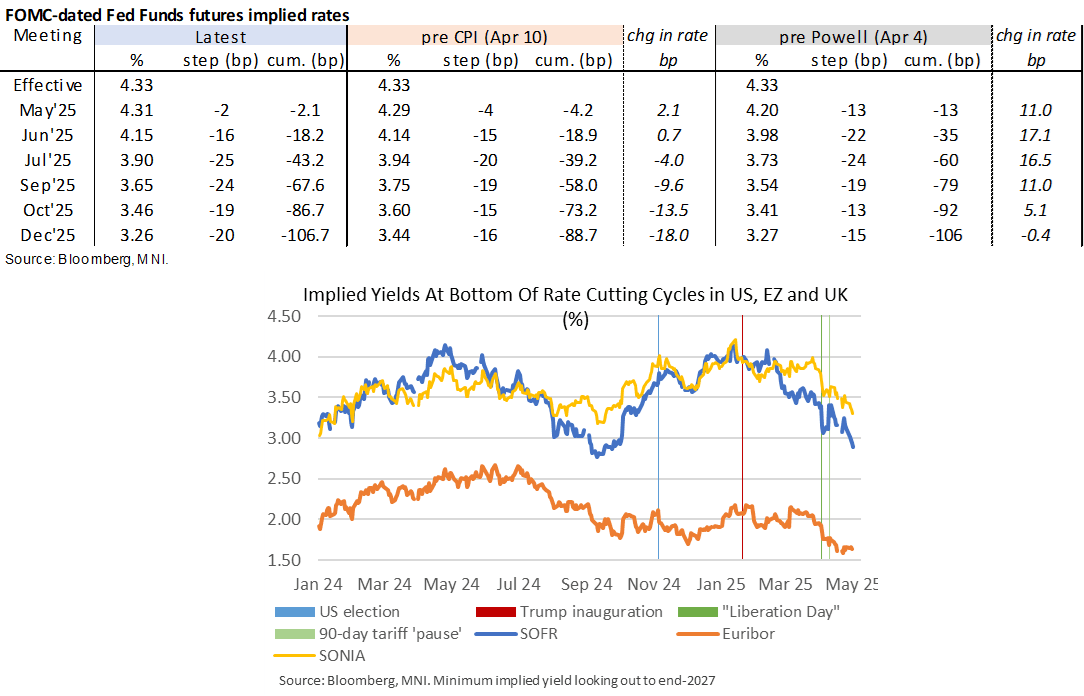

STIR: Trend Decline In US Implied Rates Continues

May-01 13:44

- Fed Funds implied rates have pared some of the decline on higher than expected jobless claims but nevertheless extend the trend decline seen this week.

- The initial retracement is down to the caution needed with initial claims capturing the week after a late Easter but downward pressure is maintained by the pop to new cycle highs for continuing claims.

- Cumulative cuts from 4.33% effective: 2bp next week, 18bp Jun, 43bp Jul, 68bp Sep and 106.5bp Dec.

- Terminal implied yields in SOFR futures are 5bp lower on the day at 2.89% (SFRU6), new lows since September and some 50bp lower than pre Apr 2 “Liberation Day” levels.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EQUITY TECHS: E-MINI S&P: (M5) Key Support Remains Exposed

Apr-01 13:39

- RES 4: 5886.86 50-day EMA

- RES 3: 5837.25 High Mar 25 and a key resistance

- RES 2: 5766.74 20-day EMA

- RES 1: 5672.75 High Mar 31

- PRICE: 5640.50 @ 14:28 BST Apr 1

- SUP 1: 5559.75/33.75 Low Mar 13 and the bear trigger / Low Mar 31

- SUP 2: 5500.00 Round number support

- SUP 3: 5483.50 2.00 proj of the Dec 6 ‘24 - Jan 13 - Feb 19 swing

- SUP 4: 5396.00 2.236 proj of the Dec 6 ‘24 - Jan 13 - Feb 19 swing

S&P E-Minis maintain a softer tone following recent bearish price action. Attention is on key support and the bear trigger at 5559.75, the Mar 13 low. It has been pierced, a clear break of it would confirm a resumption of the downtrend that started Feb 19, and open 5483.30, a Fibonacci projection. MA studies are in a bear-mode position, highlighting a dominant downtrend. Key short-term resistance has been defined at 5837.25, the Mar 25 high

EQUITIES: US Cash opening calls

Apr-01 13:25

SPX: 5,606.9 (-0.1%); DJIA: 41,899 (-0.2%/-103pts); NDX: 19,258.1 (-0.1%).

EUROPEAN INFLATION: SA Data Suggests Elevated Pace Despite NSA Deceleration

Apr-01 13:15

Sequentially, SA services prices rose 0.27% M/M - almost in line with the 0.29% M/M average seen since December.

- In annualized terms, this would mean a current services pace of around 3.5%. Although annual NSA services inflation was slightly weaker-than-expected at 3.42% Y/Y (vs 3.5% MNI consensus, 3.68% prior), the seasonally adjusted data suggests that underlying price pressures still remain elevated.

- Eurozone services inflation momentum rose to 3.23% on a 3m/3m seasonally adjusted and annualised basis (using ECB data), the second consecutive increase after an eight-month streak of decelerations - underscoring questions some analysts had raised before on residual seasonality in the data. Momentum rose last Spring, too.

- For hawkish ECB policymakers (nowadays led by Executive Board member Schnabel), this development will underscore the need for a more cautious approach to policy further ahead - especially if the governing council goes ahead with an April cut, as appears to be markets' base case as of now.

- Non-energy industrial goods momentum ticked up to 0.75% (vs 0.68% prior), with sequential prices flat M/M (vs 0.12% prior).

- Taken together, this left core inflation momentum at 2.34% (vs 2.22% Feb, 1.85% Jan).