SOUTH KOREA: SK STIR - S/T Rates Point to Rate Hike

Jun-17 02:39

* Short term interest rates continue to build in rate hike expectations in Korea with the upgrade ...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

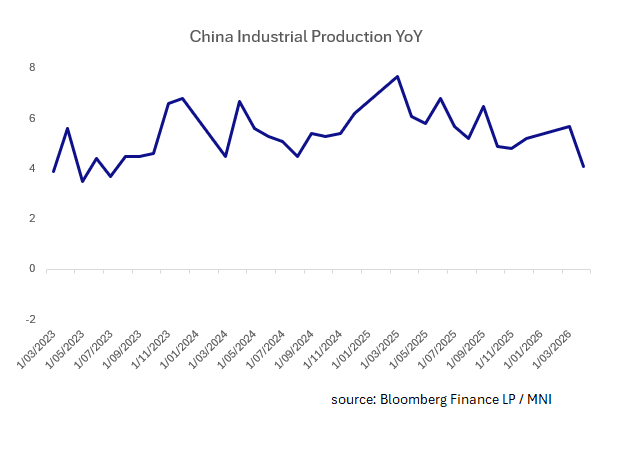

CHINA: Industrial Production Decline Likely Symptomatic of Oil Shock

May-18 02:39

- China's Industrial Production increase rose by +4.1% in April, the slowest increase since July 2023.

- On an industry basis, the largest declines were in Pharmaceutical, mining whilst the largest increases were in the auto sector and telcos/communications.

- Strong exports have been supporting the economy from the impacts of the Iran war even though the adverse consequences of higher oil prices are playing out on factory floors as manufacturers cope with surging raw material costs.

- Whilst for some observers might suggest the need for immediate monetary policy relief, this looks more like a natural reaction to the oil price shock and at +4.1% is only marginally down from the 5-year average of +4.9%

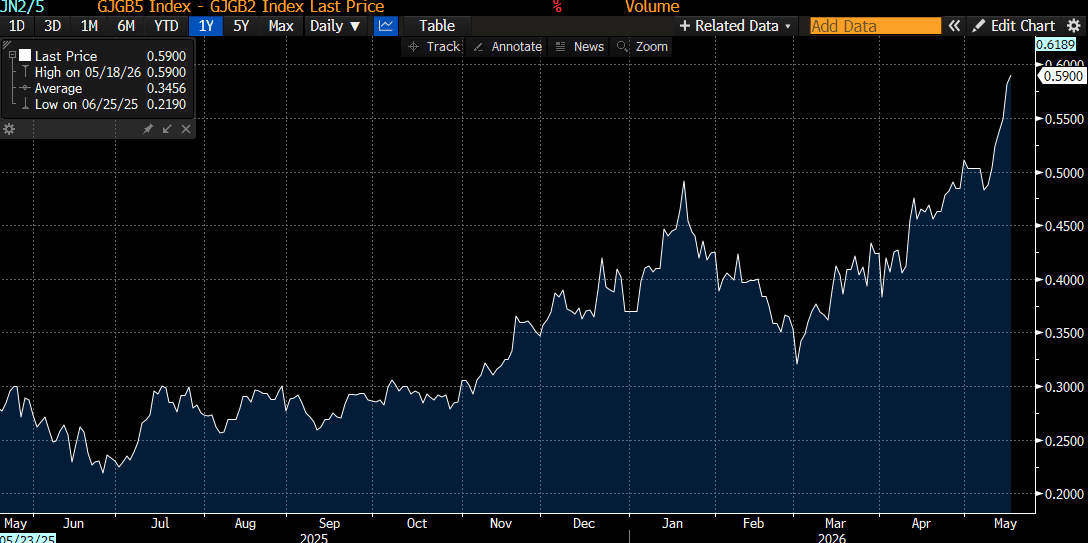

JGBS AUCTION: 5Y Supply Faces Higher Yield & Steeper Curve

May-18 02:30

The Japanese Ministry of Finance (MoF) will today sell Y2.5tn of 5-Year JGBs. MoF last sold 5-year debt on 9 April 2026.

- The yield on today’s offering is 20bps higher last month’s level and sits at a fresh cycle high.

- JGB yields have risen global bond yields on inflationary concerns. That said, the rise in JGBs also likely reflects renewed concerns over the nation's fiscal policy.

- "Japanese Prime Minister Sanae Takaichi is set to announce plans soon to compile an extra budget in response to rising commodity prices driven by the ongoing Middle East conflict, according to people familiar with the matter." - BBG

- The 2s/5s curve is at a cycle high, steepest since 2006.

- Amid weak at recent auctions, today’s results will be closely watched for signs of continued weakness.

- Results are due at 0435 BST / 1235 JST.

Bloomberg Finance LP

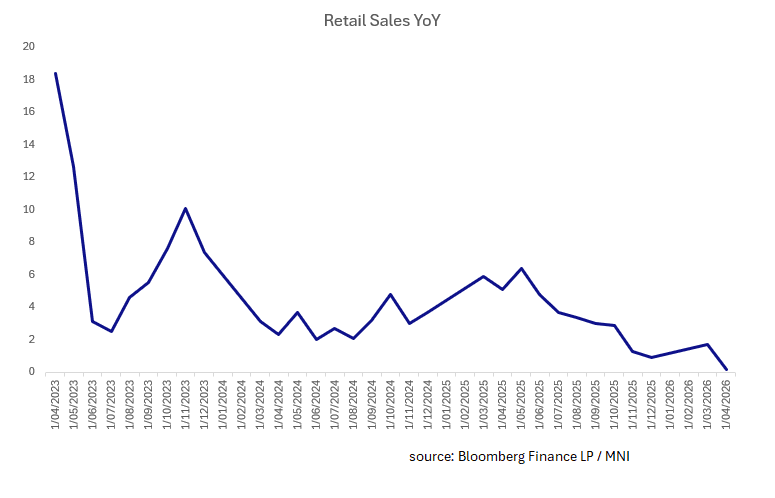

CHINA: Retail Sales Weakest Since 2022

May-18 02:27

- China's April retail sales recorded the slowest expansion since December 2022, rising just +0.2%

- Autos, construction materials, petrol products, household electronics and jewelry all posted significant falls

- China’s April retail sales reinforces that the consumer side of the economy remains under significant pressure even whilst exports and industrial production are holding up relatively well.

- China's consumers continue to agonize over falling property prices, soft wage growth, job insecurity and weak household wealth effects.

- Consumers are shifting toward services, not goods with some positive signs (for spending) in travel, restaurants, entertainment and services.

- Weak retail sales increases the pressure on Beijing and the PBOC to deliver additional support measures later this year, particularly targeted consumption stimulus or property-sector easing