US STOCKS: S&P- Semiconductors/AI Back Under Pressure, Kimi K3 Adds To Headwinds

The S&P(ESU6) range overnight was 7548.25 - 7625.00, SPX closed -0.51%, Asia is currently trading ar...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US STOCKS: S&P - Pulls Back As Tech Sees Some Profit-Taking

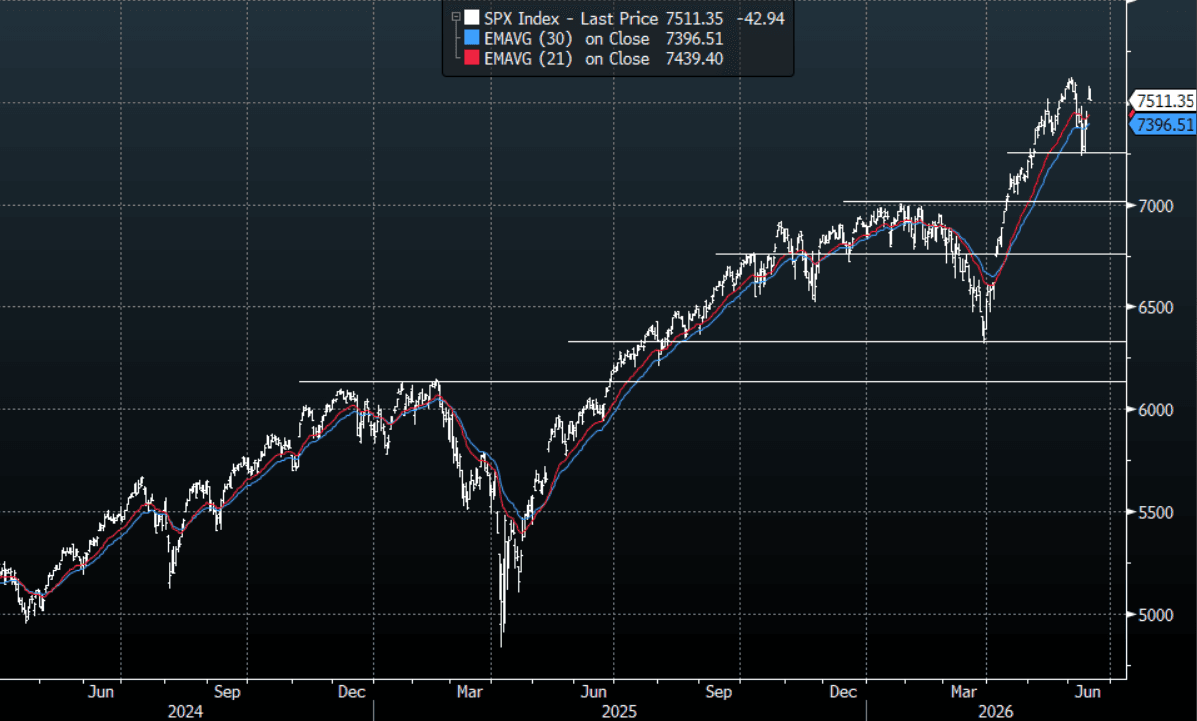

The S&P(ESM6) range overnight was 7578.00 - 7636.75, SPX closed -0.57%, Asia is trading around 7595, +0.10%. The index could not continue its surge higher and stalled for the first time as some selling in Tech was seen, SpaceX continues its march higher though as money pours in. With peace now being priced in the Middle-East and an unprecedented surge by anyone and everyone to get long SpaceX it's hard to make a bearish case other than, it doesn't make sense. The price action is very bullish and while we continue to hold above 7250-7300 I suspect dips will continue to be faded. This morning US futures opened slightly higher, E-minis(S&P) +0.10%, NQZ5 +0.20%. Support is now back toward the 7500-7540 area, as the all-time highs come back into play.

- The Kobeissi Letter on X: “Retail investors are piling in to SpaceX stock: Over the last 2 trading sessions, retail investors bought nearly as much SpaceX, $SPCX, as every other US single stock combined in the entire prior week, according to Vanda Research data.”

