MNI Norges Bank Preview Mar 26 -The Question is: How Hawkish?

Mar-24 14:20By: Emil Lundh

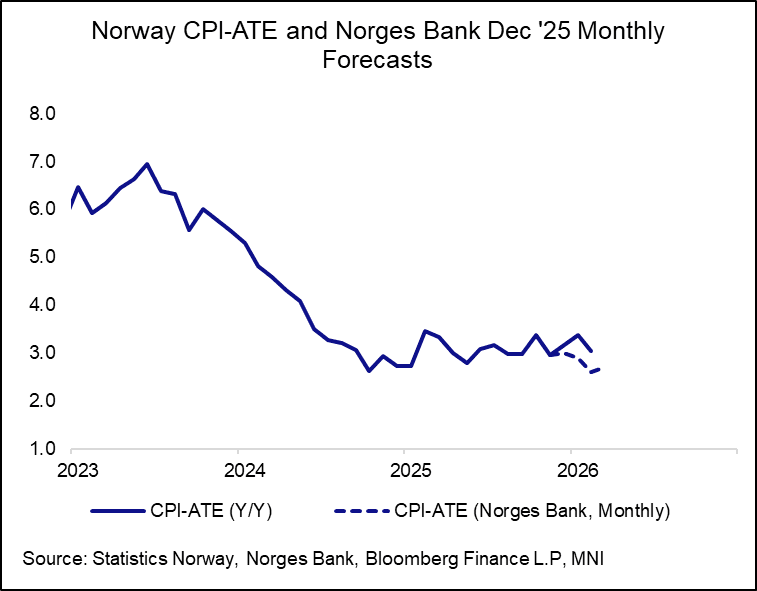

Norway

FOR THE FULL PUBLICATION PLEASE CLICK HERE

EXECUTIVE SUMMARY:

- Norges Bank is expected to hold the deposit rate at 4.00%, but the overall tone of the meeting is likely to be hawkish owing to a significant upward revision to the March MPR rate path projection. While we agree with consensus that a hold is the most likely outcome, a plausible tail risk is that the Board delivers a pre-emptive hike in March

- Expectations for a hawkish pivot had been cemented before the Iran war started, following the significantly higher than expected January inflation reading. Other domestic indicators also suggest the economy is not in need of further easing. Fallout from the Iran war has pushed up oil and gas prices and driven a sharp hawkish repricing in foreign rate expectations – these factors provide an additional hawkish impulse into Norges Bank’s rate path framework. The stronger exchange rate will provide a sole dovish offset, in our view.

The December MPR rate path was consistent with 2x25bp cuts this year, but Governor Wolden-Bache never endorsed this as a base case in her verbal communuications. Her annual address in mid-February also removed guidance that rates would likely be lowered during the course of 2026. We expect the March MPR rate path to fully remove implied cuts over the next 1-2 years, and embed a material implied probability of a hike in Q2/Q3. The policy statement is likely to stress heightened vigilance on inflation, and the potential for rate hikes to combat high domestic price growth. From mid-2027, we expect the rate projection to move lower again as implied hike pricing is unwound.