US: Probability Of GOP Retaining Senate Increases

The Republican Party has continued a steady recovery in their chances of retaining the Senate in Nov...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OPTIONS: Expiries for May28 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1520-30(E679mln) $1.1725-40(E5.2bln)

- USD/JPY: Y157.00($1.7bln), Y161.00($770mln), Y162.00($1.3bln)

- AUD/USD: $0.7115(A$545mln), $0.7175-85(A$782mln)

- NZD/USD: $0.5900(N$559mln)

- USD/CAD: C$1.3545-50($775mln)

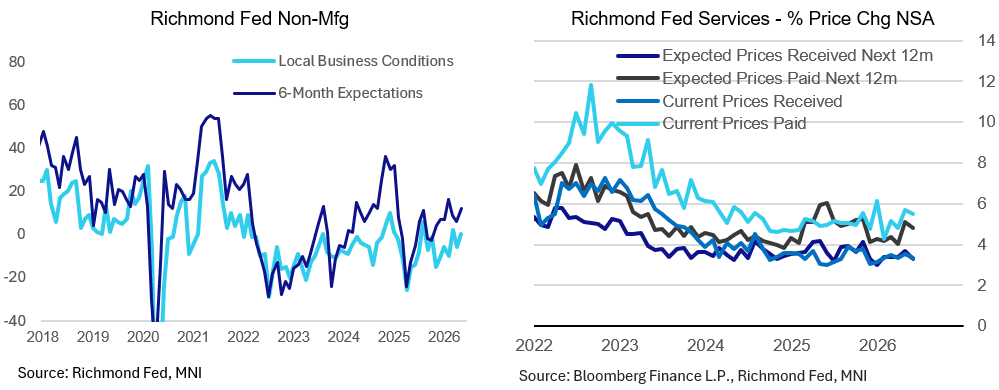

US DATA: Solid Richmond Fed Non-Mfg Sees Better Activity, Softer Inflation (2/2)

While just a 2-month high in the Richmond Fed non-manufacturing survey's main index (0 from -6), this is still a solid reading (compared with routinely negative readings over the past year), and details of the report were solid.

- First and foremost, 6-month expectations rose to 12 from 6, a 3-month high and the 2nd highest reading since the start of 2025. The revenues index rose to 14 from 9 with demand up to 15 from 10. On a slightly sourer note, employment fell to -1 in May from 6 prior.

- Like the Richmond manufacturing survey, there was a moderation in price pressures that appears to have helped spur an uptick in optimism. On a 12-month lookback basis, prices paid fell to 5.5% from April's 4-month high 5.7%, with received ticking down to 3.4% from 3.5%.

- And as with manufacturers, non-manufacturer inflation expectations appear to be stabilizing, with expected prices paid down to 4.8% from April's 6-month high 5.1% and receiived down to a 5-month low 3.3% (3.7% prior).

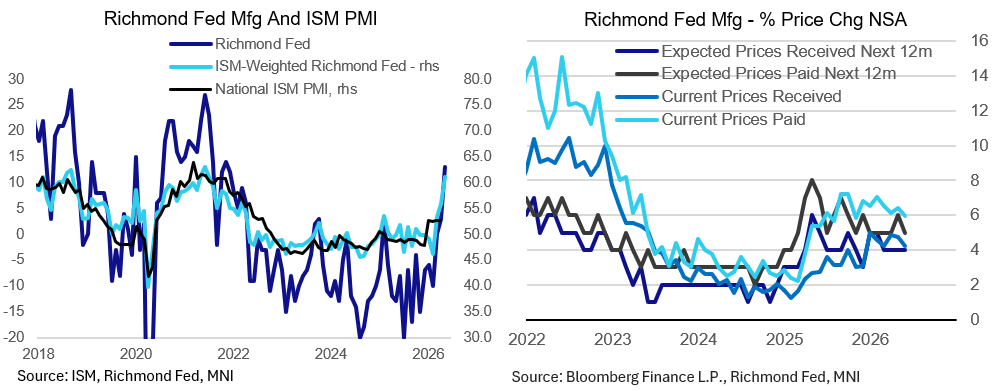

US DATA: Richmond Fed Survey Sees Strongest Manufacturing In Years In May (1/2)

The Richmond Fed's Fifth District industry surveys were better than expected in May, with manufacturing enjoying its strongest readings in years in the region (Washington D.C., Maryland, North Carolina, South Carolina, Virginia, and most of West Virginia). There is no anecdotal commentary included with these reports but the softening in inflationary gauges suggests some improvement in private sector optimism following the initial Middle East war-induced energy price spike.

- The manufacturing survey composite index jumped to 13 (3 prior, 4 expected), with the non-manufacturing local business conditions index rising to 0 (-6 prior, -5 expected).

- While just a 2-month high for non-manufacturing, that's a 54-month best for the manufacturing gauge - with all three of its component indexes notably higher (shipments to 16 from -2, new orders to 17 from 8, and employment to 3 from 0) for some of the best readings in years. And manufacturing expectations also jumped.

- On an ISM-weighted basis, the manufacturing index jumped to a 58-month high 61.0 from 55.8 (in addition to new orders, shipments, and employment above, delivery times were steady, inventories a little lower)

- And this came with a pullback in inflation gauges. The Richmond Fed reports 12-month back-looking indices, with prices paid dipping to a 7-month low 6.0% (6.4% prior) and prices received down to a 6-month low 4.2% (4.7% prior). Those are well down from 2026 peaks of 7.1% and 4.9%, respectively.

- In a sign of relatively anchored expectations, expected prices paid and received (12-months ahead) were relatively steady at 5.0% and 4.0%.