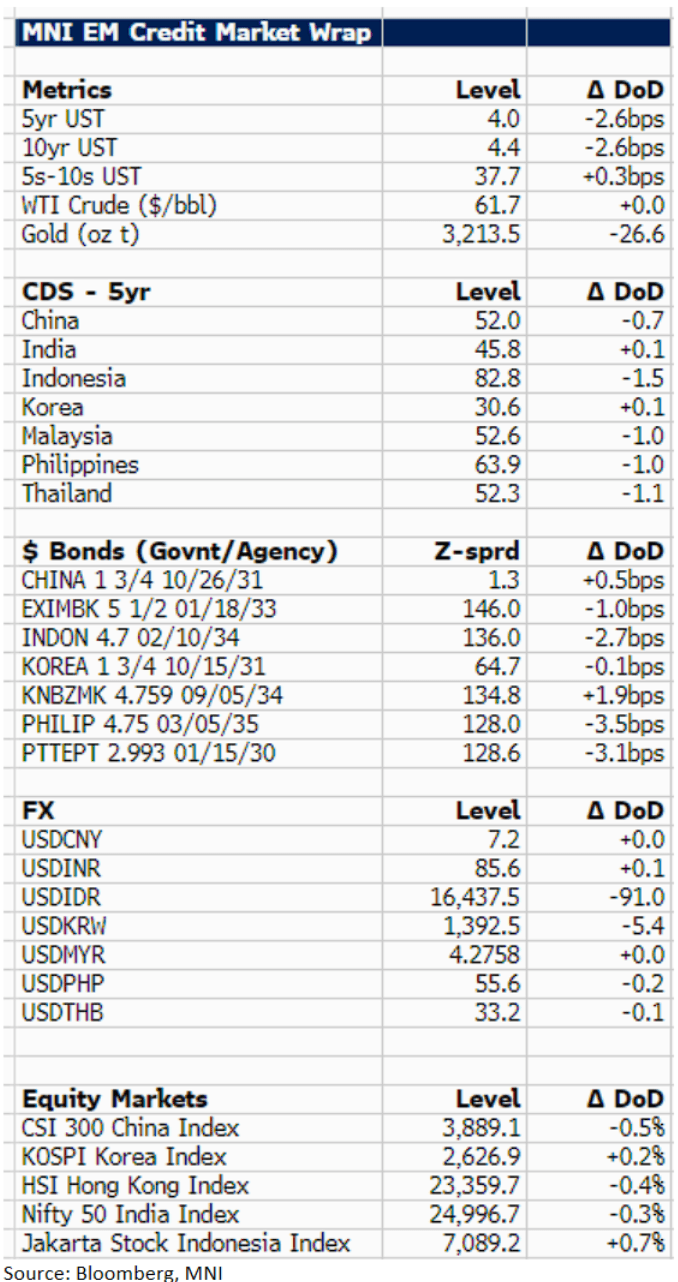

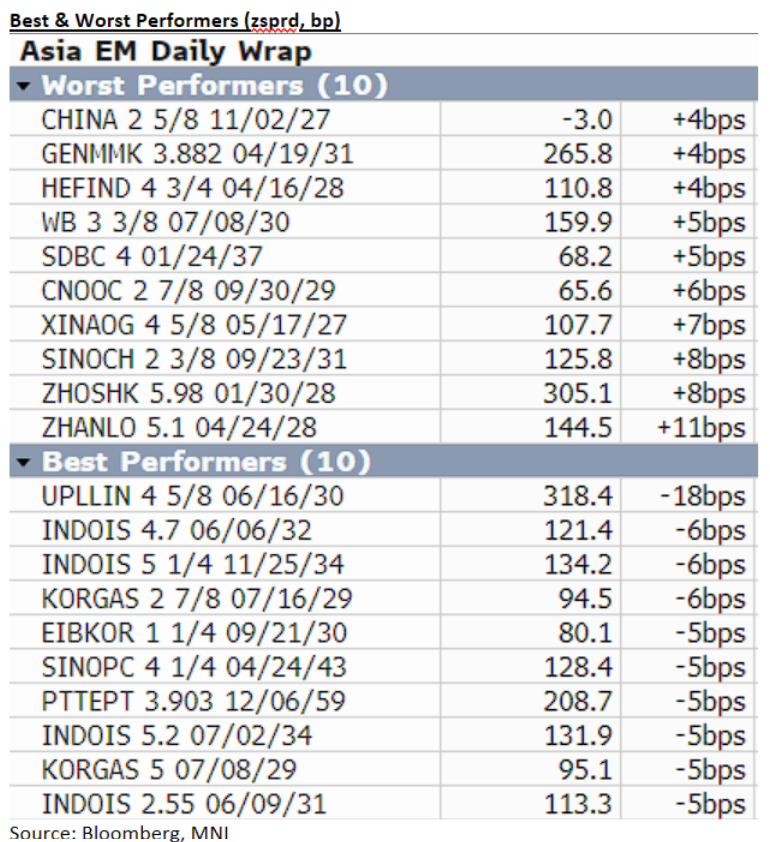

EM ASIA CREDIT: MNI EM Credit Market Update - Asia

U.S. 10y treasury yields are a 3bp tighter on the day at 4.4% and follows quite a bit of data out of the U.S. overnight with PPI lower than expected, while retail sales and weekly claims were in line. Asia EM credit is mostly better today with govie/agency $ spreads up to 3bp tighter, the Philippines (-3bp) and Thailand (-3bp) outperforming. Malaysia underperformed, with our $ proxy (KNBZMK 9/34), +2bp on the day. Malaysia released 1Q GDP numbers today (+4.4%), which were a bit weaker than consensus (+4.5%). Overall it was a relatively quiet session in the sovereign space. In terms of corporate newsflow, CATL has raised $4.6bn in its IPO, more than originally guided ($4bn), and Alibaba results were solid, neutral for spreads. No new issuance today. We did price the Shandong Gold overnight at a yield of 4.6%, our fair value estimate was 4.65%.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EGBS: Soft Risk Tone Prompts EGB Spread Widening, Issuance In Focus Today

This morning’s soft tone for risk assets sees 10-year EGB spreads to Bunds widen. The BTP/Bund spread is up 2bps to 120bps, but remains comfortably below last week’s ~126bp close following S&P’s rating upgrade after hours on Friday.

- Books are open for today’s dual tranche 7-year BTP / 30-year BTPei syndication. We pencil in a wide E7-13bln range for the 7-year size, while the 30-year is a E3bln WNG.

- Italian PM Meloni will meet with US President Trump on Thursday, in an attempt to negotiate some tariff reprieve for the EU (including Italy’s export-dependent manufacturing sector). Bloomberg reported yesterday that little progress has been made between the EU and the US at present.

- GGBs underperform for the second consecutive session, with spreads 3bps wider at 90.5bps (though still well shy of last week’s 100bp extreme).

