US STOCKS: Soft Data Keeps Stocks Bid

The ESM5 Overnight range was 5867.00 - 5944.50, Asia is currently trading around 5935. This morning risk is opening up relatively flat in Asia after a decent close in the US session after some soft data.

- Bloomberg TV - “Jamie Dimon did an interview stating a recession remains a possibility due to tariff fallout, he also stated that some clients are holding back on investments due to market volatility caused by the Trump administration’s tariff policies.”

- “A reprieve in trade tensions is showing up in shipping rates. The cost for a 40-foot container from Shanghai to New York surged 19.3% from the previous week to $4,350, the sharpest weekly advance since January 2024. The Shanghai-to-Los Angeles route gained 15.6%, the biggest jump this year.’(BBG)

- “A continued bid from systematic funds and corporate buybacks, along with increased bullish option positioning, also means the S&P 500 can push higher from here.”(BBG)

- The dip in US Stocks was short-lived after some soft data overnight causing the market to look for rate cuts to head off a recession. Listening to the Fed speakers though it's hard to see cuts materializing until this so-called recession actually comes to fruition.

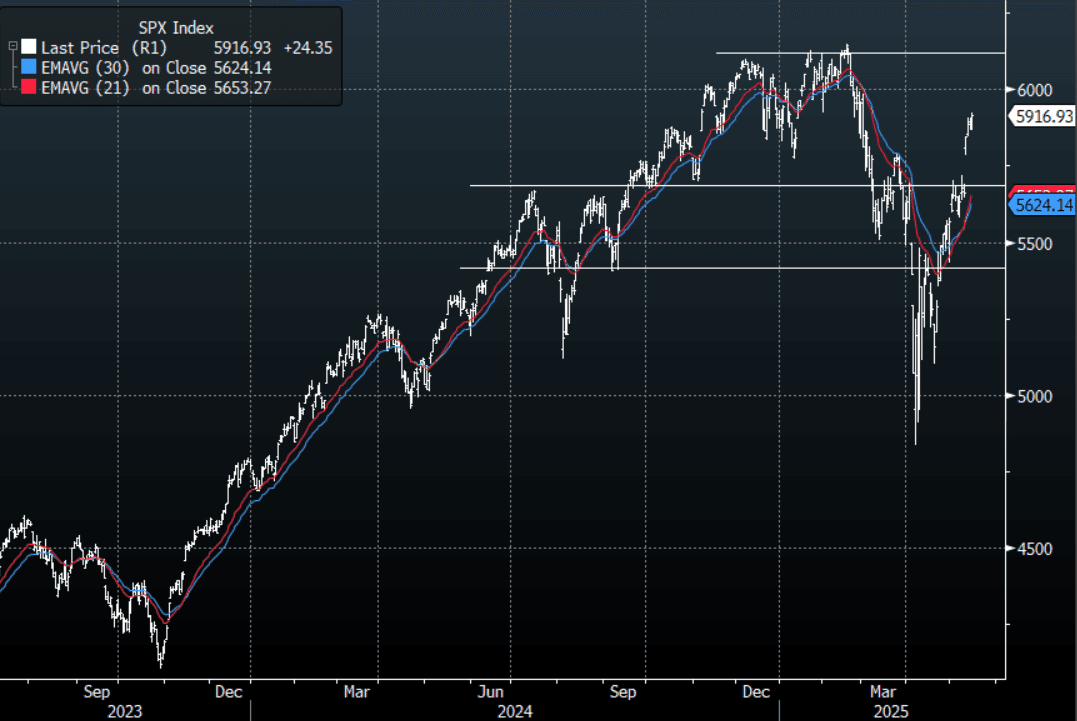

- The SPX has had a huge bounce from its lows on a 4800 handle, this has left a generally bearish market completely wrong-footed. In the short-term though this move is starting to look a little overdone.

