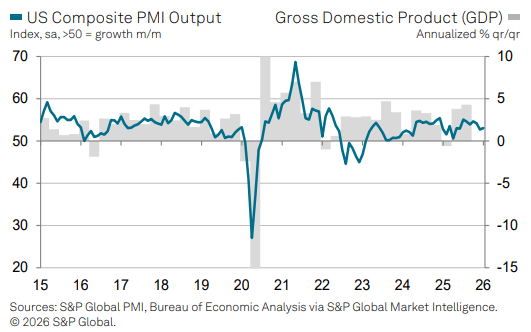

US DATA: Services PMI Follows Manufacturing With Upward Revision In January

The services PMI was revised up 0.2pp to 52.7 in the final January release after Monday's more sizeable 0.5pp upward revision to the final manufacturing release to 52.4. It left the composite PMI at 53.0 in January after 52.7 in December although it has still moderated from the 54.5 averaged through Jul-Nov 2025.

- S&P Global US Services PMI: 52.7 (cons & flash 52.5) in Jan final after 52.5 in Dec and 54.1 in Nov

- S&P Global US Composite PMI: 53.0 (cons 52.9, flash 52.8) in Jan final after 52.7 in Dec and 54.2 in Nov

The PMI press release highlights (full release, here) look broadly similar to the flash although a clearer discussion on the reduction in foreign demand here:

- “January’s S&P Global PMI survey of US private service sector companies signaled a quicker expansion of business activity. Stronger growth was linked to a steeper uplift of new work, although subdued consumer confidence and ongoing uncertainty served to limit gains.”

- “Moreover, service providers reported the steepest reduction in foreign demand in just over three years, whilst sentiment regarding the outlook softened, linked in some instances by firms to tariffs and political uncertainty. That said, capacity pressures continued to build and encouraged service providers to lift staffing levels marginally.”

- “On the price front, cost pressures remained historically elevated driven principally by tariffs and higher labor and supplier costs. In response, services companies raised their own selling prices, but at a slightly softer rate.”

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EGB OPTIONS: Bund outright Put seller

RXH6 126.50p, sold at 51.5 in 9.2k.

EURGBP TECHS: Bear Cycle Remains Intact

- RES 4: 0.8865 High Nov 14 and a bull trigger

- RES 3: 0.8840 High Nov 20

- RES 2: 0.8818 High Nov 26

- RES 1: 0.8747/97 50-day EMA / High Dec 17 and a key resistance

- PRICE: 0.8674 @ 14:51 GMT Jan 5

- SUP 1: 0.8670 Low Oct 21

- SUP 2: 0.8656 Low Oct 8 and a key support

- SUP 3: 0.8633 Low Sep 15

- SUP 4: 0.8620 38.2% retracement of the Dec ‘24 - Nov ‘25 bull cycle

The bear cycle that started Nov 14 in EURGBP remains intact. 0.8706, the 76.4% retracement of the Oct 8 - Nov 14 bull leg, has been cleared. The break of it strengthens the current bear theme and opens 0.8656, the Oct 8 low and a key support. On the upside, initial resistance is at 0.8744, the 50-day EMA. Key short-term resistance has been defined at 0.8797, the Dec 17 high.

SOFR OPTIONS: Post-Open Trade Remains Mixed

Projected rate cut pricing has consolidated vs. early morning levels (*): Jan'26 steady at -4bp (-4.6bp), Mar'26 at -13.7bp (-14.5bp), Apr'26 at -19.5bp (-20.6bp), Jun'26 at -33.7bp (-35.3bp).

- -1,500 0QG6 96.87 straddles, 21.25

- +8,000 SFRZ6 96.87 calls, 27.0 vs. 96.895/0.50%

- +2,000 SFRF6 96.31/96.43/96.50 1x3x2 call flys, 5.0 ref 96.485

- +10,000 SFRF6 96.43 puts, 2.0 (-2.5k sold earlier at 1.75)

- -8,000 0QG6 97.25/97.75/98.25 call flys, 1.5

- +4,000 SFRH6/SFRM6 96.00/96.25 put spd strip, 0.5

- +4,000 SFRM6 98.00 calls, 2.0 ref 96.69

- 24,059 SFRH6 96.31/96.37/96.50 put trees ref 96.485