BONDS: NZGBS: Unchanged, Local Calendar Empty Next Week

NZGBs closed unchanged, outperforming the $-bloc with the NZ-US and NZ-AU 10-year yield differential...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

ASIA STOCKS: Market Pauses Ahead of Nvidia; JCI Down for 7th Day

The Nikkei 225 fell heavily today down 1.65% and below the critical 60,000 psychological threshold for the first time this month. AI are hammered with Softbank down -6.1% and Tokyo Electron down -2.8%. Ahead of Nvidia's result, the rout started with Fujikura , which is currently down -7.8% as Fujikura’s conservative margin forecasts triggered an immediate, sector-wide exit. Japan's vital semiconductor lithography and testing ecosystem faced liquidations following Kokusai Electric (6525.JP) plunged over 6.3% following the post-market announcement that its major shareholder, KKR & Co., intends to completely block-trade its remaining stake, sparking concerns that professional investors are 'getting out at the top.'

The Jakarta Composite is down again, -1.1% today as the forced liquidation for global managers following the MSCI decision continued. The CEO of the Danantara Indonesia ‘s sovereign wealth fund, stated that state-owned enterprise (BUMN) stocks on the Indonesia Stock Exchange (IDX) are suitable for long-term investment and have shown good performance of late; in what appears to be an attempt to support stocks in a falling market. Headlines around Prabowo's focus on mining companies isn't helping sentiment either.

Both onshore and offshore bourses are down in China today by around -0.50% as some parts are disappointed by the no change on the Loan Prime Rates whilst other sectors are derisking ahead of Nvidia results. Foxconn Industrial Internet (FII) is the go-to proxy because its revenue is highly tied to Nvidia's global Blackwell and Vera Rubin server architectures. FII fell -2.3% today despite its revenue growth being poised to accelerate in 2026, driven by a new wave of robust capital expenditure from global cloud providers

BONDS: NZGBS: Cheaper After Pick Up In HH Infl Exp

NZGBs closed showing a bear-steepener, with benchmark yields 4-6bps higher. Yields moved 1bp higher post-data.

- There was a significant pickup in RBNZ measured household inflation expectations in Q2 across time periods but often not above 2025 highs. The RBNZ will need to judge if the increase is likely to be temporary following recent geopolitical events and their impact on fuel prices. There is evidence that ongoing weak demand is making it difficult for producers to pass higher input costs onto customers, but rising inflation expectations are consistent with higher core inflation.

- The NZ-US and NZ-AU 10-year yield differentials nudged 1bp and 2bps higher, respectively.

- Swap rates closed 3-5bps higher, with a steeper 2s10s curve.

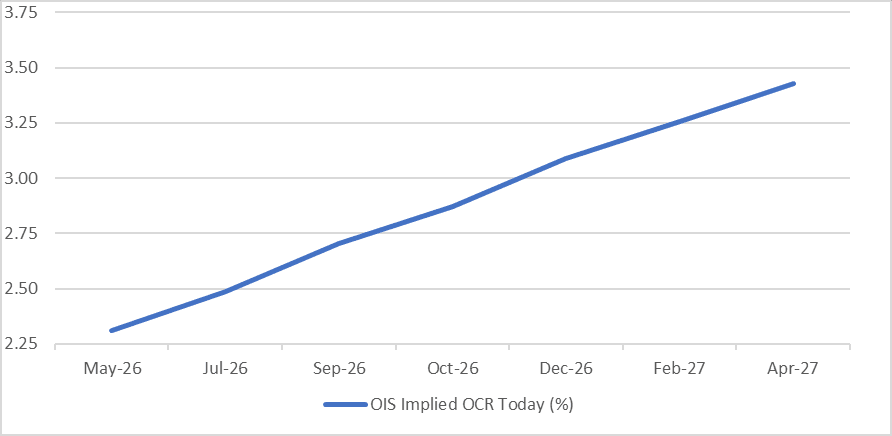

- RBNZ-dated OIS pricing is little changed across meetings. 6bps of tightening is priced for May 27, while February 2027 assigns 101bps.

- Given the near 100% probability assigned to a July hike and market’s stellar track record predicting hikes that cycle, all eyes will be on the updated RBNZ forecasts, especially its OCR profile which has often been used to signal the MPC's thinking on future decisions.

- Tomorrow, the local calendar will see Trade Balance data.

- On Thursday, the NZ Treasury plans to sell NZ$250mn of the 1.50% May-31 bond and NZ$200mn of the 4.25% May-36 bond.

