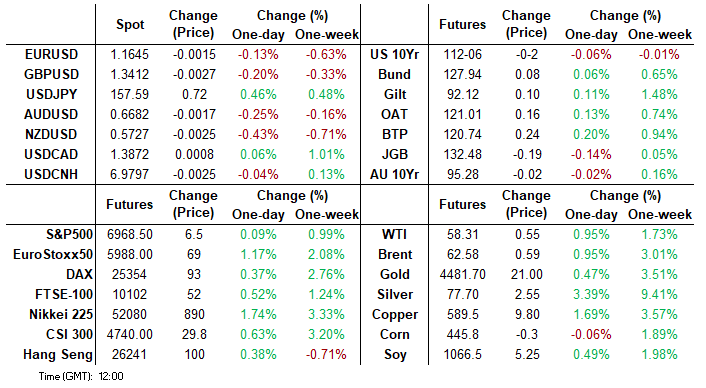

MNI US MARKETS ANALYSIS - NFP Next, Tariff Ruling a Tail Risk

Highlights:

- Jobs data in focus, but lingering impact of shutdown data collection could muddy interpretation

- USD Index at new YTD high ahead of NFP data, USDJPY bid

- Tariff ruling a tail risk, publication could be from 1000ET... or not at all

US TSYS: TYH6 Support Exposed Ahead Of NFPs & Potential IEEPA Ruling

Treasuries have extended yesterday’s net losses, with most benchmark tenors more than reversing a sharp rally ahead of the close (when Trump called for $200bn of mortgage bond purchases). The nonfarm payrolls report for December dominates initial proceedings in what should be a cleaner report after last month’s release. Attention then likely turns to a potential Supreme Court ruling on the legality of the White House's IEEPA tariffs - the justices sit at 1000ET but it's not certain given that they do not announce in advance what opinions that they are providing.

- Cash yields are 1.6-2.3bps higher on the day, led by the belly.

- 5s30s has flattened further to 110bp, last lower on Dec 26 having recently peaked at 116bp on Jan 6.

- TYH6 sits 1 tick above a session low of 112-05 (-03) seen earlier in London trade, currently with reasonable cumulative volumes of 320k ahead of NFPs.

- Support remains exposed with 112-01+ (Dec 23 low) before the bear trigger at 111-29 (Dec 10 low), whilst resistance is seen at 112-22 (Jan 7 high) before 112-25+ (Dec 30/31 high).

- Data: Payrolls Dec (0830ET), Housing starts/building permits Sep-Oct (0830ET), U.Mich consumer survey Jan prelim (1000ET), Household net worth Q3 (1200ET)

- Fedspeak: Kashkari opening remarks (1000ET), Bostic interviewed on WLRN public media (1200ET), Barkin repeats his speech on the economic outlook but will also give Q&A (1335ET)

- Politics: Trump in meeting with oil & gas execs

- Tariffs, potentially: Supreme Court Opinion Day (1000ET)

