LOOK AHEAD: US Macro Week Ahead: Wider Calendar

In addition to the ISM Services report and FOMC Minutes already discussed, some other data releases ...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

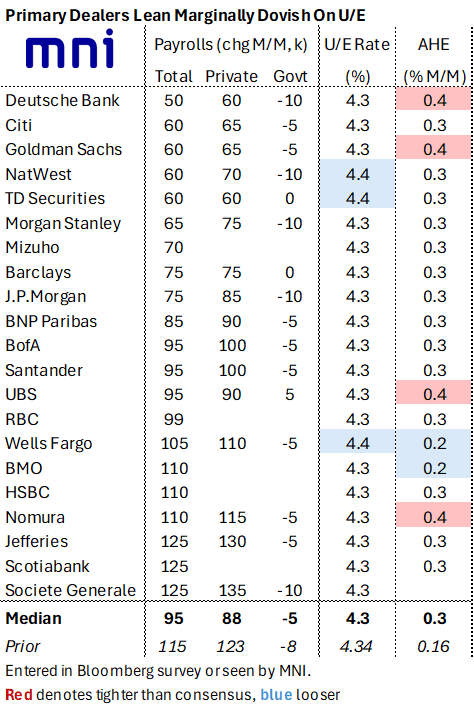

US LABOR MARKET: A Tighter Range To Primary Dealer Analyst Estimates For NFPs

- MNI’s survey of primary dealers shows a median expectation of 95k for nonfarm payrolls growth in May, a little stronger than the 85k currently seen for nonfarm payrolls.

- There’s a narrower range to estimates this month, from 50k-125k vs -15k to 135k in April.

- Highlighting the extent of the past two upside surprises, only Jefferies had a higher estimate than the realized 115k in April whilst the 178k initially reported for March (since revised to 185k) was higher than every primary dealer analyst.

- Back to May estimates, primary dealers may be more optimistic than broader consensus for nonfarm payrolls growth but they’re in line on private payrolls at 88k vs 87k for broader consensus.

- The unemployment rate is widely expected to round to 4.3% again, with a surprisingly small dovish skew to a 4.4% print considering it was 4.34% in April.

- There’s also relatively little divergence around the median expectation of a 0.3% M/M increase in AHE.

- See supporting comments behind these analyst estimates in the full MNI US Payrolls Preview, here.

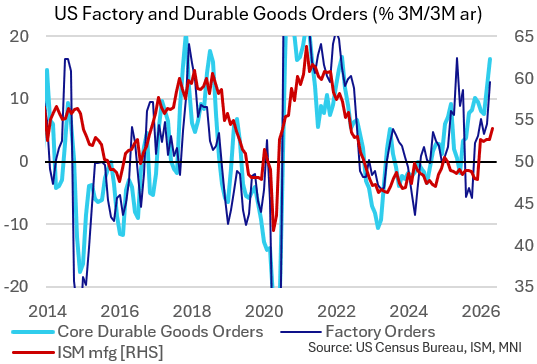

US DATA: Factory Orders Confirm Solid Gains In April

Solid headline/softer core April durable goods orders were roughly confirmed in the Full Report on Manufacturers’ Shipments, Inventories, & Orders, alongside a robust gain in factory orders. Overall the data merely reiterated what was known from the initial release, which is that there is no sign of a meaningful reversal in the continued momentum of business investment going into Q2.

- April's factory orders report showed a 4.8% M/M gain in headline (4.6% expected, 1.8% prior rev from 1.5%) and 1.3% ex-transportation (0.8$ expected, 1.8% prior rev from 1.6%). That was the best month for manufacturing orders since May 2025 and it's now growing at a near-13% 3M/3M annualized pace. That's largely due to soaring aircraft orders though ex-transport it was still very solid on the month, and up over 16% 3M/3M annualized.

- There were minimal revisions to the previously released durable goods orders (8.0% / 1.1% ex-transport) or capital goods nondefense ex-aircraft orders (-1.0%).

