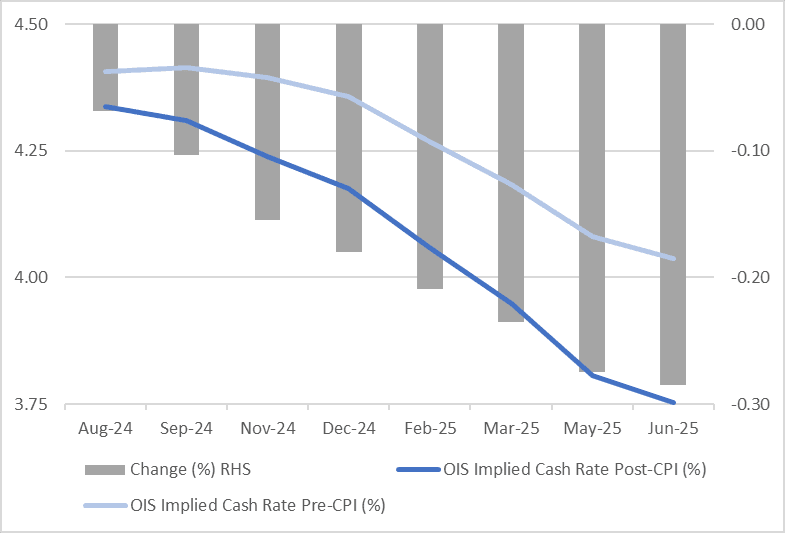

STIR: RBA Dated OIS - Year-End Easing Expectations Return

RBA-dated OIS pricing has softened 7-28bps from pre-CPI levels across meetings, with 2025 meetings leading.

- Terminal rate expectations have tumbled to 4.34% (versus the current effective rate of 4.32%) from 4.42% before yesterday’s CPI data.

- Easing expectations have returned with the expected year-end official rate falling to 4.19%, its lowest level since the mid-June RBA meeting.

Figure 1: RBA-Dated OIS – Pre- Vs. Post-CPI

Source: MNI – Market News / Bloomberg

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CHINA PRESS: Low Land Sale Revenue Could Need More Debt Issuance

Authorities issuing additional local government special refinancing bonds for resolving hidden debts in H2 cannot be ruled out, given the 14% y/y decline in land revenue from January to May, according to Wang Qing, chief macro analyst at Golden Credit Rating. Wang noted that broad fiscal expenditure, which combines general public and government fund budget expenditure, fell by 2.2% year-on-year during January to May, which was not conducive to the counter-cyclical role of current fiscal policy. (Source: 21st Century Business Herald)

CHINA PRESS: PBOC May Sell Treasuries To Curb Falling Bond Yields

The People’s Bank of China may start selling treasury bonds after deciding to borrow from selected primary dealers, in a bid to increase bond supply and curb falling yields of medium- and long-term bonds, Shanghai Securities News reported citing analysts. The central bank has repeatedly warned of maturity mismatch and interest rate risk from holding large amounts of longer-term bonds, the newspaper said. The PBOC’s holdings of government bonds are mostly three years or less, and treasury borrowing operations may pave the way for bond sales, said Zhou Guannan, chief fixed income analyst of Huachuang Securities.

BONDS: NZGBS: Short-End Moves Away From Session Cheaps After Business Opinion Survey

After initially being pressured by US tsys’ overnight bear-steepening, NZGBs have moved away from the session’s worst levels, led by the short end. Currently, NZGB benchmark yields are flat to 5bps higher compared to 7bps higher earlier in the session.

- The swaps curve has shifted from a bear-steepening to a twist-steepening, with rates 1bp lower to 4bps higher.

- RBNZ dated OIS pricing is flat to 3bps softer, with 2025 meetings leading. A cumulative 33bps of easing is priced by year-end.

- Earlier, the NZIER Business Opinion Survey for Q2 showed a net 44% of businesses expect the economy to get worse, from 25% with that view in Q1. A net 28% of businesses reported a decline in their own trading activity in Q2, with a net 10% of businesses expecting their own activity to worsen in Q3. A net 23% of firms raised prices in Q2, vs 35% in Q1.