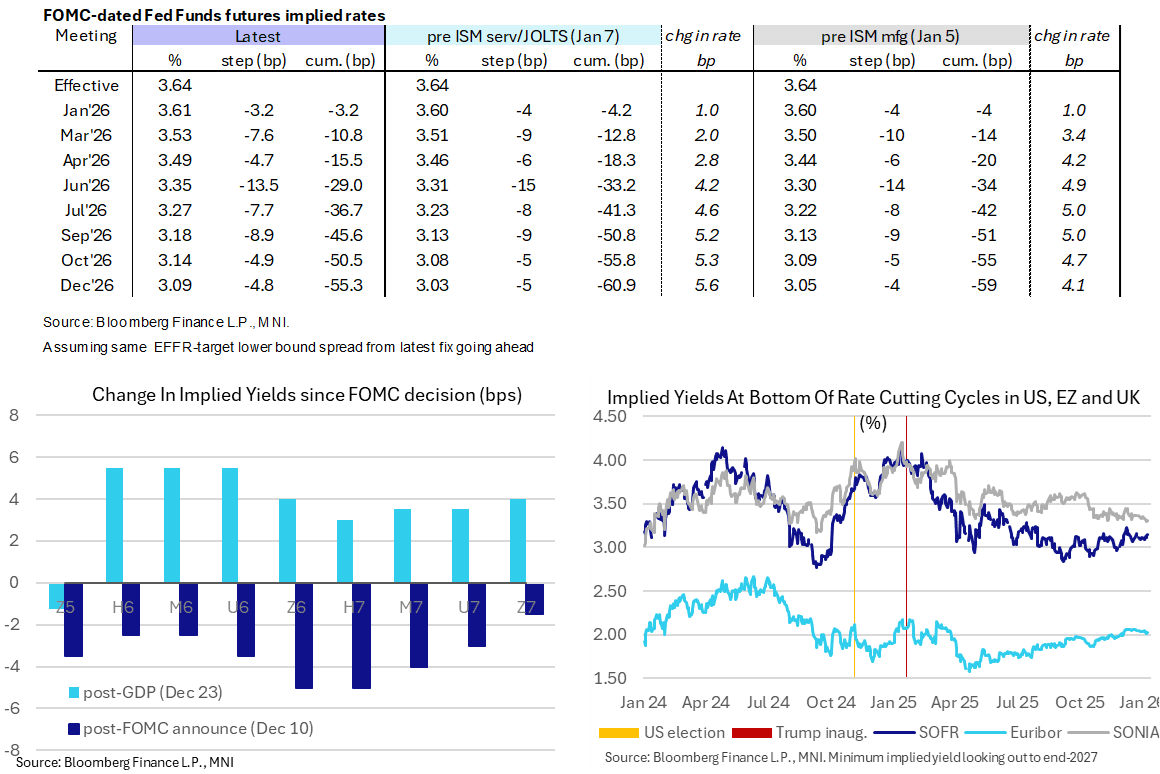

STIR: Holding Hawkish Shift In Fed Rates Ahead Of NFPs, Potential IEEPA Ruling

- Fed Funds implied rates are little changed overnight for near-term FOMC meetings but ~1bp higher for 2H26, extending yesterday’s modest hawkish shift on lower tier US data and much firmer oil prices.

- There are 5bps fewer cuts priced to end-2026 than prior to Wednesday’s ISM services beat.

- Today’s focus is clearly on the nonfarm payrolls report for December, which we characterize as likely being a cleaner but not entirely fogless release after last month’s particularly messy release (preview link). Potential for a Supreme Court ruling on IEEPA tariffs will also feature heavily.

- Cumulative cuts from 3.64% effective: 3bp Jan, 11bp Mar, 15.5bp Apr, 29bp Jun, 45.5bp Sep and 55.5bp Dec.

- SOFR futures are 2-2.5 ticks lower through 2H26 to end-2027 contracts in contrast to broadly flat European rates.

- The terminal implied yield has climbed to 3.15% (Z6) having last closed higher on Dec 23 after a boost from strong GDP growth at the time.

SOFR: Net Short Setting Dominated In Futures On Thursday

OI data points to net short setting providing the most prominent positioning swing as most SOFR futures ticked lower on Thursday, Limited instances of net long cover were seen.

