OIL: Oil Has Strong Bounceback

- Oil prices had a strong day Thursday capping of two strong days of gains.

- WTI finished +3.5% higher in US trade at US$64.47 bbl

- The strong rally in recent days has seen WTI trade through the 20-day EMA of $64.55 for the first time since the beginning of the month.

- The recent sell off dragged all major moving averages lower and into a bearish bias.

- Brent finished stronger in US trading, rising +3.2% to reach $67.76.

- The gains sees Brent touching the 20-day EMA for the first time since the begging of the month.

- The US talks with Iran remain ongoing with Treasury Secretary Scott Bessent saying that the US would apply maximum pressure to disrupt Iran’s oil supply chain as his department sanctioned a second Chinese refinery accused of handling crude from Iran with the US suggesting the refinery has handled as much as $1bn of oil from Iran.

- Chinese refiners are importing record amounts of Canadian crude, while slashing purchases of US oil by roughly 90% amid escalating trade tensions.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

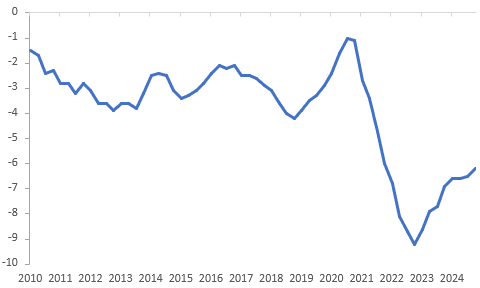

NEW ZEALAND: Strong Export Growth Drives Narrower Deficits

The Q4 current account deficit was slightly wider than expected at $7.037bn but significantly narrower than Q3’s $10.84bn. As a share of GDP it fell 0.3pp to 6.2% YTD, the lowest in three years and down 0.7pp from 2023. There was strong growth in both goods and services exports with the total up 5.4% q/q and 10.4% y/y. Imports were not as robust but still rose 2.9% q/q.

NZ current account to GDP % YTD

- Merchandise exports rose 3.8% q/q to be up 9.0% y/y in Q4 after 4.4% y/y, driven by dairy and meat. Services jumped 9% q/q to be up 13.4% y/y due to increased spending by overseas tourists while in NZ.

- Statistics NZ observed that travel exports were higher than Q4 2019 for the first time. Visitor numbers are still below pre-pandemic levels but spending is now stronger.

- Goods imports increased 3% q/q to be up 2.1% y/y after -2.4% y/y, while services rose 2.8% q/q to be up 8.7% y/y following 7.1% y/y.

- This resulted in the trade deficit narrowing $0.55bn to $1.71bn, the smallest since Q2 2021.

- There was a net outflow of $3.2bn from the financial account in Q4. As the deficit is expected to be financed by net inflows, Statistics NZ notes that the contradictions in the accounts show the difficulty in measuring investment transactions.

NZ exports vs imports y/y%

CNH: USD/CNH Holding Above Simple 200-day MA, CNY CFETS Basket To Fresh Lows

USD/CNH saw a brief dip towards the simple 200-day MA (7.2210/15) late in Asia Pac trade on Tuesday, but found support. Subsequent moves above 7.2300 drew selling interest though and we track near 7.2275 in early Wednesday dealings. The pair was unchanged for Tuesday's session. USD/CNY spot finished up at 7.2256. The CNY CFETS basket tracker, per BBG, slipped to 98.53 Tuesday, down 0.29%. This is fresh lows for the index since early Oct last year.

- For USD/CNH technicals, we are still within striking distance of the 200-day MA. A break sub this level may see round figure support at 7.2000 targeted. On the upside we have the 200-day EMA at 7.2390, but a move above 7.2500 (where the 20 and 100-day EMAs rest) is likely needed to shift the near term USD/CNH trend.

- In the cross asset space, China's equity to the rest of the world ratio continues to track higher, with a fresh wobble in US equity sentiment on Tuesday. Goldman Sachs also noted, "Foreign-exchange outflows from China plunged in February, according to a Goldman Sachs’ preferred gauge. Portfolio investments recorded net inflows, it said." (via BBG).

- USD/CNH also still looks too high relative to US-CH yield differentials, although such spreads have stabilized this past week (albeit more so in the 2yr space (last +248bps).

- There also seems little sponsorship from the CNY fixing for further strong yuan gains versus the USD. Broader USD softness may ultimately deliver lower USD/CNH and USD/CNY levels, but the yuan may continue to underperform such trends as per the continued move lower in the CNY CFETS basket.

- The data calendar is empty until tomorrow's loan prime rates, but no change is expected in the 1yr or 5yr.

US TSYS: Futures Re-Open Slightly Weaker, Focus On Wednesday’s FOMC Decision

In today's Asia-Pac session, TYM5 is 110-24, -0-01+ from closing levels.

- Yesterday, TYM5 traded 110-14 low/110-29 high, still inside initial technical levels according to MNI’s technicals team: resistance above at 111-25 (Mar 11 high), support below at 110-12.5/110-00 (Low Mar 6 & 13 / High Feb 7).

- Housing starts were far stronger than expected in February at 1,501k (1,385k expected). Building permits came close to the mark at 1,456k.

- Import price inflation was stronger than expected in February, printing 0.4% M/M (0.0% consensus, 0.4% prior after +0.1pp rev).

- Industrial production picked up strongly in February after a softer January.

- The focus turns to Wednesday's FOMC policy decision.

- Projected rate cuts through mid-2025 closed steady to softer vs. yesterday morning’s levels (*) as follows: Mar'25 steady at -.2bp, May'25 at -5.4bp ( -6bp), Jun'25 at -18.2bp (-19.7bp), Jul'25 at -26.7bp (-28.7bp).