MNI US OPEN - BoE Rate Cut Bets Rise Following Soft CPI

EXECUTIVE SUMMARY

- UK INFLATION DATA LESS OF A SURPRISE THAN IT APPEARS

- FED'S BOSTIC REPEATS PREFERENCE FOR 1 CUT THIS YEAR

- BOJ'S ADACHI SEES CONDITIONS FOR NORMALISATION

- NEW ZEALAND Q3 INFLATION IN-LINE WITH EXPECTATIONS AT 2.2% Y/Y

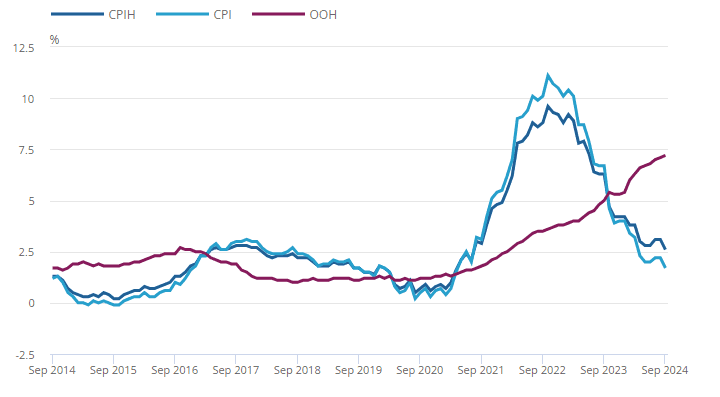

Figure 1: UK headline inflation slows to near 3-1/2 year low

Source: ONS

NEWS

FED (MNI): Fed's Bostic Repeats Preference For 1 Cut This Year

Federal Reserve Bank of Atlanta President Raphael Bostic Tuesday said he sees the need for one more interest rate cut this year but is remaining open to a cut in November. "I'm keeping my eyes open. I'm keeping my options open," Bostic said in a moderated discussion. "I'm allowed to have information inform me moving forward and that's what I'm going to do. The data for much of this year, inflation has gone faster than I expected. If that continues, I'll be comfortable doing another 25 but the data will tell me that."

US (BBG): Harris Has 48% Backing, Trump 47% in Marquette National Poll

Democratic presidential candidate Kamala Harris has 48% support and Republican candidate Donald Trump has 47% backing among likely voters, a Marquette Law School Poll national survey shows. Survey of 699 likely voters nationwide was conducted Oct. 1-10 online; margin of error +/- 4.7 percentage points.

US (WSJ): Harris Sharpens Negative Attacks on Trump

When Vice President Kamala Harris walked off the stage of her rally in Erie, Pa., which included a video compilation of Donald Trump’s recent comments about “the enemy from within,” she told her campaign staff that she wanted to keep using the former president’s own words against him, advisers said.

US (BBG): Trump Defends Tariff Plan While Pressing for More Fed Influence

Republican presidential candidate Donald Trump defended his plans to overhaul the US economy through dramatic tariff increases and more direct consultation with the Federal Reserve, arguing that his policies would result in substantial growth despite projections that his agenda would fuel inflation and spike the national debt. “It’s going to have a massive effect, positive effect,” Trump told Bloomberg News Editor-in-Chief John Micklethwait on Tuesday in an interview at the Economic Club of Chicago.

US/S.KOREA (BBG): Trump Says ‘Money Machine’ Korea Should Pay More for US Troops

Republican presidential candidate Donald Trump said South Korea would pay billions of dollars more every year to host US troops if he were in the White House, calling the long-time US ally a “money machine.” “If I were there now, they’d be paying us $10 billion a year and you know what, they’d be happy to do it,” Trump told Bloomberg News Editor-in-Chief John Micklethwait on Tuesday in an interview at the Economic Club of Chicago. “It’s a money machine, South Korea.”

