OPTIONS: US Options Roundup - Jul 17 2026

Friday's U.S. rates/bond options flow included: * TYQ6 108.50 puts ~8.8K given at 0-02, went offere...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FED: Chair Warsh Starts The Job With Extraordinarily Hawkish FOMC Meeting (1/3)

June's FOMC meeting was expected to deliver a hawkish hold, with the removal of the Statement's hiking bias, an increasing number of participants eyeing rate hikes by year-end, and new Chair Warsh repudiating forward guidance and laying out a framework of reforms in the months ahead. We got the rate hold at 3.50-3.75%, but the rest was at the hawkish extreme of the consensus scenario in almost every respect. It saw pricing for a 25bp rate hike pulled forward to October from early 2027 previously, and a new peak implied rate of 4.13% (up 19bp on the day) as Committee support for a future easing now appears all but dead.

- In the Dot Plot, half of the Fed funds Dots (9 members) eyed hikes by year-end (with 6 seeing multiple hikes) and just 1 saw a cut, with the median surprisingly rising from a hold at 3.625% (analysts had been unanimous on this) to a half-hike at 3.75%.

- The FOMC Statement was completely revamped and truncated, with a seeming emphasis on inflation fighting ("The Committee will deliver price stability"), and of course, no reference to forward guidance thus ending the long-standing easing bias.

- And the economic projections also included surprisingly robust medium-term underlying inflation expectations, with the core PCE median seen at 3.3% in 2026 Q4/Q4 vs 2.7% in March's edition, but surprisingly, 2027 also upped significantly to 2.5% from 2.2%.

- The Statement changes had Warsh's fingerprints all over them - he has advocated an end to forward guidance and less, not more, verbose communications. He said in the opening of his press conference that "It’s a bit shorter, a bit simpler—and it dispenses with some older language. That statement just gives you the facts, as best we can judge it. Absent, also, is so-called “forward guidance,” which we agreed was not well-suited to the current policy conjuncture."

- His fingerprints were not found on the SEP / Dot Plot, however - "It's been the practice of this committee for participants to submit [projections]. I have encouraged my colleagues to do so. I, however, refrained from offering any projections of my own, consistent with my long-held views on the SEP, at least as currently structured."

- That raised the question, where would Warsh's dot have been if he had submitted? On the evidence of the press conference, it didn't sound like he was an advocate of the next move being a cut, to say the least. Most of the content was very much hawkish, in contrast to some expectations that he would hew to a more dovish view than the median of the FOMC even if he didn't express an outright directional view on policy.

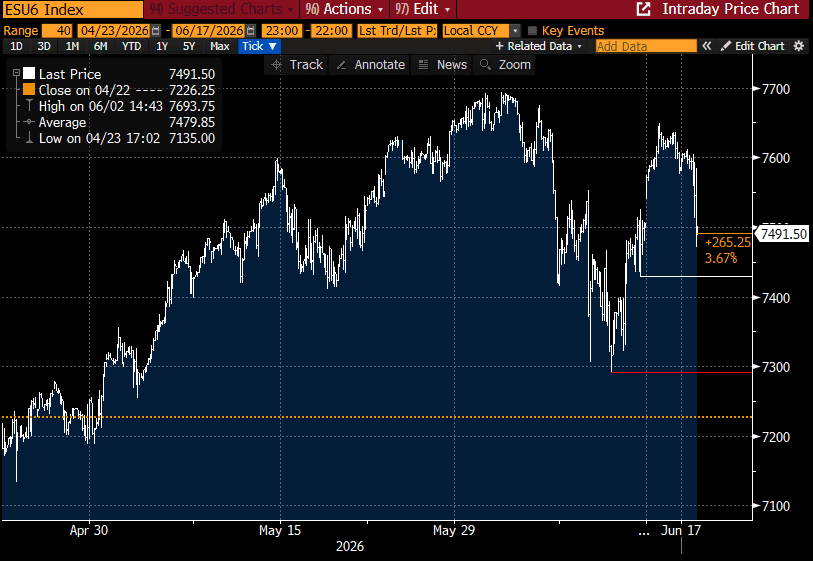

US STOCKS: [Correction] ESU6 Closes US-Iran Agreement Gap But Support Intact

Correction to the above, which should have referenced ESU6 rather than ESM6 – support hasn’t been cleared.

- ESU6, currently at ~7490 (-1.3%) off an earlier low of 7472.25, has fully reversed gains seen on Monday after the weekend’s US-Iran agreement.

- It hasn’t however tested support at 7429.00 (Jun 12 low), after which lies a key 7292.25 (Jun 11 low).

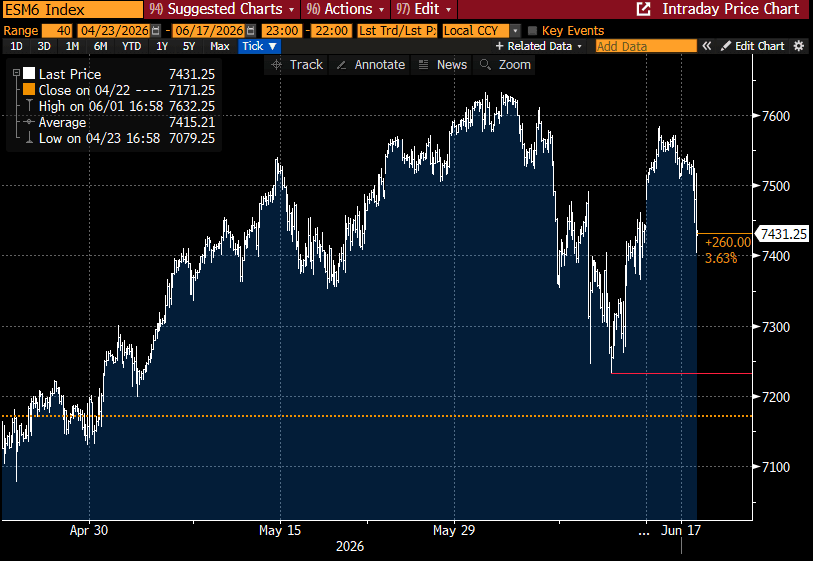

US STOCKS: S&P 500 E-mini Through Support, Opening Key Level If Sustained

- ESM6 has recently seen a small bounce to ~7430 (-1.2%) off earlier low of 7405.00, although earlier cleared support at 7429.00 (Jun 12 low) against the backdrop of sharply higher Treasury yields.

- If sustained it opens a key support at 7232.25 (Jun 11 low).

- Losses are seen across all major sectors within the SPX, led by communication services (-3.0%), consumer discretionary (-2.7%) and real estate (-2.5%).

- Industrials (-0.1%) are relative outperformers followed by financials (-0.5%).

- Some megacaps see heavy losses, led by Meta (-5.1%), Microsoft (-3.9%) and Amazon (-3.5%). Apple (-1.4%) and Nvidia (-1.5%) have been less prone.