- Greece will sell E200mln of the 3.875% Mar-29 GGB this morning (bidding deadline 1000BST/1100CET).

- In France, state audit chief Moscovici and Finance Minister Lombard appear before the National Assembly’s finance committee. Lombard said over the weekend that E40bln of savings are needed to meet the 2026 budget deficit target of 4.6% GDP. The OAT/Bund spread is 1bp wider at 76.5bps at typing.

GILTS: Futures Through Next Resistance, Tighter Vs. Bunds After CPI

The combination of broader risk-off price action (trade war- and European earnings-driven) and softer-than-expected UK CPI data (albeit with the headline reading matching the median of sell-side analysts that we read) drives a rally in gilts.

- Futures trade as high as 92.32, breaching the next resistance level at the 50.0% retracement of the April 7-9 sell off (92.24), before a fade back to ~92.15. Our technical analyst notes that the bearish threat in the contract remains intact.

- Yields ~4-6bp lower across the curve, flattening seen, 10s outperform.

- 10s ~2bp tighter vs. Bunds, continuing to reverse some of last week’s notable spread widening.

- SONIA futures and BoE-dated OIS roughly in line with levels we flagged ahead of the gilt open, showing ~85bp of cuts through year end vs. ~81.5bp late yesterday.

- Eyes on macro/cross-market cues for much of the day, with comments from Fed Chair Powell & U.S. retail sales data headlining the global calendar.

- On the supply front, the DMO will conduct a tender of GBP1.5bln of the 0.125% Jan-28 gilt this morning.

JPY: USDJPY is eyeing the April low, lowest since September

- Watch the USDJPY here, as just noted in the Gold comment, CHF and JPY are extending gains, the USDJPY is eyeing the April low of 142.07 (prices are according to Bloomberg), its lowest level since late September.

- A clear break through 142.00 {USDJPY Curncy} opens to 141.66 next.