FED: September Cut In The Balance (1/2)

Double-Dissent, Weaker Growth Leaned Dovish: The first sign of a possible dovish turn coming out of the July FOMC meeting was a double dissent in favor of a 25bp rate cut by Governors Bowman and Waller, which - while widely expected - confirmed that there is a growing contingent of activist rate cut supporters.

- And the Statement somewhat unexpectedly acknowledged slowing economic growth in contrast to the previous "solid" description. This appeared to be laying the groundwork for a potential "live" September meeting.

- "But", he added, "it is also possible that the inflationary effects could instead be more persistent, and that is a risk to be assessed and managed.”

- He spent much of the press conference emphasizing the FOMC’s focus on inflation running above-target. He said that he would characterize current policy as "modestly restrictive". and that “it seems to me and to almost the whole committee that the economy is not performing as [though] a restrictive policy is holding it back inappropriately, and modestly restrictive policy seems appropriate... the majority view was still what it has been, which is that inflation is running above target, maximum employment is right at target… When we have risks to both goals, one of them is farther away from goal than the other and that's inflation. Maximum employment at goal. That means policy should be tight because tight policy is what brings inflation down."

- Indeed he repeated multiple variations of the theme: "even if you look through the tariff effects, we think it's still a bit above target", while "the labor market looks solid".

- Asked about Gov Waller’s claim that the labor market is “on the edge”, Powell said “I think if you take the totality of the labor market data, you have got a solid labor market. But I think you have to see that there are downside risks.”

September Cut In The Balance: Overall, Powell said it's "really hard to say" whether there will be enough information to cut in September. Asked about the what the Fed is looking for in the data:

- "If you saw that the risks to the two goals were moving into balance, if they were fully in balance, that would imply that you should move toward a more neutral stance on policy. This is the special situation we are in, which is, we have two-sided risks... As the two targets get back into balance, you would think you would move it in a way closer to neutral and the next steps that we take are likely to be in that direction. What will it take? It will be the totality of the evidence. As I mentioned, there's quite a lot of data coming in which before the next meeting, will it be dispositive of that? You know, it's really hard to say. We don't make those decisions right now. So, we will have to see."

- "This is an intermeeting period where we will get two full rounds of employment and inflation data before the time of the September meeting. We have made no decisions about September. We don't do that in advance."

- While it’s a different situation this year, compare Powell's responses at this press conference with July 2024, when the FOMC held rates but ended up cutting 50bp in September. Both times he emphasized that the FOMC hadn't decided on future meetings, and that it would come down to the "totality" of the data, but last year he explicitly said "a reduction in our policy rate could be on the table as soon as the next meeting in September…the broad sense of the Committee is that the economy is moving closer to the point at which it will be appropriate to reduce our policy rate.”

- The divide on the Committee this time amid significant uncertainty appears to be too great to make any pre-commitment.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

USDCAD TECHS: Pivot Resistance Remains Intact

- RES 4: 1.4111 High Apr 4

- RES 3: 1.4016 High May 12 and 13 and a key resistance

- RES 2: 1.3920 High May 21

- RES 1: 1.3806 50-day EMA

- PRICE: 1.3654 @ 17:10 BST Jun 30

- SUP 1: 1.3618 Low Jun 26

- SUP 2: 1.3540 Low Jun 16 and the bear trigger

- SUP 3: 1.3503 1.618 proj of the Feb 3 - 14 - Mar 4 price swing

- SUP 4: 1.3473 Low Oct 2 2024

USDCAD is trading below its recent highs. The primary downtrend remains intact and short-term gains between Jun 16 - 23 appear to have been corrective. Key support and the bear trigger has been defined at 1.3540, the Jun 16 low. Clearance of this price point would resume the downtrend. Any reversal higher would instead signal scope for a stronger retracement. Pivot resistance to monitor is at the 50-day EMA, at 1.3806.