- Look for demand to materialize once more back towards the 5700 area as momentum funds and corporate buybacks dominate the flow for now.

This move could still have more to go as the conviction of the bears is challenged but look for sellers to return back above 6000 again as the concerns regarding Global growth and the re-allocation out of US Assets have not gone away.

Fig 1: SPX Daily Chart

Source: MNI - Market News/Bloomberg

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JAPAN DATA: Machine Orders Above Forecasts, But Y/Y Momentum Still Slows

Japan core machine orders for February were stronger than expected. In m/m terms the print was +4.3%, against a 1.2% forecast and -3.5% prior. This saw the y/y outcome at 1.5%, against a -0.9% forecast and 4.4% prior. The y/y pace remains well off late 2024 highs above 10%. The chart below plots the y/y core machine orders (the white line on the chart) versus Japan Capex y/y (ex software). The softer machine orders pace is still implying further easing in capex momentum.

- Looking at the manufacturing, non-manufacturing split, we had positive rises for both segments. Foreign orders were up 3.4%m/m as well.

- This data comes ahead of Q2 tariff announcements though, which will impact the Japan economy. Key government members are looking at negotiating a trade deal with the US, but a cloud remains over the outlook

- BoJ Governor Ueda also talked to a local newspaper, stating that the tariff outlook was moving towards the 'bad scenario' in terms of what the central bank envisaged (via Sankei/Rtrs).

- Hence data beats like today are unlikely to shift market thinking much around the BoJ rate path.

Fig 1: Japan Core Machine Orders & Capex Y/Y

Source: MNI - Market News/Bloomberg

US TSYS: Cash Open - Quiet Start

TYM5 is trading 110-31+, - 0-03 from its close. Yields finding further relief heading into a long weekend.

- Cash US tsys are flat to 2bps richer, with a steepening bias.

- The US 10-year yield has opened around 4.33%.

- Risk has stabilised and US yields continued to benefit as Deputy Treasury Secretary Michael Faulkner said officials are discussing a move to loosen bank regulations and allow lenders to keep more Treasuries on their balance sheets.

- The real yield curve has steepened notably in recent weeks, suggesting the market, like the Fed, continues to see inflation risks ahead.

- The Feds Cook did not comment on Monetary policy in his prepared text after the US close.

- Jerome Powell is to speak about the economic outlook later today, the market will be closing attention to this.

- The 10-year yield will continue to find sellers on dips, expect dips back towards the 4.25/4.30 area in the 10-year to find supply.

- Data: Retail Sales, Industrial Production, Capacity Utilization and NAHB Housing Market Index.

BOJ: Ueda States US Tariffs Moving Towards 'Bad Scenario'

BoJ Governor Ueda has commented to local newspaper Sankei, noting the central bank will have to monitor the tariff impact and may need to respond if the economy is impacted. Below are some of the key takeaways, which come via Reuters.

- "Bank of Japan Governor Kazuo Ueda said the central bank may need to take policy action if U.S. tariffs hurt the Japanese economy, the Sankei newspaper reported on Wednesday"

- "Since February, risks surrounding U.S. President Donald Trump's policies have "moved closer towards the bad scenario" the BOJ had envisioned, Ueda said in an interview"

- "Ueda said the BOJ will continue to raise interest rates "at an appropriate pace" if economic and price developments move in line with its projections.

- "But we will scrutinise without pre-conception the extent to which U.S. tariffs could hurt the economy," he said. "A policy response may become necessary. We will make an appropriate decision in accordance with changes in developments." (Rtrs)

- The next BoJ policy meeting concludes in at the start of May. Market expectations for rate hikes have been sharply scaled back over the past month in response to President Trump’s announcement of reciprocal tariffs. Markets now assign a 0% probability to a 25bp hike at the May meeting,

with a cumulative 50% chance not priced in until December. - This marks a significant shift from just a month ago, when a full hike was priced by October and a 50% probability was expected by June.