AUSSIE BONDS: Richer But Subdued Data-Light Session

ACGBs (YM +3.0 & XM +6.5) are stronger and at Sydney session bests on a data-light day.

- (ABC via BBG) Former RBA assistant governor Luci Ellis, who is now Westpac's chief economist, described the decision — by a six-to-three majority of the monetary policy board — to wait before cutting rates again as "uncharitable".

- Cash US tsys are flat in today’s Asia-Pac session yesterday's modest rally. Today’s US calendar: Initial Jobless Claims and US To Sell $22 Bln 30-year Bond.

- Cash ACGBs are 4-6bps richer with the AU-US 10-year yield differential at -5bps.

- The bills strip has bear-flattened, with pricing flat to +4.

- RBA-dated OIS pricing is slightly softer across meetings today. A 25bp rate cut in August is given a 90% probability, with a cumulative 62bps of easing priced by year-end.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGBS: Futures Nudge Into Negative Territory At Lunch, BoJ Ueda Remarks

At the Tokyo lunch break, JGB futures are slightly weaker, -4 compared to the settlement levels, after giving up overnight gains.

- BoJ Governor Ueda has been before parliament, answering questions from lawmakers. The Governor inoted limited policy space on the downside, given the current 0.50% policy rate. This is if fresh stimulus is needed. The real rate is being kept sub 0% to stimulate the economy further, as Ueda states that Japan is still some distance from the 2% inflation objective. Ueda reiterated that they will raise rates if they have confidence in achieving the 2% target.

- US equity futures have broken to fresh multi-month highs in the first part of Tuesday trade, with Nasdaq futures slightly outperforming. We can't see any direct fresh catalysts for the move.

- Cash US tsys are 1-2bps cheaper, with a slight flattening bias, in today's Asia-Pac session after yesterday's modest rally.

- Cash JGBs have twist-flattened across benchmarks, with 5-7-year yields 1bp higher and the 30-40-year yields 2bps lower. The benchmark 10-year yield is 0.3bp higher at 1.471% versus the cycle high of 1.596%.

- Swap rates are flat to 2bps higher, with the curve steeper. Swap spreads are mixed.

ASIA STOCKS: Large Inflow for Korea to Start the Week

A relatively quiet start to the week with a major inflow for Korea tipping the last 5-days of inflows above $2bn

- South Korea: Recorded inflows of +$834m yesterday, bringing the 5-day total to +$2,117m. 2025 to date flows are -$8,739. The 5-day average is +$423m, the 20-day average is +$158m and the 100-day average of -$89m.

- Taiwan: Had inflows of +$4m as yesterday, with total inflows of +$167 m over the past 5 days. YTD flows are negative at -$12,611. The 5-day average is +$33m, the 20-day average of +$93m and the 100-day average of -$116m.

- India: Had inflows of +$147m as of the 6th, with total outflows of -$292m over the past 5 days. YTD flows are negative -$10,820m. The 5-day average is -$58m, the 20-day average of -$11m and the 100-day average of -$106m.

- Indonesia: Had outflows of -$44m as of the 5th, with total outflows of -$205m over the prior five days. YTD flows are negative -$3,014m. The 5-day average is -$41m, the 20-day average +$2m and the 100-day average -$30m.

- Thailand: Recorded outflows of -$6m as of yesterday, outflows totaling -$417m over the past 5 days. YTD flows are negative at -$2,172m. The 5-day average is -$41m, the 20-day average of +$2m and the 100-day average of -$30m.

- Malaysia: Recorded outflows of -$8m as of yesterday, totaling -$100m over the past 5 days. YTD flows are negative at -$3,523m. The 5-day average is -$18m, the 20-day average of -$2m and the 100-day average of -$25m.

- Philippines: Saw outflows of -$4m yesterday, with net inflows of +$6m over the past 5 days. YTD flows are negative at -$517m. The 5-day average is +$1m, the 20-day average of -$14m the 100-day average of -$5m.

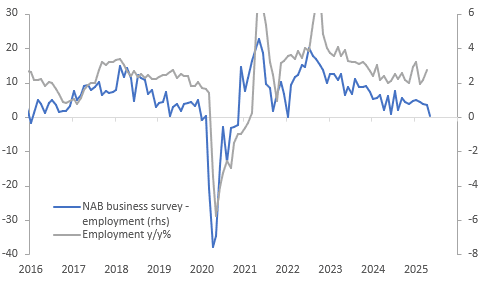

AUSTRALIA DATA: Employment Weakens But Forward Orders Improve

NAB business confidence continued to oscillate around zero in May as it has done for around two and half years. It printed at +1.9 after -0.9 in April, the highest since January. However, conditions carried on their downtrend reaching 0.3 in May following 1.6, the lowest since the Covid-impacted August 2020. Q2 average confidence is suggesting a stabilisation in annual growth in the quarter but conditions suggest it will slow.

Australia NAB business survey vs GDP y/y%

- Business conditions were driven down by employment and trading. Profitability was stable. In terms of the outlook, forward orders improved to -1.8 from -3.0, the best since October 2023. Given heightened global uncertainty, there was good news on the export front with both current and sales rising in May to their highest since December.

- Labour demand fell to 0.4 in May from 3.6, the lowest since January 2022. The trending down over this year is suggesting that employment growth is likely to slow. May data prints on June 19.

Australia employment

Source: MNI - Market News/LSEG/ABS