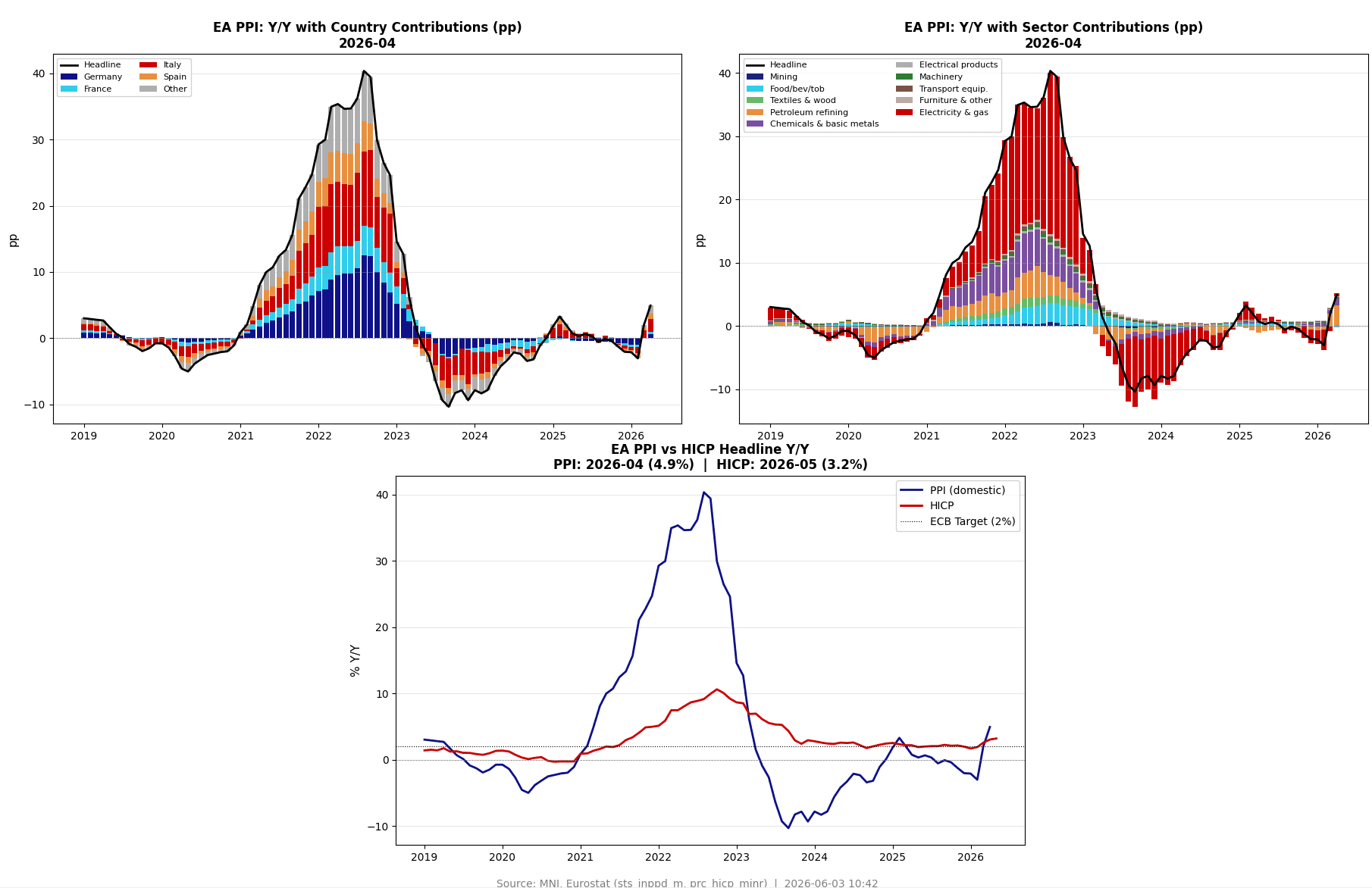

EUROZONE DATA: PPI Shows Signs Of Indirect Effects From Higher Energy

Eurozone April PPI came in in line with expectations today at 4.93% Y/Y, the highest rate since March 2023, as it accelerated from 1.98% Y/Y in March. Most importantly, the print shows signs of producers handing higher energy prices downstream somewhat in April.

- Energy PPI inflation rose to 12.29% Y/Y in April from March's 4.01% but with the acceleration notably driven by base effects as the category slipped -0.41% M/M compared to -7.7% M/M in Apr 2025 (that -0.4% M/M of course follows a particularly strong 11.0% M/M increase in March). Refined petroleum products increased 55.40% Y/Y (32.44% prior, highest since July 2022, 11.14% M/M), while electricity / gas / utilities saw base effects drive up their yearly rate to 1.56% Y/Y (-2.97% prior) amid a 4.59% sequential fall.

- PPI excl. energy and also water supply also accelerated in April to its highest rate since June 2023 at 2.27% Y/Y (1.43% prior), in our view a sign of some indirect effects on broader input costs from the energy price surge. This was to be expected at some stage as producers hand these costs downstream, and represents a distinct dynamic to so-called second-round effects, which ECB officials have repeated today are not visible yet.

- Non-energy details see various rising at their highest Y/Y rates since 2023 rather than the overall acceleration being down to a single item jumping. For example, metals (basic + fabricated) increased 5.65% Y/Y in April (4.87% prior, 0.83% M/M), machinery 2.18% Y/Y (1.68% prior, 0.50% M/M), and rubber / plastics / minerals 2.37% Y/Y (0.82% prior, 1.62% M/M).

- Across countries, PPI picked up across all 'big 4' in April: Germany saw a 1.89% Y/Y rate (0.00% prior), France a 2.07% rate (also 0.00% prior), while Italy and Spain see more pronounced pressures currently, at 8.78% (5.39% prior) and 8.20% (3.10% prior), respectively.