LOOK AHEAD: US Retail Sales, Jobless Claims, Fedspeak and Trump Address

Jul-16 10:15

US Data/Speaker Calendar (prior, estimate). All times ET * 07/16 0830 Retail sales (0.9%, 0.2%), Co...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

LOOK AHEAD: Trump At G7, Weekly ADP & Congested 0830ET Data Before 20Y Supply

Jun-16 10:10

US Data/Speaker Calendar (prior, estimate). All times ET

- 06/16 0600 Trump in working lunch with G7 and Middle East leaders

- 06/16 0815 Weekly ADP (29k, --)

- 06/16 0830 Import price index MoM (1.9%, 1.0%)

- 06/16 0830 Export price index MoM (3.3%, 0.9%)

- 06/16 0830 NY Fed services (-5.8, --)

- 06/16 0830 Housing starts (1465k, 1430k)

- 06/16 0830 Building permits (1423k, 1418k)

- 06/16 0830 Chicago Fed’s final CARTS estimate

- 06/16 0855 Redbook Johnson retail sales

- 06/16 0900 Trump in working session with G7 leaders and development countries

- 06/16 1130 US Tsy to sell $65bn 6w bills

- 06/16 1300 US Tsy to sell $13bn 20Y bond re-open (912810UV8)

Source: Bloomberg, White House Pool, MNI

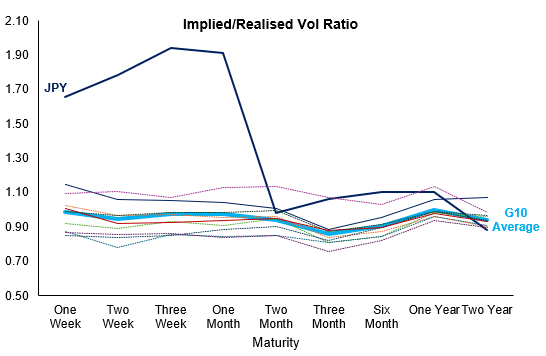

JPY: Vols Should Converge With G10 Average, But Argument for JPY Premium Remains

Jun-16 10:03

- Options trade following the BoJ decision has been generally healthy amid a quieter hedging market this morning. While the put/call notional ratio today is broadly balanced - the most salient trades of the day have been to the downside: puts wagered against 155.00, 158.00 strikes and trades consistent with a large 156.45 straddle stand out following the BoJ hike.

- With the BoJ decision now concluded, we'd expect the front-end of the JPY vol curve to converge with broader G10 after a period of dislocation that stemmed from USDJPY spot being pinned to Y160.00, which in turn pressured realised one-week vols to their lowest levels post-COVID.

Figure 1: Front-end of the JPY vol curve still trades with notable premium over G10 average

Source: MNI / Bloomberg Finance L.P.

- This should reduce the relative cost of JPY options in the near-term, and provide relief for a part of the curve that's been forced to price BoJ intervention risk, an oil price shock premium as well as political uncertainty through the first few months of Takaichi's premiership.

- That said, there remain notable drivers of near-term vol that still support a JPY vol premium, even if a reduced one. The BoJ's focus on FX passthrough for inflation, volatilty in longer-term JGB yields and lack of any spot rally on today's hike all still favour a more activist central bank - leaving USDJPY's anchor to Y160.00 looking fragile.

AUD: China Data Relatively Weighs on AUD Overnight, RBA Hike Prospects Alive

Jun-16 09:50

- While net adjustments across the G10 FX space have been contained on Tuesday, AUD has exhibited some moderate relative weakness, with overnight lows of 0.7042 taking us back to unchanged on the week. Importantly, the RBA decision had little to do with this and the moves look more a function of the China May activity data which was mostly on the softer side relative to market forecasts.

- Notably, China retail sales fell more than forecast, down 0.6%y/y (versus -0.2% forecast and 0.2% prior), the first decline since the end of 2022. This may lead to more efforts/calls for policy support in terms of the consumer sector.

- In terms of the RBA, Governor Michele Bullock stressed that monthly economic data remain volatile and should not be overinterpreted following Tuesday's decision to leave the cash rate unchanged at 4.35%, warning further rate increases cannot be ruled out.

- Short-term AUDUSD parameters appear well established approaching tomorrow’s Fed decision, with a downside focus on the June 11 low and short-term bear trigger at 0.6979. The 50-day EMA represents firm initial resistance, currently intersecting at 0.7107.