US TSYS: Modest Late Reversal W/ US/Iran Talks "Back On", Domestic Data Resumes

- Treasuries see-sawed back in range late Monday, curves twisting steeper with the short end outperforming after the bell (2s10s +2.227 at 71.610).

- Currently, TYH6 trades -.5 at 111-18.5 (111-15.5 low / 111-23.5 high), gains are considered corrective and for bears, sights are on key support at 111-09, the Jan 20 low. Clearance of this level would confirm a resumption of the downtrend.

- Risk-off to risk-on (less off): midday support for Tsys, equities weaker after Axios story making the rounds that plans for US/Iran talks on Friday are collapsing w/subject of nuclear weapons, missile program a non-starter.

- The geopol risk narrative cooled late: US Iran talks "back on" according to Barak Ravid posts on X - crude retreated from earlier highs, WTO appr 64.50 vs. 65.53 high. Stocks reacting positively (Nasdaq still underperforming with chip and software services stocks underperforming).

- Economic data to resume with stop-gap funding bill through September signed by Pres Trump late Tuesday, JOLTS expected Thursday at 1000ET, NFP on Feb 11, CPI pushed to Feb 13. Both the BOE and ECB decisions expected too.

- The USD index has matched the most recent recovery highs at 97.73 and has weighed on the precious metals space, with spot gold briefly extending an impressive intraday pullback to print around $4,850 after reaching a $5,091 high overnight.

- Meanwhile earnings expected after the close include: Allstate Corp, McKesson Corp, Alphabet Inc, O'Reilly Automotive, Coherent Corp, Snap Inc and QUALCOMM.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

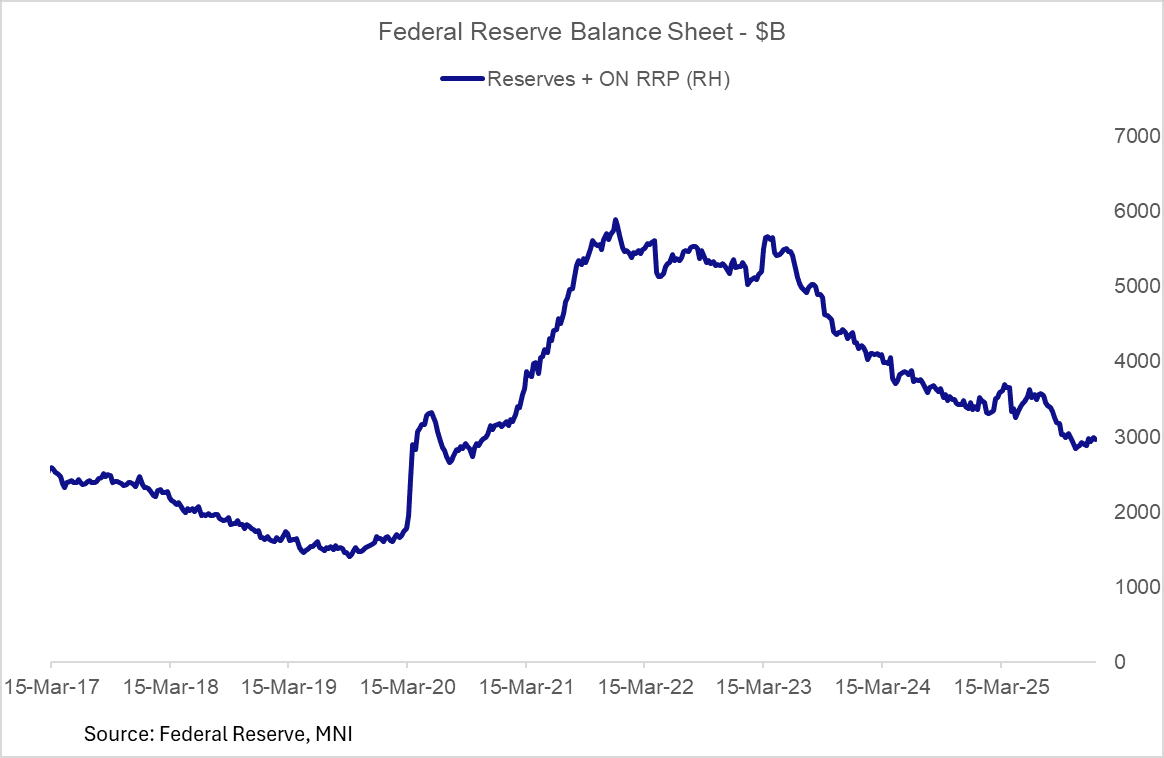

FED: Reserves End Year On Low Note, Set To Pick Up In Coming Months (1/2)

Reserves ended 2025 on a down note, with a $127B fall in the week to Dec 31 (per the Federal Reserve's holiday-delayed H.4.1 statement out late Friday). This was the biggest drop in reserves since mid-September, and came as Treasury cash jumped $71B with overnight reverse repo jumping $101B.

- This was largely down to year-/quarter-end effects, reflected in a jump in funding rates at the time, and will be reversed over the coming 1-2 weeks.

- The $2.85T reserve level was the lowest since the first week of November.

- The bigger picture though is that reserves + ON RRP combined have edged slightly higher since the Fed's decision on Oct 29 to end QT on Dec 1.

- Reserves should continue to pick up above the $3T mark in the coming months amid reserve management purchases - the NY Fed's latest Survey of Market Expectations has a median expectation of reserves gradually hitting $3T by Q4 2026.

AUDUSD TECHS: Bullish Trend Sequence

- RES 4: 0.6858 1.000 proj of the Nov 21 - Dec 10 - 18 price swing

- RES 3: 0.6795 0.764 proj of the Nov 21 - Dec 10 - 18 price swing

- RES 2: 0.6759 High Oct 11 ‘24

- RES 1: 0.6728 High Dec 29 and the bull trigger

- PRICE: 0.6715 @ 17:14 GMT Jan 5

- SUP 1: 0.6657 20-day EMA

- SUP 2: 0.6608 50-day EMA

- SUP 3: 0.6593 Low Dec 18

- SUP 4: 0.6553 Low Dec 3

The trend condition in AUDUSD is unchanged, it remains bullish and strong gains between Dec 18 - 26, reinforce current conditions. The pair has cleared a key resistance at 0.6707, the Sep 17 high. The breach confirms a resumption of the medium-term uptrend that started Apr 9. This signals scope for an extension towards 0.6759 next, the Apr 11 2024 high. Initial firm support to watch lies at 0.6657, the 20- day EMA.

EGB SYNDICATION: Slovenia 10-year: Priced (from 1700GMT)

Deal priced at 1700GMT. Posting details for completeness

- Reoffer yield/price: 3.312% / 99.675%

- Size: E1.75bln (MNI expected E1.5bln)

- Benchmark 10Y Fixed (March 12, 2036) at MS+37 (Revised Guidance was MS+40 Area, Guidance was MS+45)

- Coupon: 3.275% Annual, act/act ICMA, long first

- Books closed above E10bln (including E912mln JLM interest): Leads

- Hedge Ratio: 104% vs 2.6% Aug-35 Bund

- Settlement: Jan. 12, 2026 (t+5)

- ISIN: SI0002105227

- Bookrunners: Barclays (B&D), DZ Bank, HSBC, JPM, OTPBSI, RBI

Details as per market source, with MNI colour.