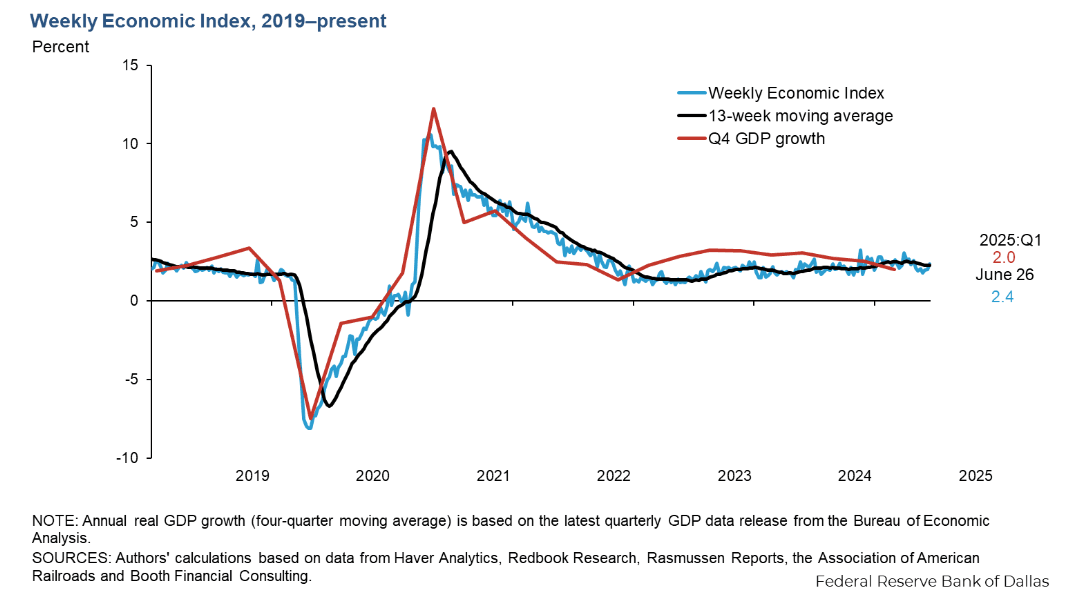

US DATA: Weekly Economic Index Points To Continued 2+% Growth

The Dallas Fed's weekly economic index came in at 2.37% in the week ending June 21 (scaled to four-quarter GDP growth), a pickup from 2.01% the prior week.

- That brought the 13-week moving average to 2.27%, which represents a slight uptick from 1.99% in Q1 2025 on the same basis.

- This is another high-frequency barometer that suggests that the trajectory of real GDP growth hasn't really shifted significantly in the last few months.

- Note this an approach that eyes Y/Y growth (if the entire quarter persists at 2.37%, activity for the quarter is expected to be recorded at 2.37% higher than the same quarter a year earlier), different from Q/Q SAAR growth, which measures and annualizes sequential quarterly growth (which the Atlanta Fed currently nowcasts for Q2 at 2.9%). Y/Y GDP in Q1 was 2.0%, vs -0.5% on a Q/Q SAAR basis.

US TSYS: Tsys Near Late Session Highs with Stocks, US$ at March '22 Lows

- Treasuries look to finish near late Monday highs, curves bull flattening amid mildly cautious risk-on tone after Canada withdrew last Friday's plans to implement a digital tax on US tech companies, trade talks to resume with US, Hassett said.

- Tsy Sep'25 10Y trades +10 at 112-04 after the bell, key resistance above at 112-23 (High May 1), 2s10s -2.210at 50.476, 5s30s -1.630 at 98.714.

- Amid the renewed focus on rate differentials in FX, the bull flattening move for the US curve has helped the US dollar extend its most recent weakness, with the dollar index falling around 0.5% to fresh cycle lows (March 2022 levels).

- The moves come amid President Trump stepping up his criticism of Fed Chair Powell and his ‘entire board’ over the level of US interest rates. Notably, Goldman Sachs have also pulled forward their call for the next Fed cut to September.

- Also note: Morgan Stanley strategists suggest buying SFRZ5 futures ahead of tomorrow's May Jolts and Thursday's June Non-Farm Payrolls release that may underpin rate cut projections that are over halfway between 50bp to 75bp in rate cuts by year end. "Downside risks to US labor market data remain underpriced, especially considering the potential for near 0k payroll prints starting as soon as July," MS suggested in a recent strategy piece.

- Stocks extended late Monday session highs - either caution to the wind ahead of a heavy data (shortened) week (markets are closed for the Independence Day holiday Friday, which draws the June employment release one day forward). Or month-end tied buying as money managers reallocated funds.