EM LATAM CREDIT: Telecom Argentina- Tap New Deal

(TECOAR; Caa1 /B- /B)

$200m WNG 9.25% 2033

IPTs: 9-9.125%

FV: 9% Area

• Telecom Argentina Tapping USD200mn WNG the 9.25% 2033 (7.35Y WAL) senior unsecured amortizing notes. Use of proceeds will be to repay loans related to the acquisition of Telefonica Moviles Argentina from Telefonica of Spain.

• TECOAR 2033 notes were quoted 8.86%, issued at 9.5% May 2025. Argentina energy company Pampa Energia (PAMPAR; Caa1 /B- /B-) has a significant portion of EBITDA derived from regulated businesses, electricity and gas pipeline, with 2031 notes at 7.47% YTM. TECOAR 2031s were quoted 8.35%, so 88bp wider. PAMPAR 2034s were quoted 7.93% so applying that 88bp leads to 8.81%.

• At the time of the initial issuance of TECOAR 2033s, TECOAR 2031s were quoted at about 106bps wide to PAMPAR 31s. PAMPAR 2034s were at 8% so TECOAR 33s were issued 150bp wide at 9.5%.

• A lot of that was new issue concession in placing a relatively large USD800mn deal size as well as event risk from the company’s acquisition of Telefonica Moviles Argentina which has run into some regulatory objections. As the company is only looking to place USD200mn less concession should be required and the company did recently get some support on the legal front.

• The Argentina government announced it would conduct a review of the transaction with concerns about a monopoly in the telecom market. Telecom Argentina projected a 58% market share of the Argentina mobile telecom market but would lag competitors in other businesses such as Broadband and fixed line.

• In June Telecom Argentina won a legal victory with the Federal Court of Appeals allowing the company to proceed with operational integration of the acquisition but still regulators are reviewing the transaction as the government is concerned about lack of competition.

• Telecom Argentina has the second highest market share behind Mexico based America Movil’s Argentina subsidiary and ahead of Telefonica’s Argentina subsidiary according to the company. The balance sheet was also reasonably leveraged, reported at 1.9x net debt/EBITDA 1Q 2025.

• Telefonica of Spain is seeking to divest all its Latin America subsidiaries except Brazil and announced February 2025, that it was selling its Argentina subsidiary for USD1.25bn to Telecom Argentina which would result in a merger of the number 2 and 3 operators in the country.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

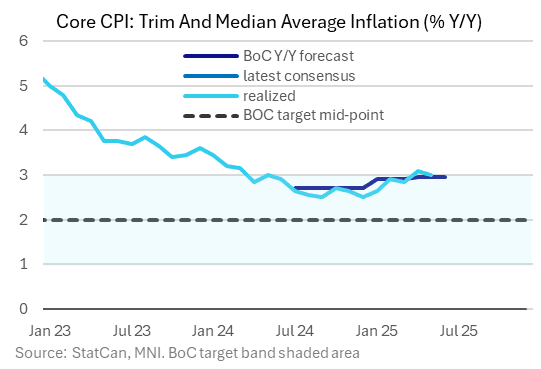

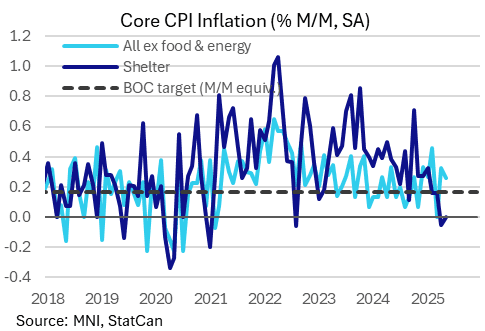

CANADA: Limited May Disinflationary Progress Doesn't Firm July BOC Cut Case

Market-implied pricing for a 25bp BOC cut in July dipped to around 32% from 40% prior to the largely in-line CPI report. As for the rest of the year, pricing through December is unch at 32bp, though there's just slightly less of an implied full cut through October (23bp vs just under 25bp pre-CPI).

- We think there had been some anticipation that May's readings could clarify that April's surprisingly hot report had largely been driven by volatility rather than broader underlying factors, but even if core metrics pulled back largely across the board, it's not clear recent stubbornness can so easily be dismissed by the BOC. Indeed, May's report looked broadly similar to April's. Another CPI report - namely June's on July 25 - will probably be required barring clear deterioration in activity/labour market data.

- The headline Y/Y reading of 1.73% unrounded was barely changed from 1.74% prior, though the 0.6% M/M upside surprise was very close to rounding down vs 0.5% consensus (was 0.551%, after -0.06%). As noted previously, the weighted median/mean average of 3.0% Y/Y was in line with expectations (3.1% prior downward rev from 3.15%).

- In headline CPI, food prices at 3.4% Y/Y were in line with expectations of a pullback from 3.8% prior, with energy's -11.0% Y/Y (-12.7% prior) perhaps a little less deflationary than had been expected.

