US STOCKS: Painful Rally Pauses

The ESM5 Overnight range was 5890.00 - 5925.00, Asia is currently trading around 5898. This morning risk is opening up relatively flat in Asia after a quiet US session.

- “Cisco shares gained post market after it boosted its full-year revenue forecast in a sign AI is buoying demand. Tencent’s revenue beat on the back of a growing gaming and social media portfolio.”(BBG)

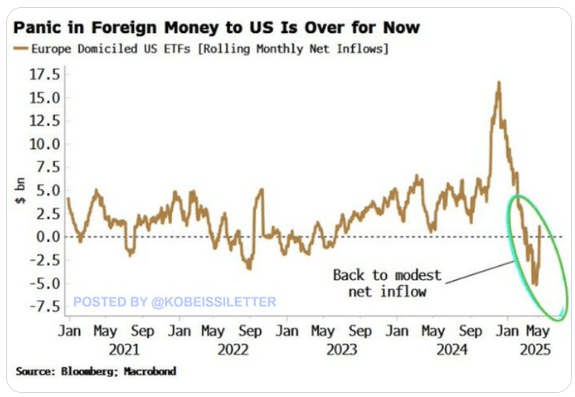

- The Kobeissi Letter on X - “Foreign investors are pouring money into US stocks again: US equity funds have attracted ~$1.5 billion in net inflows over the last month, the most since February.”

- “This comes after a net outflow of -$5 billion at the beginning of April, the most in at least 5 years.”

- “European investors have piled back into US equity funds as trade war uncertainty has eased over the last few weeks. According to the Fed data, foreigners own $18.5 trillion in US equities, reflecting ~20% of the total US equity market.” https://x.com/KobeissiLetter/status/1922773086384034220

- The move higher in US stocks finally stalled overnight to take a breathe, dips should now be supported back towards the 5700 area.

- The SPX has had a huge bounce from its lows on 4800 handle, without any pause and has left a generally bearish market completely wrong-footed. There are still very good fundamental reasons to be underweight stocks but when price moves higher like this portfolio managers are forced to react.

This move could still have more to go as the conviction of the bears is challenged but look for sellers to return back towards 6000 again as the concerns regarding Global growth and the re-allocation out of US Assets have not gone away.

Fig 1: European US ETF Flows

Source: MNI - Market News/Bloomberg/Kobeissi Letter

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE BONDS: Richer After A Solid Session For US Tsys, RBA Minutes Due

ACGBs (YM +1.0 & XM +3.0) are slightly stronger after US tsys opened in today’s Asia-Pac session little changed.

- Yesterday, risk stabilised, and US yields benefited as money was put back to work.

- The US 10-year yield is dealing in the Asia-Pac session around 4.3815%, after closing yesterday at 4.3739%.

- The US market has been forced to reduce the number of cuts it was expecting as the Fed has been consistent in saying it was worried about inflation due to the President's policies. Bostic spoke this morning: "Right now range of possible outcomes has multiplied. Inflation is still much higher than target. Not in a position to boldly move in any direction, need more clarity." (via RTRS/BBG)

- Today, the local calendar will see the release of the RBA Minutes for the April Meeting.

- Cash ACGBs are 1-3bps richer with the AU-US 10-year yield differential at -1bp.

- Swap rates are also lower with EFPs little changed.

- The bills strip has bull-flattened, with pricing flat to +4.

- RBA-dated OIS pricing is flat to 3bps softer across meetings today. A 50bp rate cut in May is given a 40% probability, with a cumulative 120bps of easing priced by year-end.

CNH: USD/CNH Holding Above 7.3100, Yuan Basket Weakness Continues

USD/CNH tracks near 7.3125/30 in early Tuesday dealings, little changed for the session so far. Post yesterday's Asia close we didn't drift too far from the 7.31/7.32 range (highs were at 7.3251), while CNH lost 0.33% for Monday's session. This underperformed softer USD index levels, although EUR, CHF and to a lessor extent JPY, stalled somewhat in terms of their rally versus the USD. Spot USD/CNY finished up at 7.3095. The CNY CFETS basket tracker, per BBG, finished up at 96.62, down a further 0.75%.

- For USD/CNH technicals, recent dips sub the 50-day EMA (near 7.2845) have been supported). Upside focus will rest with a retest of highs from last week above 7.4000. The USD/CNY fixing has continued to edge higher, helping keep USD/CNH dips supported, while also seeing CNH underperform on key crosses.

- Still, rapid yuan depreciation seems unlikely. Firstly, that may destabilize sentiment domestically and also upset potential US-China trade talks. US Trade Representative Jamieson Greer spoke earlier (on Fox News), stating that Trump expects talks with China to take place but the two sides aren't there yet (via BBG).

- Outside of continued focus on the USD/CNY fixing level, the data calendar is empty until tomorrow's Q1 GDP and monthly activity figures. House prices for March will also be out.

US TSYS: Cash Open, Slightly Mixed After Yesterday's Strong Session

TYM5 is trading 110-21, - 0-03 from its close.

- Yesterday, risk stabilised and US yields benefited as money was put back to work.

- The 10-year yield is dealing in Asia around 4.3775%, after closing at 4.3739%.

- The market has been forced to reduce the number of cuts it was expecting as the FED has been consistent in saying it was worried about inflation due to the President’s policies.

- Bostic spoke this morning: ”Right now range of possible outcomes has multiplied. Inflation is still much higher than target. Not in a position to boldly move in any direction, need more clarity.” (via RTRS/BBG)

- Treasury Secretary Scott Bessent rejects speculation that foreign nations are dumping their US Treasury holdings, citing increased foreign demand at recent auctions.

- Bessent attributes the recent bond market selloff to deleveraging, saying he has no evidence that sovereigns are behind the decline.

- He notes that the Treasury Department has tools to address dislocation if needed, including a buyback program for older securities, but says they are "a long way" from needing to take action. (via BBG)

- The 10-year yield will continue to find sellers on dips, expect any move back towards the 4.25/4.30 area to find supply.