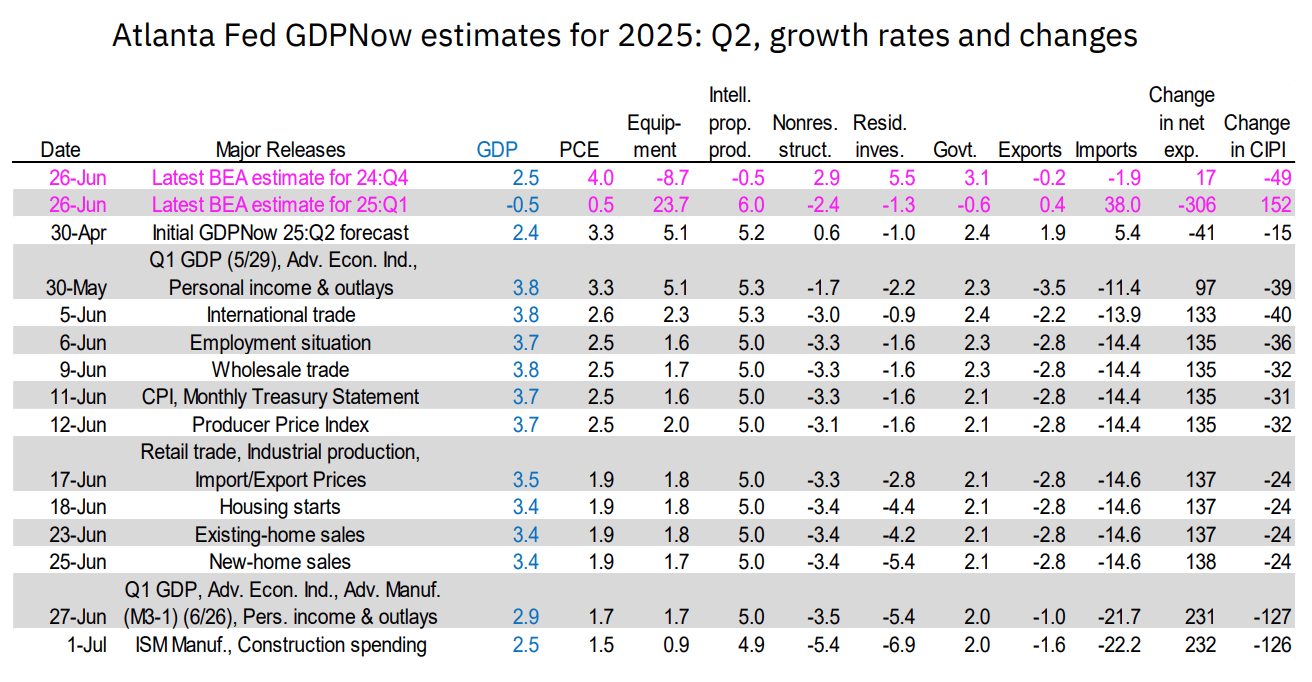

US OUTLOOK/OPINION: GDPNow Souring On Final Domestic Demand

Jul-01 15:31

The Atlanta Fed's GDPNow estimate for Q2 fell once again in the latest update, to 2.5% Q/Q SAAR vs 2.9% in its previous full update on Jun 27.

- This comes following the latest construction activity and ISM Manufacturing data which saw estimates of real PCE for the quarter fall to 1.5% (was 1.7%, and 0.5% in Q1), and as we had flagged with the Construction report, residential investment is seen shrinking 6.9% (was 5.4%, and -1.3% in Q1) with nonresidential structures falling 5.4% (was -3.5%, and -2.4% in Q1). Equipment investment is now seen growing just 0.9% (prior est was 1.7%, and was +23.7% in Q1). See table below for details.

- This is the slowest forecast rate of growth for the quarter since the initial nowcast of 2.4% and is well down from the 3.8% high in early June since when it has been continually downgraded.

- As it stands, the estimated GDP growth of 2.5% would be 1.2% absent inventories (which are set to subtract 2.2pp from GDP) and net exports (estimated to contribute 3.5pp to GDP), suggesting pretty weak domestic final demand dynamics.

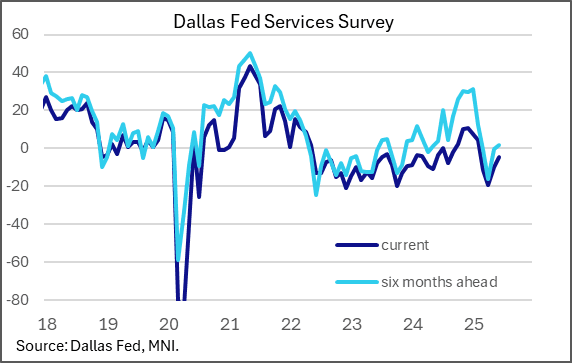

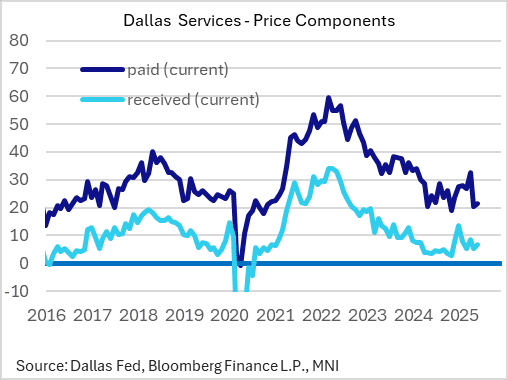

US DATA: Dallas Fed Services Activity Normalizing, Inflation Dynamics Tame

Jul-01 15:20

The Dallas Fed's Texas Service Sector Outlook Survey shows General Business Activity index rose to its best level in 5 months in June, -4.4 from -10.1 prior. That's still contractionary, but the 6-month ahead reading rose to 1.5 from -0.3, marking the first positive reading since February.

- The current reading is consistent with levels that prevailed through much of 2023-24, before volatility associated with the November 2024 elections through the tariff uncertainty that picked up strongly earlier in 2025. That said, the anecdotes to the report were almost universally negative, with several respondents citing elevated policy uncertainty and soft demand.

- Inflation didn't seem particularly pronounced. Prices paid ticked up to 21.3 from 20.5, though that's well below the average of 29 in the first 4 months of the year. Prices received also edged higher to 6.8 from 5.2 but still below the Jan-Apr average of 9.

- Highlights from the report: "Labor market measures indicated employment and hours worked were largely unchanged again in June. ... Perceptions of broader business conditions continued to worsen in June, though the indexes were less negative than the prior month.... The wages and benefits index remained largely unchanged"

- The retail sales index, a sub-category of the report, remained weak with the sales index at –29.5 vs –30.5 prior.