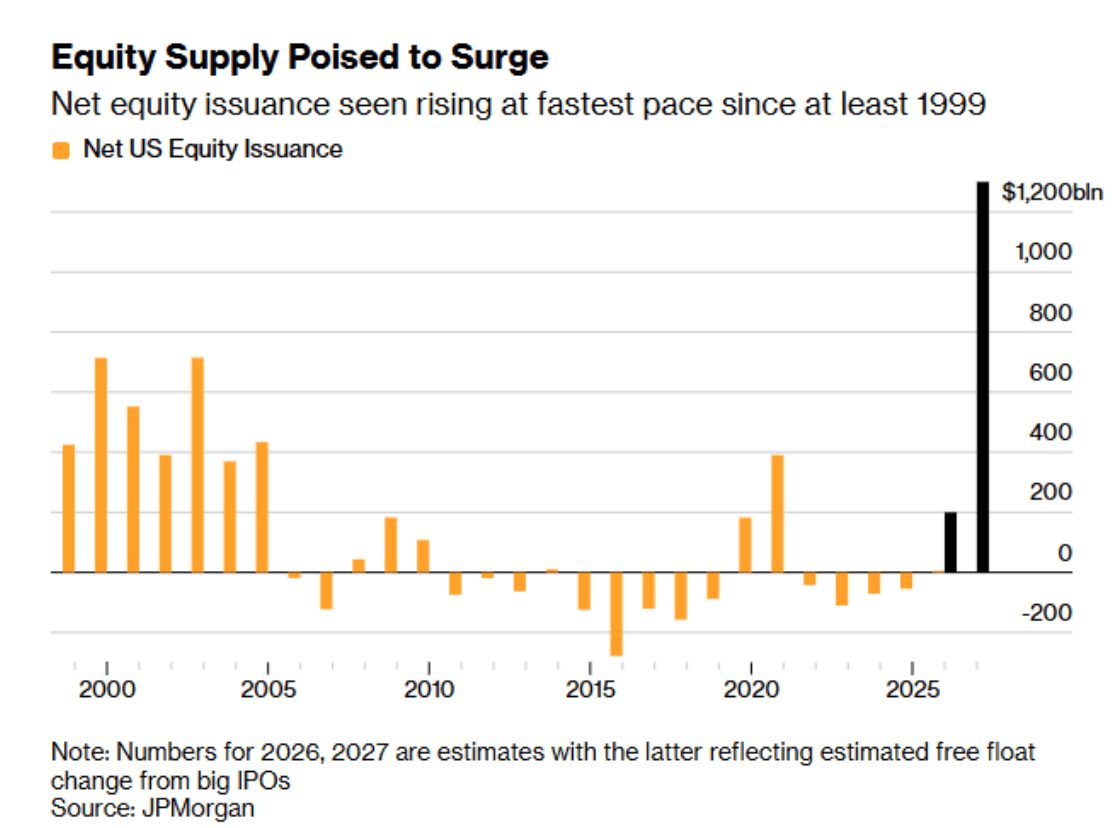

- Tracy Shuchart on X: “SpaceX and OpenAI Are Ending Wall Street’s Era of Stock Scarcity. For the better part of two decades, a defining feature of the US stock market has been scarcity. Year after year, shares disappeared from public hands, with buybacks by S&P 500 companies alone erasing nearly $12 trillion worth. Now, investors are about to discover what happens when the supply suddenly comes rushing back." See Fig. 1 below.

- Danny Citrinowicz on X: “Iran sees a direct link between what happens in Lebanon and regional stability as a whole, and even reserves for itself an opening to renew the confrontation if it believes the campaign against Hezbollah continues.”

- “The question is not only what they think in Beirut or Tehran, but also how much patience(for Israel) remains in the White House for a situation in which the Lebanese arena threatens to thwart a broader strategic goal from Trump's perspective – a deal with Iran and avoiding further deterioration in the Middle East.”

- The S&P 500 Index Average True Range(ATR) for the last 10 Trading days: 125 Points

