POWER: Nordic Curve Could Rebound on Hydro Revisions But Bearish Pressure Noted

The Nordic forward curve may rebound on open amid downward revisions of hydro balances - albeit tren...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

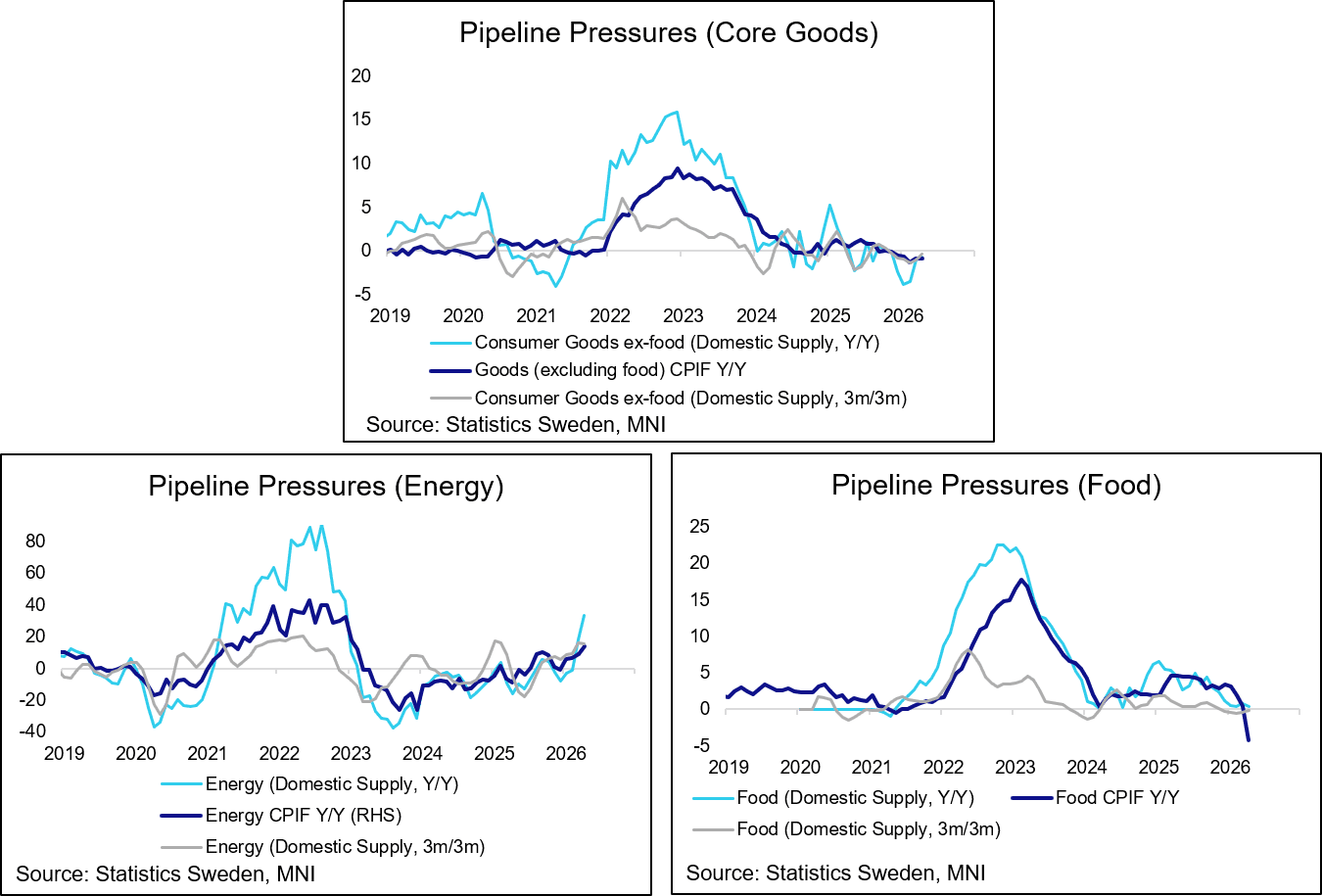

SWEDEN: Some Indications Of Broadening Pipeline Pressures

Producer price data for April pointed broadening upstream inflation pressures. While not enough to justify Riksbank action yet, it’s certainly one indicator that the Board is monitoring. This week also sees the May Economic Tendency Indicator on Thursday, which will contain important expected price plan metrics. The price index for domestic supply rose to 7.3% Y/Y (vs 3.7% prior), but this was unsurprisingly an energy story. Excluding energy, domestic supply inflation rose to 2.3% Y/Y (vs 0.5% prior), the fastest rate in 14 months. Accelerations were seen in capital goods and consumer goods ex-food, while food inflation eased back to 0.4% Y/Y (vs 0.8% in March).

EQUITY TECHS: E-MINI S&P: (M6) Path Of Least Resistance Remains Up

- RES 4: 7618.26 3.382 proj of the Apr 23 - 28 - 29 price swing

- RES 3: 7600.00 Round number resistance

- RES 2: 7597.23 3.236 proj of the Apr 23 - 28 - 29 price swing

- RES 1: 7569.75 Intraday high

- PRICE: 7540.75 @ 07:21 BST May 26

- SUP 1: 7349.80 20-day EMA

- SUP 2: 7293.50 Low May 6

- SUP 3: 7159.00 50-day EMA

- SUP 4: 7131.25 Low Apr 29

The primary trend in S&P E-Minis is bullish and a fresh cycle high, reinforces current conditions and confirms a resumption of the uptrend. The break higher maintains the bullish price sequence of higher highs and higher lows and note that moving average studies are in a bull-mode position, highlighting a dominant uptrend. Sights are on 7597.23 next, a Fibonacci projection. Initial firm support to watch lies at 7349.80, the 20-day EMA.

EURJPY TECHS: Still Looking For Gains

- RES 4: 187.95 High Apr 17 and the bull trigger

- RES 3: 187.56 High Apr 30

- RES 2: 186.56 76.4% retracement of the Apr 17 - May 6 bear leg

- RES 1: 185.46/70 High May 12 / 61.8% of Apr 17 - May 6 bear leg

- PRICE: 185.03 @ 07:29 BST May 26

- SUP 1: 183.50/182.05 Low May 07 / 06 and a bear trigger

- SUP 2: 181.87 Low Mar 16 and a key support

- SUP 3: 181.42 Low Feb 18

- SUP 4: 180.81 Low Feb 12 and a key M/T support

EURJPY remains in consolidation mode. The trend cycle is bullish and attention is on resistance at 185.46, the May 12 high. A clear break of this hurdle would strengthen a bullish theme and confirm a breach of the 50-day EMA - currently at 184.86. This would open 186.56, a Fibonacci retracement. Key support has been defined at 182.05, the May 6 low. Clearance of this level would highlight an important bearish development.