US STOCKS: S&P Stalling Above 6000

The ESM5 Overnight range was 6006.25 - 6074.75, Asia is currently trading around 6015. Interesting price action in stocks, positive trade talks with China, a lower CPI which has the market pricing in potential rate cuts and Bessent stating that the US could extend the tariff pause for countries dealing in “good faith” on trade. Is the good news already baked into the price as the S&P trades heavy above 6000.

- The Kobeissi Letter on X: Retail investors' purchases of Big Tech are slowing: The 10-day moving average of retail purchases of the Magnificent 7+ stocks as a % of total retail inflows just fell to ~12%, the lowest since the start of the 2022 bear market. This share has declined by ~24 percentage points over the last 2 months. To put this into perspective, an all-time high of 42% was recorded in January 2023. However, retail investors are still heavily invested in technology stocks overall. Retail is simply cashing in some profits. https://x.com/KobeissiLetter/status/1932557384553046281

- (Bloomberg) - “The S&P 500 is within striking distance of new all-time highs following May’s CPI report, but the current rally has a number of headwinds, leaving market participants wondering how much further upside equities have.”

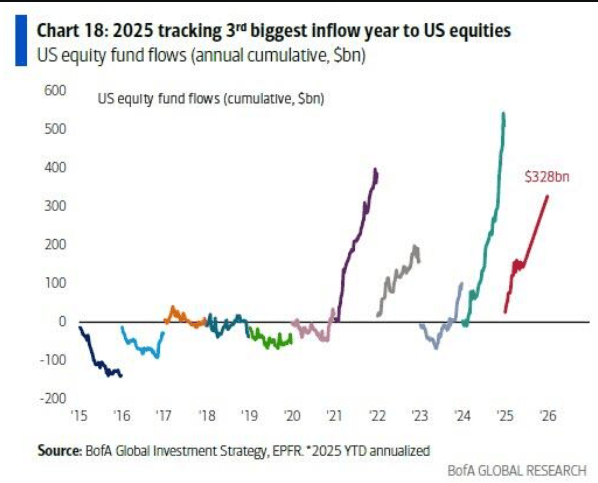

- Barchart on X: U.S. Equities on track for a yearly inflow of $328 billion, the 3rd largest in history. See chart below.

- Overnight decent demand was seen over the CPI print but this move higher was met with supply and was quickly reversed, closing back towards the 6000 area.

- Momentum type funds and share buybacks have kept the market well supported as an underweight market has been forced to reenter. Share buybacks are set to enter their blackout period starting next week, will this be the signal for a potential pullback ?

In the short-term stocks look overbought, if the S&P can’t hold above 6000 we could see the start of some sort of a retracement. The first buy-zone is back towards the 5700 area where demand could be expected.

Fig 1: US Equity Inflows

Source @Barchart via X/BofA

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE BONDS: Sharply Cheaper With US Tsys, Con & Bus Conf Due

ACGBs (YM -10.0 & XM -6.0) are sharply weaker after US tsys finished sharply cheaper. US tsys gapped lower in early London trade and stocks surged to the pre-Liberation Day levels (April 2) after the US and China agreed to pause their retaliatory reciprocal tariffs for 90 days.

- After a collective sigh of relief, US tsys traded sideways, near session lows for much of the session. The pop in risk appetite and the less dovish Fed outlook saw the 2-year bond cheapen 12bps to 4.01%, with the 10-year yield 9bps at 4.48%. Today’s focus is on April US CPI figures at 0830ET.

- Cash ACGBs are 6-9bps cheaper with the 3/10 curve flatter and the AU-US 10-year yield differential at -4bps.

- The bills strip has bear-steepened, with pricing -3 to -10.

- RBA-dated OIS pricing is 2-10bps firmer across meetings today. A 25bp rate cut in May is given a 96% probability, with a cumulative 82bps of easing priced by year-end (based on an effective cash rate of 4.09%).

- Today, the local calendar will see Westpac Consumer and NAB Business Confidence measures.

- AOFM plans to sell A$1200mn of the 3.50% 21 December 2034 bond on Wednesday and A$800mn of the 2.50% 21 May 2030 bond on Friday.

US TSYS: Cash Open

TYM5 is trading 110-04+, unchanged from its from its close.

- The US 2-year yield opens around 4.00%, down 0.01 from its close.

- The US 10-year yield opens around 4.463%, down 0.01 from its close

- Bloomberg - “ Investors are avoiding Treasury bills that mature in August due to Treasury Secretary Scott Bessent's warning that the US may run out of cash if the federal debt ceiling isn't raised or suspended by then.”

- “The Treasury's $76 billion auction of three-month bills that will mature in August received tepid investor demand, with a high rate of 4.30% and a small award to indirect bidders.”

- After a significant hawkish re-pricing on positive trade developments, Fed Funds futures imply a next Fed cut coming in July (two meetings away) is only a 50/50 call with it fully priced for September. - MNI US

- The 10-year Yield range seems to be 4.10% - 4.5%, price has bounced nicely off the 4.25/30 support, price is now testing the upper bound of the range around 4.45/50%. A sustained break above this level would see another round of selling targeting the 4.75% area.

- Data: US CPI

JPY: Little Change in USD/JPY Post BoJ Summary Of Opinions

USD/JPY was little changed post the release of the BoJ Summary Of Opinions (SOO) from the early May policy meeting. We were last near 148.20, down slightly from end NY levels on Monday.

- The SOO had a strong emphasis on high uncertainties facing the outlook, particularly in terms of US trade policy. Still there is scope to raise rates if the outlook is realized, but the discussion recognised upside and downside risks to the outlook. Also less certainty of achieving the outlook compared to earlier in the year, which saw the downward forecast revisions at the May 1 meeting outcome. All in all the central bank is wait and see mode for the near term.