CHINA: PBoC - To Add Overnight Reverse Repo At Appropriate Time

Headlines crossing from PBoC Governor Pan at Lujiazui forum. "*PAN: 7-DAY REVERSE REPO RATE HAS HAD ...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

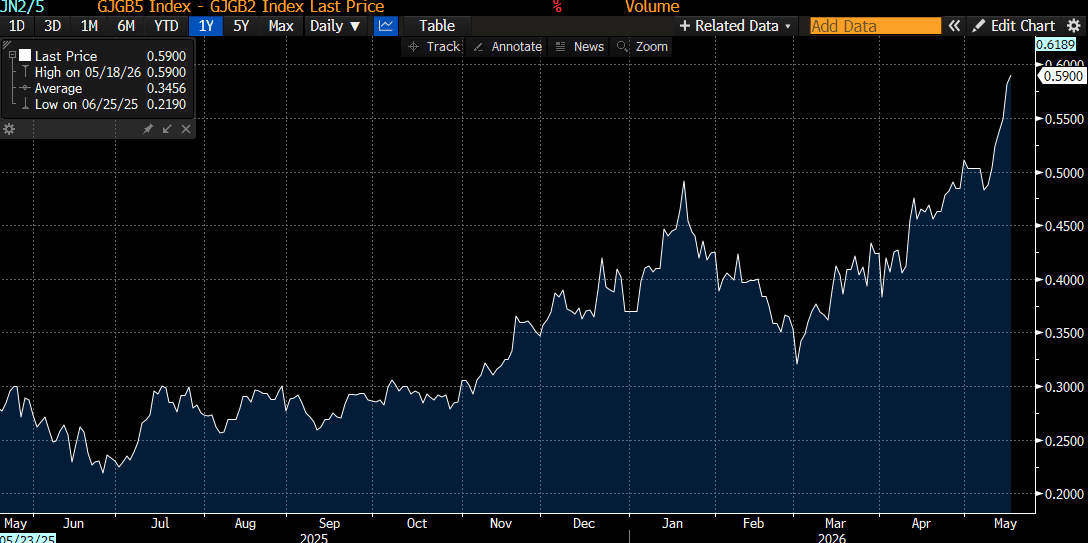

JGBS AUCTION: 5Y Supply Faces Higher Yield & Steeper Curve

The Japanese Ministry of Finance (MoF) will today sell Y2.5tn of 5-Year JGBs. MoF last sold 5-year debt on 9 April 2026.

- The yield on today’s offering is 20bps higher last month’s level and sits at a fresh cycle high.

- JGB yields have risen global bond yields on inflationary concerns. That said, the rise in JGBs also likely reflects renewed concerns over the nation's fiscal policy.

- "Japanese Prime Minister Sanae Takaichi is set to announce plans soon to compile an extra budget in response to rising commodity prices driven by the ongoing Middle East conflict, according to people familiar with the matter." - BBG

- The 2s/5s curve is at a cycle high, steepest since 2006.

- Amid weak at recent auctions, today’s results will be closely watched for signs of continued weakness.

- Results are due at 0435 BST / 1235 JST.

Bloomberg Finance LP

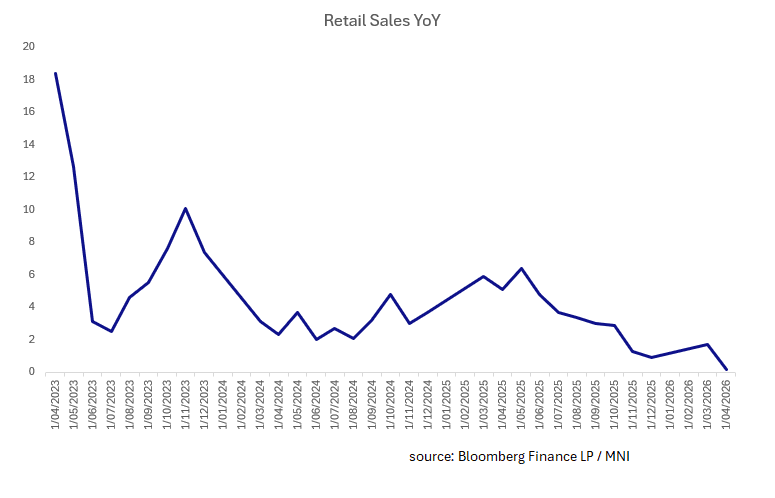

CHINA: Retail Sales Weakest Since 2022

- China's April retail sales recorded the slowest expansion since December 2022, rising just +0.2%

- Autos, construction materials, petrol products, household electronics and jewelry all posted significant falls

- China’s April retail sales reinforces that the consumer side of the economy remains under significant pressure even whilst exports and industrial production are holding up relatively well.

