NEW ZEALAND: Q1 Growth Materially Stronger Than RBNZ Forecast

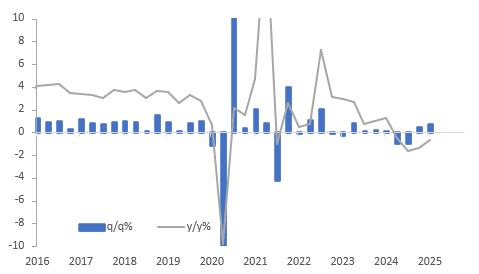

Q1 NZ production-based GDP was stronger than expected rising 0.8% q/q resulting in the annual rate falling 0.7% y/y but up from the downwardly-revised -1.3% in Q4. Expenditure GDP rose 0.9% q/q, the fastest since Q2 2023, to be down 0.2% y/y after -1.1% in Q4. Growth in Q1 was fairly broad based and substantially above the RBNZ’s May forecast. While it is backward-looking data, it may allow the central bank to pause in July especially given the pickup in inflation.

NZ production-based GDP %

Source: MNI - Market News/LSEG

- Nine of sixteen industries posted an increase in growth with primary, goods and services sectors all positive.

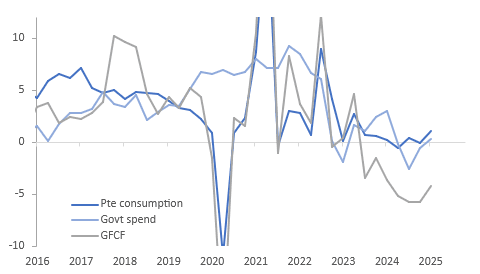

- Domestic demand was robust rising 1.1% q/q to be down 0.3% y/y after -1.5% y/y in Q4. This was the second straight quarter of growth.

- Private consumption rose 1.3% q/q driven by spending on services, durables and non-durables. It was the strongest quarter since Q1 2022 which was impacted by the post-Covid recovery. This strength is in contrast to card transaction and consumer sentiment data, which have been flat and pessimistic respectively.

- Government spending rose 1.1% q/q to be 0.3% y/y higher up from -0.6% y/y.

- GFCF rose 0.6% q/q, the first positive after 7 consecutive declines. The pickup was driven by a 2% q/q rise in residential building, a sign that the construction sector is recovering. Other GFCF fell 0.1% q/q.

- Net exports detracted 0.1pp from growth due to slightly higher goods & services imports but a sharp 8.5% q/q drop in services exports offsetting the 3.6% q/q rise in goods shipments.

- Productivity rose 0.8% q/q and rose 0.4% y/y, the second consecutive quarterly increase, which the RBNZ will want to see continue as low productivity growth has been a concern.

- GDP per capita increased 0.5% q/q in Q1.

NZ domestic demand y/y%

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGBS: Futures Richer With US Tsys, Light Local Calendar, 20Y Supply

In post-Tokyo trade, JGB futures closed stronger, +16 compared to settlement levels, after US tsys finished the NY session 2-4bps richer.

- Jitters over Moody's downgrade on Friday rekindled fears of another "Sell America" trade. But the downgrade concerns abated since it was a long time coming and not surprising.

- 30Y yields notably touched their highest since Nov 1 2023 (5.0353%) - up 13.5bp from Friday's ratings downgrade announcement - before an impressive reversal lower on the day (just 1+bp up from pre-downgrade).

- We heard from multiple Fed speakers, including Bostic, Jefferson, Williams, and Kashkari. All of them reiterated the FOMC's patient approach to cuts amid economic uncertainty, and Williams and Bostic in particular suggested that the next cut wouldn't seriously be contemplated until after the summer. Reaction was limited, however, given the market's already-low implied probability of a cut before September.

- US President Trump has had a two-hour conversation with Russian President Putin about the war in Ukraine. Trump said that he believes that Putin wants peace.

- Reuters reported - "Nippon Steel plans to invest $14 billion in US Steel if the Trump administration approves the merger of the companies."

- Today, the local calendar will see Tokyo Condominiums for Sale data alongside 20-year supply.

BONDS: Richer After US Tsys Reverse Initial Downgrade Reaction

In local morning trade, NZGBs are 2-4bps richer after US tsy yields finished the NY session 2-4bps lower.

- Wall Street and US tsys erased early losses and closed in the green. Jitters over Moody's downgrade on Friday rekindled fears of another "Sell America" trade. But the downgrade concerns abated since it was a long time coming and not really surprising.

- Overnight US 10-year yields had a range of 4.4434% - 4.5624%, closing around 4.44%.

- 30Y yields notably touched their highest since Nov 1 2023 (5.0353%) - up 13.5bp from Friday's ratings downgrade announcement - before an impressive reversal lower on the day (just 1+bp up from pre-downgrade).

- We heard from multiple Fed speakers. Reaction was limited, however, given the market's already-low implied probability of a cut before September.

- Swap rates are 2-4bps lower, with the 2s10s curve flatter.

- RBNZ dated OIS pricing is little changed across meetings. 25bps of easing is priced for May, with a cumulative 63bps by November 2025.

- Today, the local calendar will be empty ahead of trade balance data on Wednesday and the Budget on Thursday.

- On Friday, the NZ Treasury plans to sell NZ$250mn of the 3.00% Apr-29 bond, NZ$150mn of the 3.50% Apr-33 bond and NZ$50mn of the 1.75% May-41 bond.

CHINA: Preview: Loan Prime Rate Decision Today

- Loan Prime Rates ("LPR") are market-based benchmark lending rates used for new and outstanding loans, replacing the central bank's benchmark one-year lending rate. They are calculated monthly based on quotes submitted by designated commercial banks, with the National Interbank Funding Center (NIFC) acting as the publisher. The LPR is used as a reference for bank lending, and it's calculated by adding a spread to the Medium-Term Lending Facility (MLF) rate, which is a central bank lending instrument.

- The LPR's intent is to promote a market based system and to make credit pricing more efficient. It consists of two tenors: one-year and over-five-year. The one-year LPR is a key benchmark for most new and outstanding loans, while the five-year LPR is used for mortgages.

- Over the last year then PBOC has tended to focus on the daily open market operation ("OMO") as the mechanism for supporting interbank liquidity.

- On May 7th, the PBOC announced a reduction in the 7-day rate for reverse repo sold during the OMO.

- As such, we expect Banks to reduce their quotes for both tenors of the LPR by the 10bps reduction.

- This would bring the LPR's down to 3.00% for the 1-year and 3.50% for the 5-year