ISRAEL/MIDEAST (BBG): Israel Says It Struck Hezbollah Weapons Depot in Beirut

Israel’s air force struck targets in Beirut for the first time in almost a week, and the US warned it could cut arms supplies if the humanitarian crisis in Gaza doesn’t improve. The Israel Defense Forces said it conducted the strike early Wednesday on an underground weapons-storage site in the southern suburbs of Beirut, a stronghold of the Iran-backed Hezbollah militant group. The airstrike came just hours after Lebanon’s prime minister said the US had assured him that Israeli attacks on the capital would ease.

EUROPE (FT): Shares in Luxury and Consumer Brands Fall on LVMH Warning

European luxury goods and consumer goods stocks fell on Wednesday after LVMH warned of an “uncertain economic and geopolitical environment” as it missed earnings expectations. Shares in the French luxury group dropped 5.1 per cent in Paris while Kering, owner of the Gucci brand, fell 4.1 per cent. Profits for luxury goods companies have been under pressure this year as consumer spending in China has failed to regain momentum after the pandemic.

UK (BBG): Keir Starmer Aides Engage With ‘Non-Doms’ Amid Wealth Tax Fight

UK Prime Minister Keir Starmer’s political aides plan to confer with advocates for the nation’s so-called non-dom population of wealthy foreigners amid concerns his Labour Party’s intended tax hikes may end up costing money. Business and investment advisers for 10 Downing Street are scheduled to meet with the head of Foreign Investors for Britain, a lobbying group for wealthy individuals created in response to proposals to change Britain’s non-dom system, according to a person familiar with the matter.

BOJ (MNI): BOJ's Adachi Sees Conditions For Normalisation

Bank of Japan board member Seiji Adachi said on Wednesday conditions for policy normalisation had been satisfied, but the BOJ should avoid drastic monetary-policy adjustment. “It is appropriate for the BOJ to raise the policy rate gradually,” Adachi told business leaders in Takamatsu City. However, Adachi did not elaborate on when and how the Bank would raise the policy interest rate. The BOJ must keep accommodative financial conditions and raise the policy rate at a very moderate pace until 2% underlying inflation is achieved in a stable and sustainable manner, he continued.

CHINA/RUSSIA (MNI): PMs Talk Up Links at SCO Summit Ahead of Xi/Putin Meeting at BRICS

MNI (London) During a meeting on the sidelines of the Shanghai Cooperation Organisation (SCO) summit in Islamabad, Pakistan with Russian PM Mikhail Mishustin, Chinese Premier Li Qiang said "China is willing to further deepen cooperation with Russia in traditional fields such as economy, trade, and energy, promote cooperation in emerging fields such as the digital economy, continuously improve the level of cooperation in the industrial chain and supply chain between the two countries," according to state outlet Xinhua.

CHINA (BBG): China to Extend Record Aluminum Output Amid Ample Power

China’s record-breaking run of aluminum output is likely to extend through the rest of the year as supply risks dissipate at a key production base in the south of the country. National output is expected to rise 3% in the fourth quarter from a year ago to 11 million tons, according to Shanghai Metals Market. The forecast assumes that smelters in Yunnan will escape production cuts for the first time in four years due to abundant electricity supplies.

RBA (MNI): RBA Sees Anchored Inflation Expectations - Hunter

The Reserve Bank of Australia is confident inflation expectations remain well anchored, with short-term notions of price rises appearing to converge towards the long-term outlook. In an industry presentation on Wednesday, Assistant Governor and Chief Economist Sarah Hunter noted there was no evidence of expectations being more persistent than normal. “Recent research has improved our understanding of how people form inflation expectations,” she said. “As a result, we have been able to better analyse how expectations have evolved during the recent high-inflation period and it’s a good news story with respect to expectations.”

COMMODITIES (BBG): World Set for Cheaper Energy on Shift From Oil and Gas, IEA Says

The world is heading into an era of cheaper energy prices as a shift towards electricity use leaves behind surpluses of oil and gas, the International Energy Agency predicted. Global demand for all fossil fuels will stop growing this decade, while supplies of oil and LNG are set to climb, the IEA forecast in its annual long-term report. Meanwhile, an ongoing surge in electricity consumption led by China is on track to accelerate, it said.