Fig 1: Equity Supply

Source: MNI - Market News/@chigrl/JPMorgan

Fig 2: S&P 500 Index Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

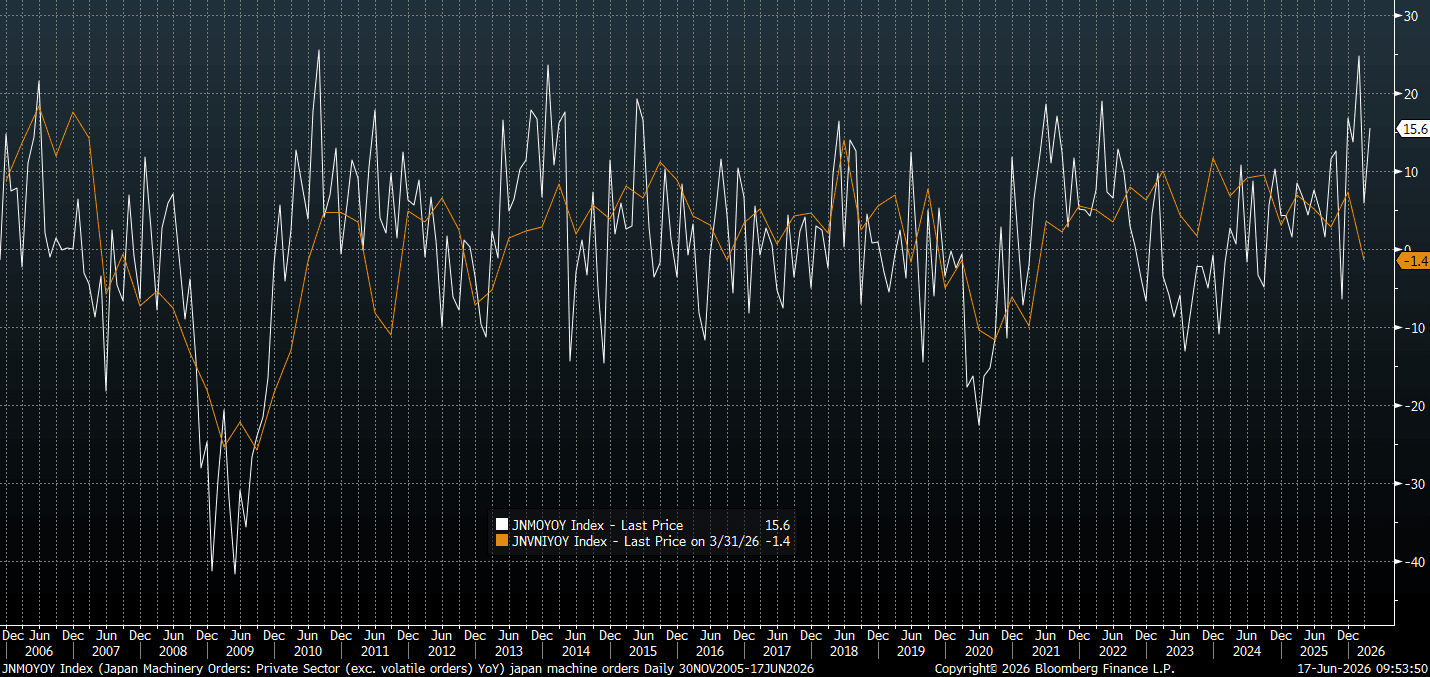

JAPAN DATA: Machine Order Beat Points To Improved Q2 Capex

Japan core machine orders for Apr were better than forecast. In m/m terms we rose 8.7%, against a 0.5% forecast and -9.4% Mar outcome. In y/y terms we rose 15.6%, against a 8.7% forecast and prior outcome of 5.9%. At face value this is a positive start for Capex trends in the first part of Q2. The chart below plots the core machine orders y/y, versus Capex y/y (ex software). If the better machine order trend holds for Q2 it does point to a capex rebound. This would be consistent with a still supportive external backdrop, as other data showed exports up 17%y/y for May, while the manufacturing PMI has also stayed elevated through Q2 to date.

- Rtrs also noted earlier that its Tankan survey measure rose to +13 in June versus +8 in May. Chip related orders reportedly surged.

- In terms of the detail on the machine orders print today, manufacturing rose 5.1%m/m, to be 12.9% higher y/y. Non-manufacturing also posted solid m/m and y/y gains.

Fig 1: Japan Core Machine Orders Y/Y (White Line) & Capex, Ex Software Y/Y (Orange Line).

Source: Bloomberg Finance L.P/MNI

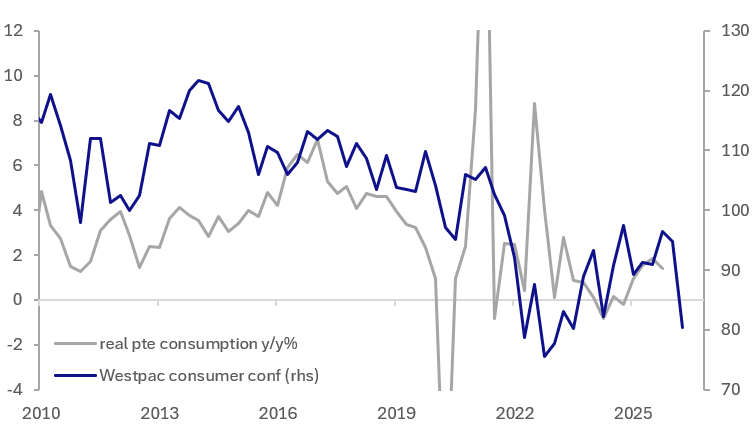

NEW ZEALAND: Weak Sentiment Measured Before Middle East Stabilisation

Westpac consumer confidence fell sharply in Q2 to 80.4 from Q1’s 94.7, the lowest since Q3 2023. Geopolitical uncertainty weighed on sentiment but cost-of-living pressures are a major concern, exacerbated by higher fuel prices. Also wholesale rates have increased mortgage costs before the RBNZ actually tightens. Sentiment suggests a slowing of private consumption growth in Q2 but card transactions are holding up.

- If the reopening of the Strait of Hormuz, expected on Friday, is sustained and a long-term US-Iran deal can be reached, then households may see some relief - retail fuel prices are already lower. Other input costs would also likely fall, such as fertiliser. Therefore, the RBNZ may not have to hike rates as much as feared. It will take time though for the benefits to be felt from free shipping.

- There was a decline in all components with present conditions down to 73.5 from 87.9 and expectations 85.0 from 99.2. The economic outlook and current & future finances all deteriorated.

- Westpac notes that its consumer survey was taken in the first two weeks of June before the announcement of the memorandum of understanding between the US and Iran. It’s possible that respondents felt that a deal to reopen Hormuz was unlikely especially as the US-Iran-Israel had resumed hostilities.

Westpac consumer sentiment vs private consumption growth

Source: MNI - Market News/LSEG