US NATGAS: Natural Gas End of Day Summary: Henry Hub Falls

Henry Hub front month has lost ground today on mixed weather forecasts.

- US Natgas SEP 25 down 0.5% at 3.09$/mmbtu

- US Natgas OCT 25 down 0.2% at 3.19$/mmbtu

- Baker Hughes US rig count: Gas: 124 (2) - up 27 rigs, or 27.8% on the year. Gas rigs have surged since mid-July and are now at their highest since August 2023.

- Meanwhile, Reuters, citing Energy Ventures Analysis, reported that weather in the immediate term doesn’t seem as bullish as in the past few weeks.

- BNEF estimates lower 48 dry gas production at 108.18 Bcf/d, down from 108.30 Bcf/d yesterday.

- U.S. dry gas consumption is estimated at 76.10 Bcf/d, down from the previous day of 80.55 Bcf/d.

- LNG net flows from the US totaled 15.11 Bcf/d, up from the previous day of 14.11 Bcf/d.

- Golden Pass LNG is expected to deliver first gas from late 2025 or early 2026 according to Exxon’s Q2 results call.

- Ongoing healthy injection rates raised European gas storage is up to 68.34% full on July 30 compared to the previous five-year average of 76.4% full, according to GIE.

- The Energos Force FSRU is due to arrive at Aqaba in Jordan on Aug. 1 to allow Jordan to import cargoes of LNG once more: ICIS.

- Asian spot LNG prices inched up after two weeks of declines as geopolitical risk factors including US threats of sanctions Russian energy lent support.

- Asian LNG imports are expected to rise in August driven by power generation demand in Japan and South Korea: BNEF.

- Brazil’s natural gas production was 181.64 mcm/d, up 20.9% on the previous year.

- Egypt’s annual LNG imports are now forecast to reach 7.9m mt in 2025, 21.5% above earlier projections: Platts

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

USDJPY TECHS: Bearish Cycle

- RES 4: 149.28 High Apr 3

- RES 3: 148.65 High May 12 and a reversal trigger

- RES 2: 146.19/148.03 High Jun 24 / 23

- RES 1: 144.97 50-day EMA

- PRICE: 143.87 @ 16:22 BST Jul 2

- SUP 1: 142.68 Low Jul 1

- SUP 2: 142.12 Low May 27 and a key short-term support

- SUP 3: 141.96 76.4% retracement of the Apr 22 - May 12 upleg

- SUP 4: 141.49 Low Apr 23

A bear threat in USDJPY remains intact and Tuesday’s sell-off reinforces this theme. The Jun 23 shooting star candle formation highlighted a reversal of the recent recovery and this signal remains in play. Note too that price has traded through the 20- and 50-day EMAs. A clear break of the EMAs strengthens a bearish threat and opens 142.12, the May 27 low and a key short-term support. Initial resistance is at 144.97, the 50-day EMA.

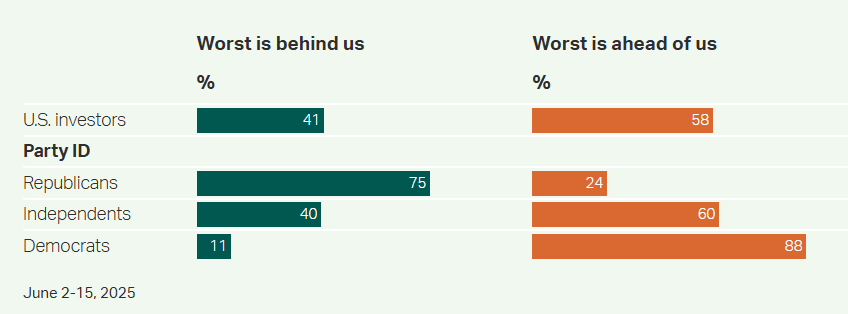

US: Partisan Split Widens On Market Volitility Expectations In 2025 - Gallup

A new survey from Gallup has found that, “Most investors foresee volatility persisting through 2025 and believe the worst is still to come, rather than “behind us.” Despite this, investor confidence in the stock market as a means of building retirement wealth remains high.”

- Gallup notes: “Democratic investors (48%) are far more likely than Republican investors (9%) to say they are very concerned about recent stock market volatility and are twice as likely to be very or somewhat concerned overall (82% vs. 41%). Concern among independents falls between the two partisan groups, similar to the national average.”

Figure 1: "In terms of market volatility this year, do you think the worst is behind us or the worst is ahead of us?"

Source: Gallup

US OUTLOOK/OPINION: Specific Private Industries Worth Watching In NFP Report

- Within industries of nonfarm payrolls, expect a continued focus on those more cyclically sensitive sectors, such as food & drinking places, for discretionary spending indicators.

- This category saw notable strength in May at +30k after +23k in April (average +11k in 2024) but maybe scope for a downward revision.

- Friday saw real consumer spending disappoint in May at -0.3% M/M (cons 0.0) with particular weakness admittedly in goods (-0.8%) but services also languished with -0.03% M/M for technically a third monthly contraction in the five months of the year to date.

- There could also be a calendar effect at play, with BofA warning that the earlier Memorial Day could weigh on leisure & hospitality more broadly.

- Transportation & warehousing should also be watched for a look at more direct impacts from US tariff policy. Recall that this category saw large downward revisions last month, leaving payrolls growth of +6k in May after -8k in April (initially +29k) and -21k in March (+3k) and changing a narrative around implications of inventory accumulation on warehousing roles in particular.

- The latest vintage points to a recent net negative impact from tariffs now having peaked with 28k and 34k monthly increases back in Nov and Dec.

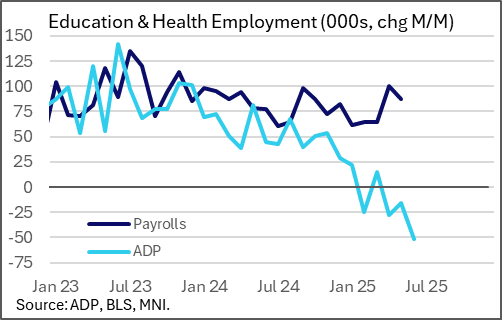

- Education & health services will also be watched closely after today's ADP employment report showed a yet further widening in what has been a puzzling disconnect with BLS payrolls.