DATA

UK DATA (MNI): Inflation Data Less of a Surprise Than It Appears

- UK SEP CPI +0% M/M, +1.7% Y/Y

- UK SEP CORE CPI +0.1% M/M, +3.2% Y/Y

- UK SEP SERVICES CPI -0.3% M/M, +4.9% Y/Y

- UK SEP OUTPUT PPI -0.5% M/M, -0.7% Y/Y

- UK SEP INPUT PPI -1% M/M, -2.3% Y/Y

Transport is the biggest downward contributor here - contributing -0.49ppt of the 0.53ppt headline fall. Air fares contributed -0.22ppt to headline CPI alone - that is reversing their rise last month. Fuels and lubricants fell 3.4%M/M, contributing -0.22ppt to the headline CPI Y/Y change. That's a little less of a fall than the c. 4% M/M fall we had seen analysts pencil in. There is no change in education's Y/Y contribution (some had expected this if there were early VAT changes to private school fees). Food and non-alcoholic beverages rose 1.86% Y/Y (up from +1.34% Y/Y in August) that's more than expected.

In terms of impact for the BOE. Given that a large part of the surprise was driven by air fares, it's not as big a surprise as at first glance. Overall, services CPI at 4.94% Y/Y is 0.58ppt below the BOE's August MPR forecast - that is partly driven by air fares, partly by hotel prices not being as strong as they were a few months ago, and then a very slight broad-based softening elsewhere. Core goods at 0.20% Y/Y are higher than the BOE's forecast of -0.02% Y/Y, food prices are higher at 1.86% Y/Y vs 1.19% but energy is also softer than expected (due largely to petrol prices). These probably broadly offset each other - leaving the BOE's headline surprise driven by services.

ITALY DATA (MNI): Risk of Downward EZ Revision After Italian Final Sep Data

- ITALY FINAL HICP +1.2% M/M, +0.7%Y/Y

Italian September final headline HICP was revised a tenth lower on an annual basis to 0.7% Y/Y. Taken alongside the downward revision to the French data yesterday, there may be larger-than-usual risks of a revision to the Eurozone-wide flash print tomorrow (which was 1.77% Y/Y on an unrounded basis). A two tenths downward adjustment to food, alcohol and tobacco inflation (to 1.4% Y/Y) drove the headline revision in Italy. Italian core inflation (ex-energy, food, alcohol and tobacco) was confirmed

at 1.8% Y/Y (vs 2.3% prior), with services at 3.1% Y/Y (unch vs flash, vs 3.4% prior) and core goods at -0.1% Y/Y (vs -0.2% flash and 0.3% prior).

JAPAN AUG CORE MACHINE ORDERS -1.9% M/M; JULY -0.1% (MNI)

NEW ZEALAND (MNI): NZ Q3 Inflation Prints at 2.2% Y/Y

New Zealand September quarter CPI printed at 2.2% y/y, down from Q2's 3.3%, in line with market expectations and 10 basis points lower than the Reserve Bank of New Zealand’s most recent forecasts. Non-tradeable inflation printed at 1.3% q/q, in line with expectations, while tradeable price rises fell 0.2% - 10bp more than anticipated.

The RBNZ cut the OCR 50bp to 4.75% last week, noting it was confident inflation would fall back towards the midpoint of its 1-3% target band. Stats NZ noted inflation was still supported primarily by local government rates, up 12.2%, vegetables, up 8.4% and pharmaceutical products, which increased 17%.

FOREX: Markets Look to Budget for Next Leg in GBP

- GBP/USD's break lower Wednesday puts the pair through support at both the 1.3002 level as well as the 1.30 handle - making for a second key technical break across major markets this week. Soft UK inflation data drove the spot price lower, as markets sharply raised the implied probability of back-to-back BoE rate cuts for the November and December meetings. 44bps of rate cuts are now priced by year-end, up from ~36bps before this morning's release.

- The next focus for G10 FX will be the sustainability of the next GBP leg lower. The 100-dma undercuts as next support at 1.2953, and it's this level that could come into focus headed into the UK Budget on October 30th - at which the Chancellor is looking to raise as much as £40bln in tax revenues to plug the black hole in government finances.