- China's consumers continue to agonize over falling property prices, soft wage growth, job insecurity and weak household wealth effects.

- Consumers are shifting toward services, not goods with some positive signs (for spending) in travel, restaurants, entertainment and services.

- Weak retail sales increases the pressure on Beijing and the PBOC to deliver additional support measures later this year, particularly targeted consumption stimulus or property-sector easing

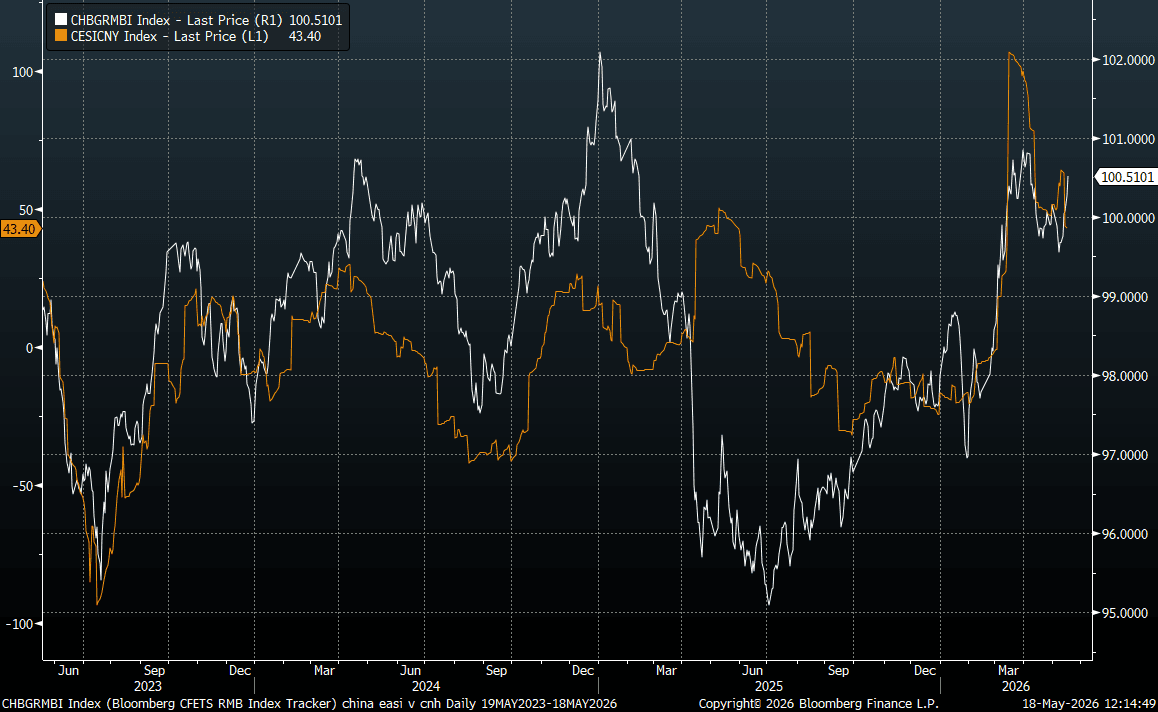

CNH: USD/CNH May Have Found Base, Data Surprise Index Coming Off High Levels

China April activity data outcomes were weaker across the board. Retail sales grew just 0.2%y/y (2.0% was forecast), while IP rose 4.1% (against a 6.0% forecast). Fixed asset investment fell 1.6%ytd y/y (against a 1.7% forecast rise). Property investment was -13.7% ytd y/y, also below forecasts. USD/CNH has tested above 6.8200 post these weaker outcomes, although aggregate moves remain modest for the pair. Highs so far rest at 6.8215, which is still comfortably under the 50-day EMA. We were last near 6.8195. Still such data outcomes may solidify a near term base in the pair around 6.8000 (particularly amidst a firmer USD backdrop).

- To be sure, China data outcomes are coming off strong levels. The chart below plots the Citi China surprise index (the orange line), which is not update yet for today's activity prints, versus the CNY basket tracker. For the most part the two series are positive correlated, so if we see more negative China data surprises it could weigh on the CNY basket.

- Headlines have crossed from the NBS: "CHINA NBS SPOKESPERSON: SHOULD IMPLEMENT MORE ACTIVE FISCAL POLICIES, MODERATELY LOOSE MONETARY POLICIES" RTRS

- The exception could be if we more concerted risk off in markets, like in parts of Q2 last year (during the tariff scare), which significantly weighed on global equity sentiment. Even with softer China outcomes we saw CNY basket tracker outperform.

Fig 1: CNY Basket Tracker Versus Citi China Surprise Index

Source: Citi/Bloomberg Finance L.P/MNI