STIR: SOFR Futures Update

Aug-02 16:22

- Mirroring steeper Treasury curves, Secured Overnight Financing Rate 3M futures are holding firmer levels in Whites to Reds at the moment, Blues to Golds weaker.

- Front month Sep'23 SOFR futures are currently trading steady at 94.59 (3M SOFR settled +0.00306 to 5.36941 (-0.00250/wk)). The balance of Whites through Reds (SFRZ3-SFRM5) are trading +0.030-0.045, Greens (SFRU5-SFRM6) +0.030 to -0.010, Blues-Golds (SFRU6-SFRM8) -0.015-0.055.

- Rate hike projections through year end remain subdued, Sep 20 FOMC is 17% w/ implied rate change of +4.3bp to 5.371%. November cumulative of +9bp at 5.419, December cumulative of 5.3bp at 5.32%. Fed terminal holding at 5.42% in Nov'23.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US: Independence Day Exchange Schedules

Jul-03 16:20

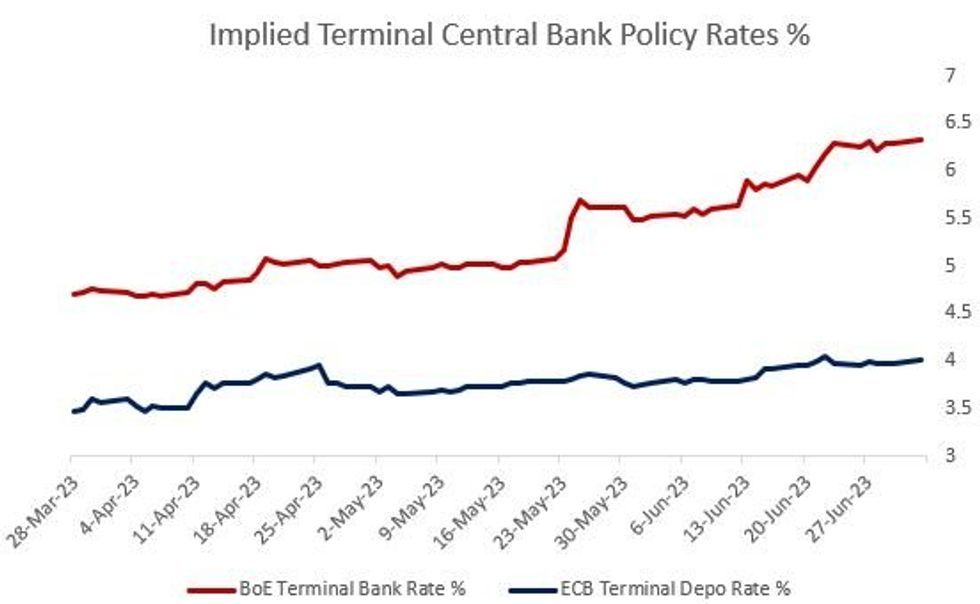

STIR: ECB Peak Pricing Back Above 4%, BoE Fresh 2023 High

Jul-03 16:11

ECB and BoE hike pricing faded from intraday peaks but overall picked up sharply to start the week, despite soft Eurozone (notably Italian PMI) data, with a weak US ISM Manufacturing reading pulling global tightening expectations back from session highs.

- ECB terminal depo Rate pricing +4.2bp to 4.01% (52bp of further hikes left in the cycle to Dec 2023): After closing stubbornly below 4% in each session last week, amid the Sintra summit and Euro inflation data, ECB terminal pricing closed above that mark today for the first time since June 22nd. The intraday peak was around 4.05%. Bundesbank's Nagel was the only speaker of note, and he was characteristically hawkish, pointing out the ECB's hiking cycle has "some way to go". As MNI noted last week, core / services inflation momentum remains strong, suggesting that a 25bp hike in September is more likely than not at this point.

- BoE terminal Bank Rate pricing +3.6bp to 6.29% (129bp of further hikes left in the cycle to Mar 2024) BoE pricing hit an intraday peak of 6.35%, not quite piercing the 2022 mini-budget crisis highs but a 2023 high. 45bp is priced for the August MPC.

US STOCKS: Equities Roundup: Strong Auto Unit Sales Lifts Consumer Discretionary

Jul-03 15:56

- Stocks trading mildly lower, near the middle of a narrow range on a shortened pre-holiday session. Currently S&P E-Mini futures up 52.5 points (-0.03%) at 4489.5, DJIA up 285.18 points (-0.11%) at 34454.43, Nasdaq up 196.6 points (0.1%) at 13783.72.

- Leading gainers: Real Estate, Energy and Consumer Discretionary sectors outperforming in the first half. Consumer Discretionary sector led by auto makers after strong unit sales reports: Tesla off highs is still trading +6.23% higher ahead the early close, GM +1.25%, Ford +0.85%. Real Estate sector buoyed by a combination of hotel/resort and office real estate investment trusts.

- Laggers: Health Care and Information Technology sectors underperformed, the latter weighed by weaker software and services shares: Oracle -1.57%, Intuit -1.54%, Adobe -1.35%.

- The technical/bull theme in S&P E-minis remains intact and Friday’s gains reinforce this condition. The contract has pierced key resistance and the bull trigger at 4493.75, the Jun 16 high. A clear break of this level would confirm a resumption of the uptrend and pave the way for a climb towards 4532.08, a Fibonacci projection. On the downside, key trend support has been defined at 4368.50, the Jun 26 low.