- The greenback is the firmest currency in G10, aided by both the GBP/USD leg lower and the persistent buy-on-dips theme in USD/JPY. This keeps Y150.00 in view for the pair, clearance of which would resume the underlying uptrend posted off the mid-September lows.

- European equities are soft - with continental indices off 0.4-1.0% and extending losses posted off yesterday's highs. Earnings remain the key driver here, with the EuroStoxx50's two biggest stocks (LVMH and ASML) both posting sharp declines on their updates this week. The next key release comes next week, with SAP's Q3 performance update on the 21st October.

EGBS: Stronger Following UK CPI, European Equity Pullback

EGBs have taken cues from Gilts and European equities this morning, with today’s regional macro calendar limited.

- Lower-than-expected UK CPI drove the initial bid in Bund futures, while European stocks remain under pressure following yesterday’s weaker-than-expected LVMH and ASML earnings.

- Bund futures are +25 at 134.00, a little above the first resistance at the 20-day EMA. A clear break of this average is required to counter a bearish technical theme.

- 10-year peripheral spreads to Bunds have narrowed away from opening wides, with the BTP/Bund spread now little changed at 124bps (the spread closed at its tightest since mid-March yesterday at 123.5bps).

- Italian Finance Minister Giorgetti is currently delivering a press conference on the 2025 budget, which was approved by the Cabinet last night.

- 30-year Bund supply is due at 1030BST/1130CET.

GILTS: Rally Extends

The post-CPI rally in gilts extends, with futures through initial reissuance at the 20-day EMA (97.68).

- Contract last +93 at 97.84, vs. recent session highs of 97.85.

- Bulls eye key near-term resistance at the September 2 low (98.11).

- Yields 6-10bp lower, curve bull steepens.

- 10-Year gilt yields extend yesterday’s move back below broken downtrend resistance drawn off the October ’23 peak. September 2 high (4.061%) the next downside target.

- 2s10s and 5s30s stick within multi-week ranges.

- 10-Year spread vs. Bunds back below 190bp, 5.5bp tighter on the day.

- GBP3.5bln 4.00% Oct-31 supply generated strong demand.

- BoE-dated OIS show ~25bp of easing for November, 42.5bp of cuts through year-end and 113.5bp of cuts through June ‘25, 3-11bp more dovish on the day.

- We don’t think the BoE will entertain the idea of a 50bp cut at this juncture, given still elevated (but cooling) wage growth and services inflation.

- The profile of cuts through the second half of ’25 still looks quite flat, despite today’s repricing.

- Looking ahead, a more austere Budget (which the latest round of press reports has indicated is in the offing) could facilitate further dovish repricing for ’25 meetings, as well as promoting cross-market gilt tightening.

EQUITIES: Eurostoxx 50 Futures Pierce 50-Day EMA Following Tuesday's Sell-Off

Eurostoxx 50 futures traded sharply lower Tuesday, reversing recent gains. The contract has pierced support around the 50-day EMA, at 4944.57. A clear break of this average would undermine a recent bullish theme and highlight a stronger reversal. This would open 4884.06, a Fibonacci retracement. Key resistance and bull trigger is unchanged at 5106.00, the Sep 30 high. A break would resume the uptrend. A bull cycle in S&P E-Minis remains intact and Tuesday’s pullback appears to be a correction. Recent gains confirm a resumption of the primary uptrend and maintain the bullish price sequence of higher highs and higher lows. Note that moving average studies are in a bull-mode setup, highlighting a dominant uptrend. Sights are on 5961.00, a Fibonacci projection. Initial support to watch is 5789.86, the 20-day EMA.

- Japan's NIKKEI closed lower by 730.25 pts or -1.83% at 39180.3 and the TOPIX ended 32.91 pts lower or -1.21% at 2690.66.

- Elsewhere, in China the SHANGHAI closed higher by 1.656 pts or +0.05% at 3202.948 and the HANG SENG ended 31.94 pts lower or -0.16% at 20286.85.