| 08-Jan-26 | 07-Jan-26 | Daily OI Change |

| Daily OI Change In Packs |

SFRZ5 | 1,448,688 | 1,463,580 | -14,892 | Whites | +28,104 |

SFRH6 | 1,344,921 | 1,318,857 | +26,064 | Reds | +23,956 |

SFRM6 | 1,187,549 | 1,174,303 | +13,246 | Greens | +17,488 |

SFRU6 | 1,246,066 | 1,242,380 | +3,686 | Blues | +3,340 |

SFRZ6 | 1,221,590 | 1,219,597 | +1,993 |

|

|

SFRH7 | 866,271 | 864,715 | +1,556 |

|

|

SFRM7 | 772,185 | 755,007 | +17,178 |

|

|

SFRU7 | 771,481 | 768,252 | +3,229 |

|

|

SFRZ7 | 857,703 | 849,037 | +8,666 |

|

|

SFRH8 | 475,291 | 473,534 | +1,757 |

|

|

SFRM8 | 426,615 | 421,547 | +5,068 |

|

|

SFRU8 | 372,081 | 370,084 | +1,997 |

|

|

SFRZ8 | 351,630 | 347,739 | +3,891 |

|

|

SFRH9 | 217,632 | 218,218 | -586 |

|

|

SFRM9 | 215,052 | 215,481 | -429 |

|

|

SFRU9 | 166,402 | 165,938 | +464 |

|

|

US TSY FUTURES: Mix Of Short Setting & Long Cover Seen On Thursday

OI data points to a mix of net long cover (TU, FV, UXY & WN) and short setting (TY & US) as Tsy futures ticked lower on Thursday, with the former dominating in net curve-wide terms even as the largest DV01 swing came in TY positioning.

| 08-Jan-26 | 07-Jan-26 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,513,232 | 4,522,628 | -9,396 | -360,570 |

FV | 6,688,150 | 6,738,109 | -49,959 | -2,176,535 |

TY | 5,575,730 | 5,574,958 | +772 | +51,301 |

UXY | 2,566,420 | 2,581,625 | -15,205 | -1,365,016 |

US | 1,888,482 | 1,871,749 | +16,733 | +2,314,125 |

WN | 2,084,989 | 2,091,301 | -6,312 | -1,155,412 |

|

| Total | -63,367 | -2,692,106 |

IRAN: Internal & External Factors At Play Amid Escalating Protests

Comments from Supreme Leader Ayatollah Ali Khamenei are being reported as he delivers a televised address regarding the ongoing protests. Says that "There are some rioters who want to please the American president by damaging public property", but that Iran "won't back down in the face of vandalism". Says Iran will not "tolerate foreign-backed operatives". Says that President Donald Trump "should focus on running his own country". Claims that Trump "will be overthrown at the peak of pride, like past tyrants".

- Khamenei calls on the Iranian youth to "Maintain your unity. Maintain unity; a unified nation will overcome any enemy.” Khamenei: "America's hands are stained with the blood of more than 1,000 Iranians, including leaders and innocent people. Iran is steadfast and will not back down one iota from its principles."

- The situation remains an extremely complex domestic and international political web.

- Internally, the protests stem from a number of issues. For some, it is anger over the state of the economy amid high inflation, goods shortages, and the collapse of the rial currency. In some regions, the perceived persecution of Kurdish, Azeri and Lor ethic minorities is another spark for protests. For a section of society, there is the long-held desire to see the return of the Iranian monarchy under the late Shah's son, Crown Prince Reza Pahlavai. Then there is what appears to be the largest segment of the protesters, those who oppose the hardline, theocratic and authoritarian nature of the Khamenei regime.

Internationally, the Israeli gov't has reportedly stressed that it does not intend to exploit the current unrest, with PM Benjamin Netanyahu asking Russian President Vladimir Putin to relay the message that Israel does not seek war with Iran amid concerns over a preemptive strike from Tehran. Netanyahu did say to the Knesset earlier in the week that “We may be standing at a decisive moment in which the Iranian people will take their fate into their own hands.”

- As noted earlier (IRAN: Supreme Leader To Deliver Speech On Protests Shortly-State TV), Trump has threatened "there will be hell to pay" if the regime engages in a violent crackdown on protesters. It remains to be seen what this threat entails, and indeed, the willingness of the Trump administration to open up another international flashpoint amid global focus on US operations in Venezuela, concerns in Europe regarding the future of Greenland, and ongoing efforts among Ukraine and its allies to secure continued US support for Kyiv.

- However, following the operation in Venezuela, as well as US airstrikes in Nigeria and its seizure of a sanctioned oil tanker supposedly being protected by Russian naval vessels, the Trump White House has shown in recent weeks its clear willingness to forgo usual diplomatic channels and act unilaterally and swiftly if it sees fit.

- Amid protests in Iran, there is also usually a focus on the possible actions of the Middle East's powerful Gulf nations, especially Saudi Arabia. Despite a Chinese-brokered rapprochement between Riyadh and Tehran in recent years, the region's Sunni and Shia power centres still view one another as strategic competitors.

