ARGENTINA: Trade Surplus Rises To $906mn In June, Above Expectations

Jul-17 19:02

- "*ARGENTINA JUNE TRADE SURPLUS $906M; EST. +$700M" - BBG

- "*ARGENTINA JUNE EXPORTS $7.275B"

- "*ARGENTINA JUNE IMPORTS $6.370B"

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

COMMODITIES: Crude Extends Gains Amid Mounting Geopolitical Tensions

Jun-17 19:01

- Crude has extended gains after US administration rhetoric late in the day raised the prospects of US direct involvement in the Iran-Israel conflict.

- WTI Jul 25 is up by 4.9% at $76.8/bbl, taking gains over the last week to over 15%.

- Several military analysts and reporters have interpreted VP JD Vance's recent social media post as laying the groundwork for President Trump to authorise the use of 'bunker buster' bombs to strike Iran's Fordow nuclear facility.

- The sharp rally in WTI futures marks an acceleration of the current bull phase. Price action is likely to remain volatile near-term, and from a technical standpoint, the trend is currently in an extreme overbought position.

- A continuation higher would expose the $80.00 handle, followed by $81.93, a Fibonacci projection.

- Meanwhile, spot gold is little changed at $3,383/oz.

- A bullish theme in gold remains intact, with initial resistance at $3,451.3, the Jun 16 high. Initial key support to monitor is $3,271.7, the 50-day EMA.

- By contrast, silver has rallied by 2.0% today to $37.0/oz, taking the precious metal to a new multi-year high. As a result, the gold-silver cross has fallen to 91.4, close to recent 2-month lows.

- A bull wave in silver remains in play, with sights on $37.195 next, a Fibonacci projection, which was pierced earlier. A clear break would open $37.478, the March 2012 high.

EURJPY TECHS: Northbound

Jun-17 19:00

- RES 4: 169.91 1.236 proj of the Feb 28 - Mar 18 - Apr 7 price swing

- RES 3: 168.58 2.0% 10-dma envelope

- RES 2: 168.01 High Jul 26 ‘24

- RES 1: 167.61 High Jun 17

- PRICE: 167.35 @ 15:50 BST Jun 17

- SUP 1: 165.91/164.69 Low Jun 16 / 20-day EMA

- SUP 2: 163.48 50-day EMA

- SUP 3: 162.80/161.78 Low Jun 3 / Low May 26

- SUP 4: 161.09 Low May 23 and key support

The trend set-up in EURJPY remains bullish and Monday's strong start to the week reinforces current conditions. Moving average studies remain in a bull-mode position, highlighting a dominant uptrend. 167.47, 61.8% of the Jul 11 - Aug 5 ‘24 bear leg, has been pierced. This signals scope for a climb towards 168.01 next, the Jul 26 ‘24 high. Initial support to watch lies at 164.69, the 20-day EMA.

US OUTLOOK/OPINION: Weak Restaurants Drive Pullback In PCE Estimates

Jun-17 18:58

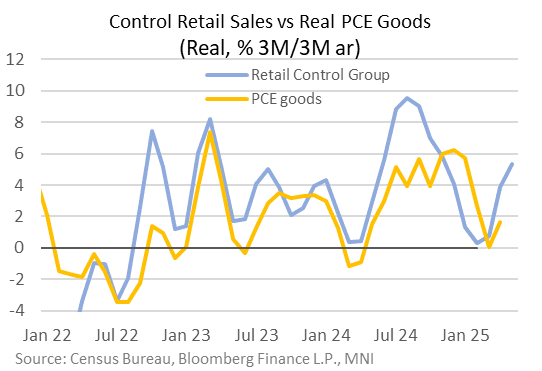

May's sequential retail sales decline sees nominal sales down for a 2nd consecutive month, but the Control Group was actually quite solid, beating expectations at 0.4% M/M and suggesting that the GDP impact of the report may be relatively limited.

- We note that today, the Atlanta Fed substantially lowered its estimate for Q2 real personal consumption expenditure (PCE) growth, to 1.9% Q/Q SAAR from 2.5% prior to this release. However real goods consumption was seen holding up relatively well, at 2.9% (a slight downgrade from 3.0% in the prior estimate).

- That's in line with what appears to be a modest pickup of Control Group momentum in May - the grouping being helped by excluding auto and gasoline among other categories which were weak (in nominal terms at least) in the month. It appears to be running at around 4.1% 3M/3M annualized, though a little stronger than that on a real basis due to recent soft non-vehicle core goods price inflation.

- In fact, the Atlanta Fed's downgrade to Q2 PCE was due almost entirely to PCE services: they slashed their growth forecast to 1.5% for the quarter from 2.2% prior. PCE goods had been seen contributing 0.6pp to GDP in the quarter, and that hasn't changed; PCE Services' expected contribution has dropped from 1.1pp to 0.7pp.

- This in turn looks driven by food services and drinking places - the only services category in retail sales - whose fall of 0.9% (biggest drop in 27 months) in May's retail sales report was a bit of a shock after strength in the prior two months (though Atlanta Fed GDPNow overall sees real PCE services ex-food services slowing in May as well). "Food services and accommodations" is over 10% of PCE services spending.

- However the strong March/April restaurant retail sales (2.5%, 0.8%) have the series running at a solid 10.6% quarterly pace of growth in May, so a major pullback in Q2 is hardly assured, at least by our calculations.

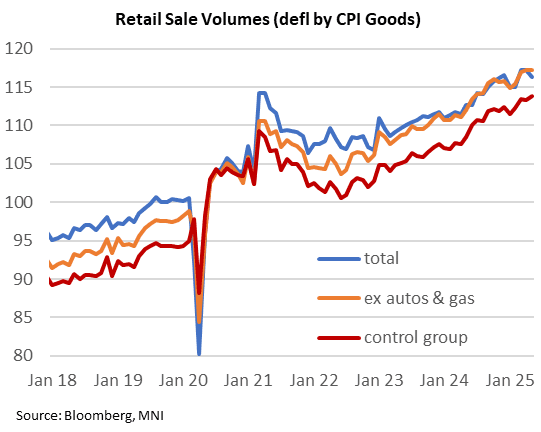

- Overall, "real" (deflated by CPI goods) retail sales volumes remain in an uptrend, notably core (ex-auto/gas and Control Group). We will watch the May PCE report at end-June with great interest to see how broader consumer dynamics are faring.