- Across Europe, Germany's DAX trades lower by 35.76 pts or -0.18% at 19451.91, FTSE 100 higher by 51.32 pts or +0.62% at 8300.87, CAC 40 down 47.49 pts or -0.63% at 7474.48 and Euro Stoxx 50 down 38.12 pts or -0.77% at 4908.61.

- Dow Jones mini down 23 pts or -0.05% at 42995, S&P 500 mini down 0 pts or 0% at 5862.75, NASDAQ mini up 15.25 pts or +0.08% at 20356.75.

Time: 09:50 BST

COMMODITIES: Further Weakness in WTI Futures Would Threaten Bullish Theme

WTI futures gapped lower yesterday and this resulted in a break of the Oct 9 low. An extension lower would threaten the recent bullish theme and expose support at $66.33, the Oct 1 low, and $64.61, the Sep 10 low and a key support. For bulls, a resumption of gains would instead refocus attention on the key short-term resistance at $78.46, the Oct 8 high. Clearance of this level would resume to the recent uptrend. Gold is trading higher this week and the recent short-term retracement appears to have been a correction. The trend condition is bullish and moving average studies are in a bull-mode set-up too, highlighting a clear uptrend and positive market sentiment. Sights are on $2690.2, a Fibonacci projection. Firm support lies at $2626.7, the 20-day EMA. It has been pierced, a clear break would signal scope for a deeper retracement.

- WTI Crude up $0.08 or +0.11% at $70.61

- Natural Gas down $0.01 or -0.52% at $2.483

- Gold spot up $14.91 or +0.56% at $2677.45

- Copper up $3.3 or +0.76% at $437

- Silver up $0.31 or +0.98% at $31.8048

- Platinum up $8.81 or +0.89% at $997.36

Time: 09:50 BST

| Date | GMT/Local | Impact | Country | Event |

| 16/10/2024 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 16/10/2024 | 1215/0815 | ** | CMHC Housing Starts | |

| 16/10/2024 | 1230/0830 | ** | Import/Export Price Index | |

| 16/10/2024 | 1230/0830 | ** | Monthly Survey of Manufacturing | |

| 16/10/2024 | 1840/2040 | ECB's Lagarde Speech at Banka Slovenije Dinner | ||

| 17/10/2024 | - | European Central Bank Meeting | ||

| 17/10/2024 | 2350/0850 | ** | Trade | |

| 17/10/2024 | 0030/1130 | *** | Labor Force Survey | |

| 17/10/2024 | 0900/1100 | *** | HICP (f) | |

| 17/10/2024 | 0900/1100 | * | Trade Balance | |

| 17/10/2024 | 1100/0700 | *** | Turkey Benchmark Rate | |

| 17/10/2024 | 1215/1415 | *** | ECB Deposit Rate | |

| 17/10/2024 | 1215/1415 | *** | ECB Main Refi Rate | |

| 17/10/2024 | 1215/1415 | *** | ECB Marginal Lending Rate | |

| 17/10/2024 | 1230/0830 | *** | Jobless Claims | |

| 17/10/2024 | 1230/0830 | * | International Canadian Transaction in Securities | |

| 17/10/2024 | 1230/0830 | *** | Retail Sales | |

| 17/10/2024 | 1230/0830 | ** | Philadelphia Fed Manufacturing Index | |

| 17/10/2024 | 1245/1445 | ECB Monetary Policy Press Conference | ||

| 17/10/2024 | 1315/0915 | *** | Industrial Production | |

| 17/10/2024 | 1400/1000 | * | Business Inventories | |

| 17/10/2024 | 1400/1000 | ** | NAHB Home Builder Index | |

| 17/10/2024 | 1415/1615 | ECB Podcast: Lagarde presents MonPol Decision | ||

| 17/10/2024 | 1430/1030 | ** | Natural Gas Stocks | |

| 17/10/2024 | 1500/1100 | ** | DOE Weekly Crude Oil Stocks | |

| 17/10/2024 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 17/10/2024 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 17/10/2024 | 2000/1600 | ** | TICS | |

| 17/10/2024 | 2000/2100 | BOE's Woods Speech at Mansion House |