- However, at present, Saudi foreign policy focus is directed southward towards Yemen amid the dissolution of the UAE-backed Southern Transitional Council, potentially providing Saudi Arabia with a significant opportunity for the Presidential Leadership Council that it has backed in the Yemeni civil war for more than a decade.

EUROPE ISSUANCE UPDATE:

GILT SYNDICATION: 5.25% Jan-41 gilt chosen for Jan syndication - as expected

- The DMO has announced the gilt for the long syndication to be held in the W/C 19 January will be the 5.25% Jan-41 gilt (ISIN: GB00BVP99897).

- This is in line with our expectations, and we have been noting since the Budget that we would be very surprised if any other gilt was on offer. This was even more the case when it was not chosen to be reopened via auction this quarter.

FOREX: USD Index Extends Solid Bounce from December Lows

- USD: FX markets have been characterised by a more constructive US dollar tone to start the year, which has helped the USD index extend the recovery from the December lows to around 1.35%. The DXY’s advance this morning has reached the 50% retracement of the Nov-Dec price swing, just above the 99.00 mark. Markets continue to weigh the ongoing geopolitical developments ahead of key US data later today and a potential Supreme Court ruling on the legality of the Trump tariffs.

- JPY: As noted, this has been led by USDJPY this morning, as broad-based weakness for the Japanese yen persists. BOJ rhetoric over the holiday period was hawkish at the margin, potentially keeping a lid on the depreciating trend. However, given the slow expected pace of BOJ rate hikes, real rates still in negative territory, and ongoing fiscal concerns related to the Takaichi administration, the path of least resistance remains clearly higher for USDJPY. Furthermore, stronger rhetoric on intervention would only become more likely with a move above key resistance at 158.00.

- EUR: EURUSD slipped below 1.1650 in late trade yesterday, extending the pull lower from the 1.1808 high in late December. Spot has moved below support at 1.1659, the Jan 5 low, cancelling a possible reversal signal on Jan 5 - a dragonfly doji candle pattern. For now, a bearish theme appears likely to dominate from a technical perspective.

- AUD: Elsewhere, both AUD and NZD have been slowly edging lower from the mid-week highs. For AUDUSD, weakness back below 0.67 appears corrective and this is allowing an overbought condition to unwind. Initial firm support lies at 0.6677, the 20- day EMA.

- CAD: This week’s extension higher in USDCAD has seen a key breach of 50-day EMA resistance, undermining the current bearish theme and signalling scope for a stronger short-term bull phase. The December 04 low at 1.3925 is the next topside level of note.

- CNH: The main exception to USD upside is USDCNH, which is holding just above 6.9800 in latest dealings (session lows were at 6.9757), after the USDCNY fixing set a fresh low since 2024 earlier. This is aiding CNH outperformance on key crosses and continues to provide a stable backdrop for the emerging market FX basket.

FOREX: USDJPY Approaches Key Resistance Ahead of Key US Data

- Ahead of December NFP, the USD index extends its recovery from the December lows to 1.35%. USDJPY has narrowed the gap substantially to key resistance at 157.89, as a BoJ sources report (said to weigh downgrade of CPI outlook) underpinned earlier strength. Japan FinMin Katayama has spoken about risks of China's export controls on global supply chains and called for smooth trade flows.

- Further strength would show JPY shorts have not surrendered after Katayama's recent FX jawboning, and would open up 158.87, the 2025 high.

- Scandinavian FX outperform after local data. Swedish monthly GDP was much stronger than expected, keeping momentum at a solid pace but a recovery in economic activity is not yet a definitively hawkish contributor to the Riksbank's policy considerations. The details of the Norway December inflation report meanwhile underscore Norges Bank's cautious stance, with services ex-rent and food inflation pressures noted. NOKSEK is roughly unchanged on the session after piercing resistance at the 20-day EMA of 0.9167.