- Core goods (ex-food purchased from stores / energy) picked up to 1.3% Y/Y from 0.9% prior for the fastest since January 2024, led by the fastest durables print since Apr 2023 (2.0% Y/Y after 1.7%) with semi-durables and nondurables prices also picking up. Passenger vehicle prices picked up to 3.2% from 2.9%.

- We'd seen mixed views on the degree to which core goods would accelerate (TD forecast 1.5%), though the overall takeaway will be that deflation in this category is over, whether that's largely tariff-related or not.

- Overall services prices inflation decelerated to 3.2% from 3.5% prior, which while largely in line with expectations means we have only seen one sub-3.0% print since 2021. While household operations and recreation were relatively firm, shelter prices continue to lead the recent deceleration: overall shelter down to the lowest since early 2021 at 3.0% Y/Y (3.4% prior), with rents at 4.5% (5.2% prior) and owned accommodation 3.2% (3.5% prior). Travel and tours - which BOC's Macklem has repeatedly highlighted in April's report as an outlier - pulled back to -0.2% Y/Y (from +6.7% prior), with overall travel services pulling back to -0.3% from 2.9%.

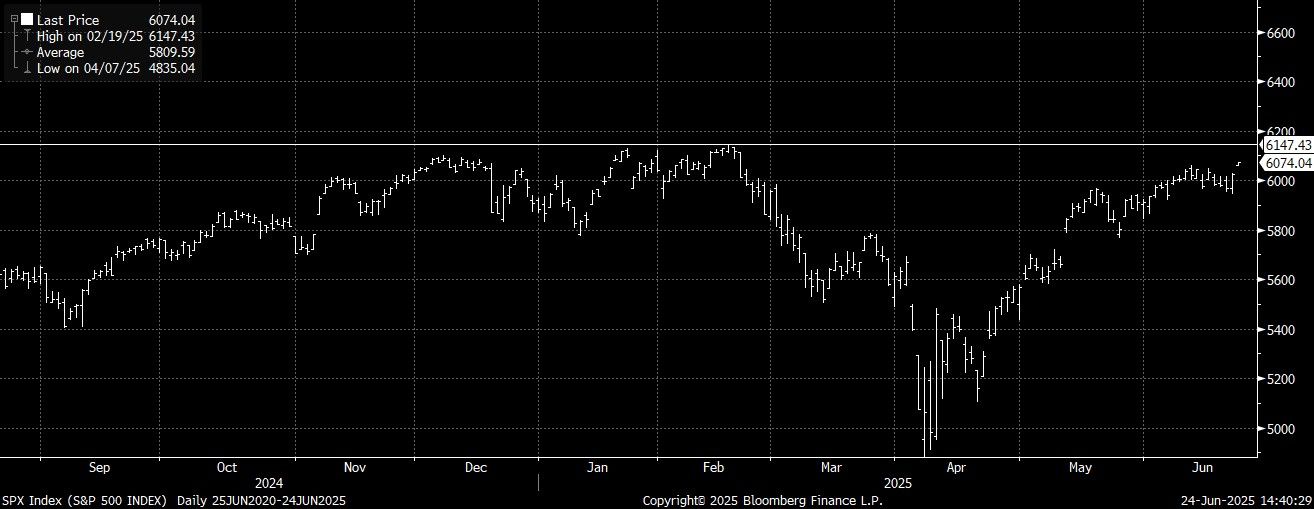

EQUITIES: US SPX fully clears the June high

- Although US Cash Indices have opened slightly below the Opening calls, the SPX has fully cleared the June High, and is reaching its highest level since February.

- The all time record high is still much further out, and would need a test up to 6147.43, the 19th February high.

- There was a program buyer, but just 1224 names, late Yesterday saw a 1672 names.

- NDX also trades at its best level seen since February, the all time record high is situated at 22,222.61, now at 22,094.28.

(Chart source: Bloomberg Finance LP/MNI).

BOE: Ramsden: Vote "finely balanced" but 4% "clearly in restrictive territory"

Other highlights from his vote decision:

- "Before finalising my vote I challenged myself on whether sequential cuts in Bank Rate in May and June would be appropriate if it subsequently became clear that risks to inflation were actually weighted to the upside. It was a finely balanced judgement for me but I concluded that my approach was robust for two main reasons."

- "First because even at 4% I assess that monetary policy would remain clearly in restrictive territory. So if evidence emerged that pointed to higher inflation in the medium term then Bank Rate could be held higher for longer than would otherwise be the case."

- "Second given the environment we are operating in I think it is important that monetary policy is outlook dependent and should respond and be seen to respond when the evidence on the outlook requires it."

- "I continue to take a watchful and responsive approach to setting policy. I think this is in line with the emphasis the MPC puts in its collective communications on policy not being on a pre-set path and that we will consider the degree of restraint which is required from meeting to meeting."

- "I see no inconsistency with my latest vote and the MPC’s gradual and careful approach to the withdrawal of restrictiveness. This has served the MPC well over the last year as we have cut Bank Rate four times by a total of 100bps in total. And I believe it will continue to serve us well in these times of increased uncertainty and unpredictability, as long as the disinflation process is judged to be continuing, in order to return inflation back to the 2% target sustainable in the medium term."