GERMAN DATA: Plummeting Euro Core Factory Orders Cast Doubt On Recovery

German factory orders rose 0.2% M/M in February on a price/seasonally/calendar adjusted basis, softer than the 0.7% expected and an even bigger downside miss vs consensus when considering a downward revision to January (by 0.1pp to -11.4%). This leaves factory orders more than 10% lower on a Y/Y working day adjusted basis, and while the headline number shows some stabilisation in the beleaguered industrial sector, the underlying trend in early 2024 remains to the downside.

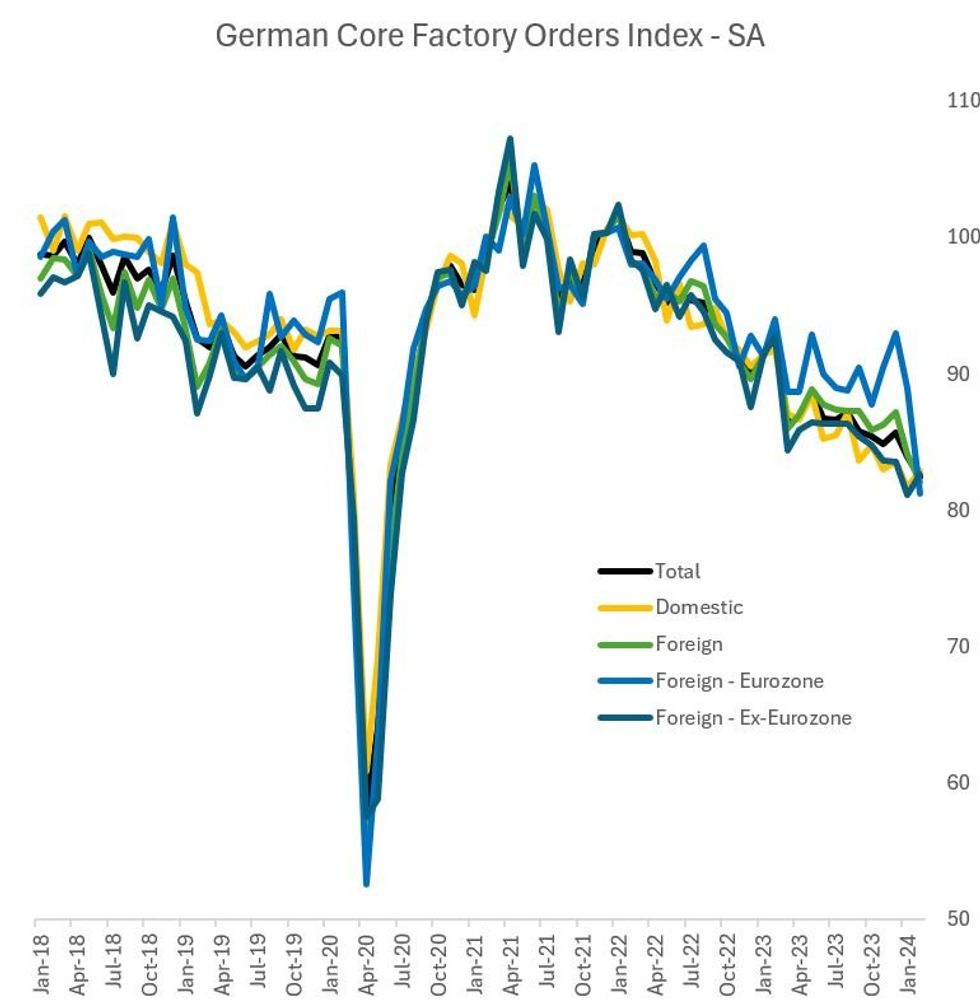

- Core (ex-large ticket items) orders, a better measure of underlying activity, fell by 0.8% M/M after -3.0% in January - the 5th contraction in 6 months. The breakdown showed domestic core orders actually fairly robust at +1.5%, the biggest gain in 6 months (-2.3% prior). Instead it was foreign orders that dragged down the overall index, falling by 2.4% M/M after -3.6% in January. Eurozone orders led the drop, plummeting by 8.8% M/M, after -4.3% in January (foreign ex-Eurozone orders actually rose for the first time in 9 months).

- Outside of the early pandemic months of 2020, this was the biggest single-month fall in core Eurozone factory orders since at least 2010. Overall (non-core) new orders from the Eurozone fell 13.1% (after -24.3% in Jan), with total ex-euro up 7.8% and domestic up 1.5%.

- It's unclear what spurred this drop, particularly as eurozone-wide surveys suggest a nascent rebound in demand and industrial production in 1Q 2024. While the drop in overall orders is clearly linked to a pullback in capital goods orders after a surge in December on a one-off contract, the core decline will be concerning if not reversed in the months ahead.

- Manufacturing turnover rose 2.2% M/M, vs -5.2% in January - the latter of which reflects major revisions from -2.0% prior (autos and machinery/equipment saw large revisions). While there is no consensus for this figure, it could underpin expectations for continued growth in industrial production in Monday's release (currently +0.5% M/M expected vs +1.0% in Jan).

- Overall though there is no convincing sign of a turnaround in German factory activity, with the manufacturing PMI falling to a 5-month low in February and the March EC manufacturing confidence survey plumbing the lowest levels since the pandemic.

Source: Destatis, MNI

Source: Destatis, MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EQUITIES: Estoxx spread is starting to be active

- Next week on the 15th March will see Triple Witching in Equities, and although it is still early for rolling into the June expiry (expected to pick up next week), Estoxx (VGA) has started to trade, and is slowly running above pace.

- The VGH4/VGM4 has mostly seen selling interest and has printed its lowest level at 45.00 Yesterday.

- This Morning has seen buying interest off that level so far today, bought for 45.50 and 45.75, and the Technical level might be one of the reason for some of the interest in the spread.

- VGH4/VGM4 trades on legs at 46 in 10k.

SOUTH KOREA: /RATINGS: Fitch Affirms Korea At AA-; Outlook Stable

Fitch notes that "Korea's rating balances robust external finances, resilient macroeconomic performance and a dynamic export sector against geopolitical risks related to North Korea, lagging governance indicators relative to 'AA' category peers and structural challenges from an ageing population."

- "Credit and policy buffers remain sufficient to manage near-term risks, but Korea has seen a relative weakening of its fiscal metrics compared with peers over the past five years."

- Click for more.

JPY: Demand for JPY Hedges Picks Up Alongside BoJ Tightening Talk

- After a quiet first two sessions of the week, FX options markets are busier early Wednesday, with BoJ-centric stories from MNI and Jiji helping stimulate activity. Total USD/JPY options notional traded is ~20% ahead of average for this time of day, and conversely to spot moves today, upside protection is in demand - evident in decent interest across 140.65, 144.50 and 146.25 ITM call strikes, tipping the put/call ratio to 0.71 for DTCC-tracked trades today.

- Two-week vols, now capturing the outcome of the March 19th BoJ decision, are further bid, adding to yesterday's rally to touch 9.3 points and the highest level since early February. This tips 2w vols above the YTD average, but still just shy of the 12m rolling 2w vol.

- The bid in the front-end of the JPY vol curve has added to the recent vol skew, as 3m vols fail to keep pace and remain subdued: 3m implied holds at 8 points, close to 2 points below the rolling 12m average, despite capturing both the March and April BoJ decisions. OIS markets now price a ~50% chance of a 10bp March hike (vs. 30% yesterday), with a BoJ exit from NIRP now fully priced through the end of the June meeting (vs. 90% prior).