- NZDUSD (-0.4%) meanwhile extends its recent pullback, breaking below 0.5736 support, the Dec 19 low. The next level to watch will be 0.5711, the Dec 2 low. Meanwhile, AUDUSD weakness back below 0.67 appears corrective, allowing an overbought condition to unwind

- December payrolls data will carry more signal to the market and Fed than the highly unusual November report, being the last NFPs before the FOMC's Jan meeting. Participants would probably require substantially weaker-than-expected NFPs to spur even consideration of another cut. A Supreme Court ruling on the legality of the Trump tariffs could also come as early as today.

- Elsewhere, ECB's Lane will likely repeat that rates are in a "good place", while the Fed's Kashkari, Bostic and Barkin are also scheduled to appear.

OPTIONS: Expiries for Jan09 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1500(E5.3bln), $1.1600(E1.0bln), $1.1750(E652mln), $1.1785(E984mln), $1.1800(E2.3bln)

- USD/JPY: Y158.00($773mln)

- GBP/USD: $1.3350(Gbp512mln)

- AUD/USD: $0.6680-90(A$804mln)

- USD/CAD: C$1.3800($764mln), C$1.3835($514mln), C$1.3880($671mln), C$1.3900($548mln)

- USD/CNY: Cny7.0250($600mln)

EQUITIES: E-Mini S&P Continues to Trade Just Below Key Resistance

- A bull cycle in Eurostoxx 50 futures remains intact and the contract is holding on to the bulk of its latest gains. The move higher this week confirms a resumption of the primary uptrend. Note too that moving average studies are in a bull-mode position, highlighting a dominant uptrend. Sights are on the 6000.00 handle next. On the downside, initial firm support to watch is 5819.97, the 20-day EMA. A pullback would be considered corrective.

- The trend condition in S&P E-Minis is unchanged, it remains bullish and price continues to trade above key near-term support at 6771.50, the Dec 18 low. Clearance of this level is required to signal scope for a deeper retracement and would also highlight a possible short-term reversal. For bulls, sights are on key resistance at 7014.00, the Oct 30 high. A move through this hurdle would confirm a resumption of the primary uptrend.

COMMODITIES: Trend Structure in Gold Unchanged and Bullish

- The trend structure in WTI futures remains bearish and recent gains appear corrective. Moving average studies are in a bear-mode position, highlighting a dominant downtrend. Note that resistance at the 50-day EMA, at $58.29, has been pierced. A clear breach of the EMA would signal scope for a stronger corrective phase. Key resistance is at $61.25, the Oct 24 high. A resumption of the downtrend would open $53.77, a Fibonacci projection.

- The trend structure in Gold is unchanged, it remains bullish and a sharp sell-off late December appears to have been a correction The trend is overbought and any deeper retracement would allow this condition to unwind. First support at $4372.9, the 20-day EMA, has been pierced. A clear break of the average would expose the 50-day EMA at $4225.3. For bulls, a resumption of gains would open $4235.2, a Fibonacci projection.

| Date | GMT/Local | Impact | Country | Event |

| 09/01/2026 | 1200/0700 | ** | Brazil Final CPI | |

| 09/01/2026 | 1245/1345 | ECB Lane Keynote at Danish Economy Conference | ||

| 09/01/2026 | 1330/0830 | *** | Labour Force Survey | |

| 09/01/2026 | 1330/0830 | *** | Labour Force Survey | |

| 09/01/2026 | 1330/0830 | *** | Housing Starts | |

| 09/01/2026 | 1330/0830 | *** | Housing Starts | |

| 09/01/2026 | 1330/0830 | *** | Employment Report | |

| 09/01/2026 | 1330/0830 | *** | Employment Report | |

| 09/01/2026 | 1330/0830 | *** | Employment Report | |

| 09/01/2026 | 1330/0830 | *** | Employment Report | |

| 09/01/2026 | 1330/0830 | *** | Employment Report | |

| 09/01/2026 | 1330/0830 | *** | Employment Report | |

| 09/01/2026 | 1500/1000 | *** | U. Mich. Survey of Consumers | |

| 09/01/2026 | 1500/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 09/01/2026 | 1500/1000 | Minneapolis Fed's Neel Kashkari | ||

| 09/01/2026 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 09/01/2026 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 09/01/2026 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 09/01/2026 | 1835/1335 | Richmond Fed's Tom Barkin |