Bloomberg Finance LP

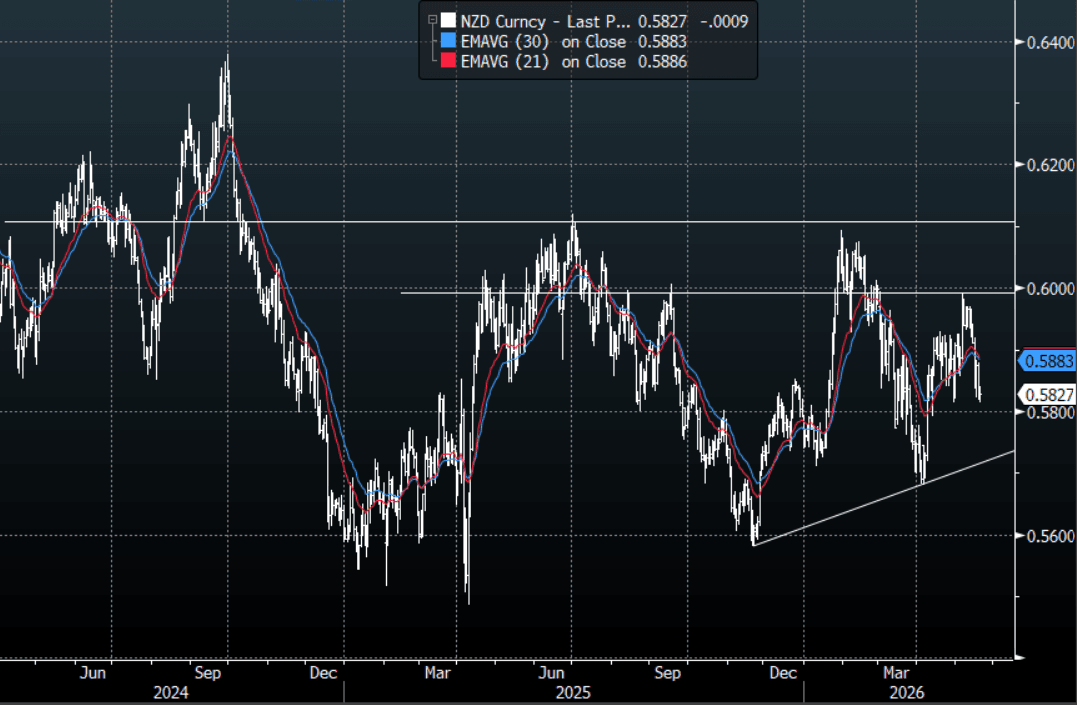

NZD: NZD/USD - Trades Heavy Just Above 0.5800, Can The USD Play Catch Up ?

The NZD/USD had a range today of 0.5815-0.5841 in the Asia-Pac session, it is currently trading around 0.5825, -0.15%. The NZD continues to find demand back toward 0.5800 and has been unable to follow through lower in the Asian session. The situation in the Middle-East remains fluid as ever but for the moment a deal looks no closer and the bond market is starting to apply real pressure to the broader risk complex. Technically the false break looks to have negated any upward momentum for now and the USD is attempting to rebound and could eventually play catch up to the move in bonds. On the day, I suspect the 0.5850-0.5880 area could now see sellers fade this initially while a deal still looks unlikely. The sellers will be looking to challenge the 0.5790-0.5810 area, a sustained break below here and the pair could move back toward its uptrend in the 0.5685-0.5715 area. Again the caveat being any announcement of a peace deal would see the USD bears re-enter the fray.

- MNI - NZ: Higher Inflation Expectations Risk To Underlying Inflation. There was a significant pickup in RBNZ measured household inflation expectations in Q2 across time periods but often not above 2025 highs. The RBNZ will need to judge if the increase is likely to be temporary following recent geopolitical events and their impact on fuel prices. There is evidence that ongoing weak demand is making it difficult for producers to pass higher input costs onto customers but rising inflation expectations are consistent with higher core inflation.

- MNI - All Eyes Will Be On RBNZ's OCR Track Next Week: RBNZ-dated OIS pricing is little changed across meetings today. Going into next week's (May 27) RBNZ policy meeting, OIS pricing shows an implied probability of a 25bp hike rising at 23%. Potentially more interesting is the fact that the market attaches a 98% probability of a 25bps hike at the July meeting.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6000(NZD380m). Upcoming Close Strikes : 0.5750(NZD524m May 22) - BBG

- The NZD/USD Average True Range for the last 10 Trading days: 47 Points

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P