- Despite a relatively calm start to the week from an event risk perspective, the US dollar is trading on the back foot Monday. Strong performance for the major equity benchmarks on US/China optimism has been weighing, while the more activist approach to Fed personnel management from the White House may be providing an additional greenback headwind.

- The USD index sits 0.25% lower on the session in sympathy, with broad based associated strength for the rest of the G10. GBP moderately outperforms, while AUD has also extended its recent momentum.

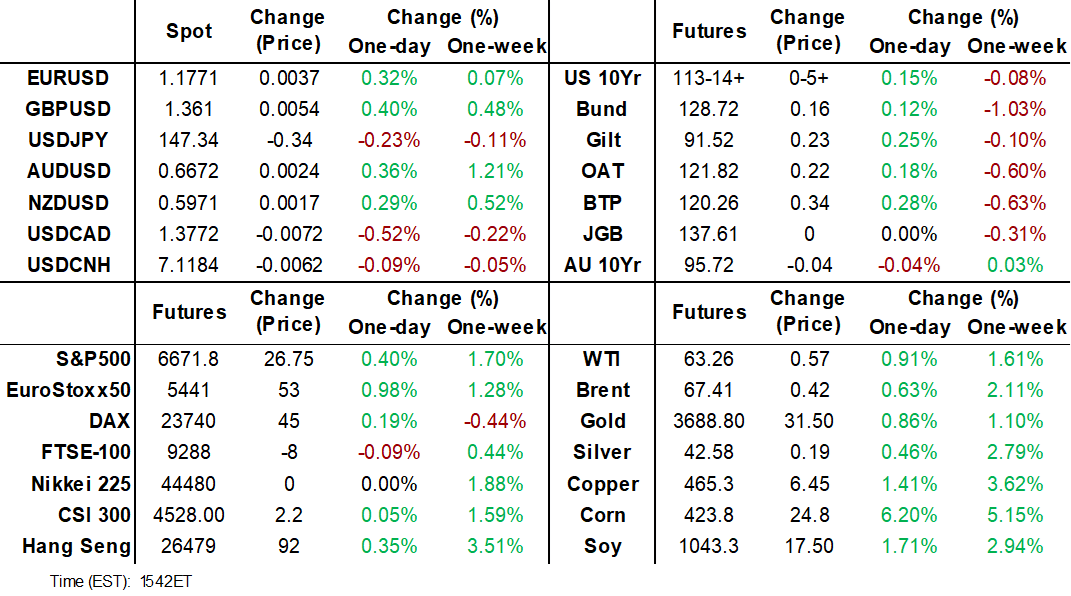

- Bullish conditions for GBPUSD have been bolstered this morning, following the break of the bull trigger located at 1.3595 (Aug 14 high) which places the pair at two-month highs and suggests the corrective cycle between Aug 14 - Sep 3 is over. Immediate resistance is found at 1.3636, the 76.4% retracement of the Jul 1 - Aug 1 downleg, before 1.3681, the Jul 4 high. UK labour market data kicks off Tuesday’s calendar, before UK CI and the BOE decision later this week.

- For AUDUSD, today’s 0.3% advance prompted fresh cycle highs for the pair at 0.6672. Last week’s gains plus the breach of the bull trigger at 0.6625 confirmed a resumption of the technical uptrend, and the pair has narrowed the gap substantially to the US election related highs at 0.6688. RBA Assistant Governor and chief economist Hunter will speak in a fireside chat Tuesday.

- SEK also outperforms the G10 basket, supported by the aforementioned drivers. However, there may also be some spillover from Riksbank Governor Thedeen's recent interview with Dagens Industri, which cements next week's central bank decision as a very close call between a cut and a hold.

- Aside from UK data, German ZEW will cross during the European morning on Tuesday. Focus then shifts to US retail sales and Canadian CPI as notable data prints before the plethora of central bank decisions later in the week.

MNI ASIA MARKETS ANALYSIS - All Time Highs For Stocks & Gold

Sep-15 19:46By: Chris Harrison

APAC

HIGHLIGHTS

- US equity futures and spot gold both hit fresh all-time highs

- USD grinds lower ahead whilst Treasuries rally amidst light volumes ahead of a busy economic calendar

- Ahead, CEA's Miran Senate confirmation vote at ~2000ET (expected to pass) and a possible Trump-Cook ruling

- Beyond that, focus turns to UK labour data before US retail sales and Canadian CPI

- The FOMC decision, with a cut fully priced and an eagerly anticipated new dot plot, looms large on Wednesday

US TSYS: Modest Earlier Rally Consolidated Under Lights Volumes

- Treasuries are holding onto a rally that came earlier in the session, with the wings lagging.

- There was little in the way of meaningful fresh drivers but with pre-FOMC positioning and Trump’s continued call for rate cuts (“bigger” than Powell “had in mind”) possibly at play.

- The move started beforehand but won’t have been hindered by a soft Empire manufacturing survey which saw new orders fall 35 points to their lowest since Apr 2024.

- Cash yields are 2.3-3.3bp lower on the day.

- TYZ5 trades at 113-14+ (+05+) having established gains early in the US session, on tepid cumulative volumes of 905k.

- Resistance is seen at 113-29 (Sep 5 high) with a bullish trend sequence intact, whilst support is seen at 112-23+ (20-day EMA).

- J.P.Morgan recommended adding shorts in 10s late on Friday. They "think the decline in long-term yields has been overdone, and we recommend tactically fading the move for a number of reasons.” That includes seeing a soft floor on 10Y yields at 4% in the near-term, the sector appearing significantly rich relative to the wings and there’s scope for “both higher medium-term growth expectations and wider TIPS breakevens”.

- Goldman Sachs in contrast "for now, the belly richness will be difficult to unseat given its low vol/carry friendly properties but can underperform in the tails. We continue to think that meaningfully lower yields from here rely on labor market news more convincingly opening up left tail worries".

- Miran vote and Cook suit headlines are still to come before tomorrow sees retail sales and import prices for August in focus, all ahead of the FOMC decision on Wednesday.

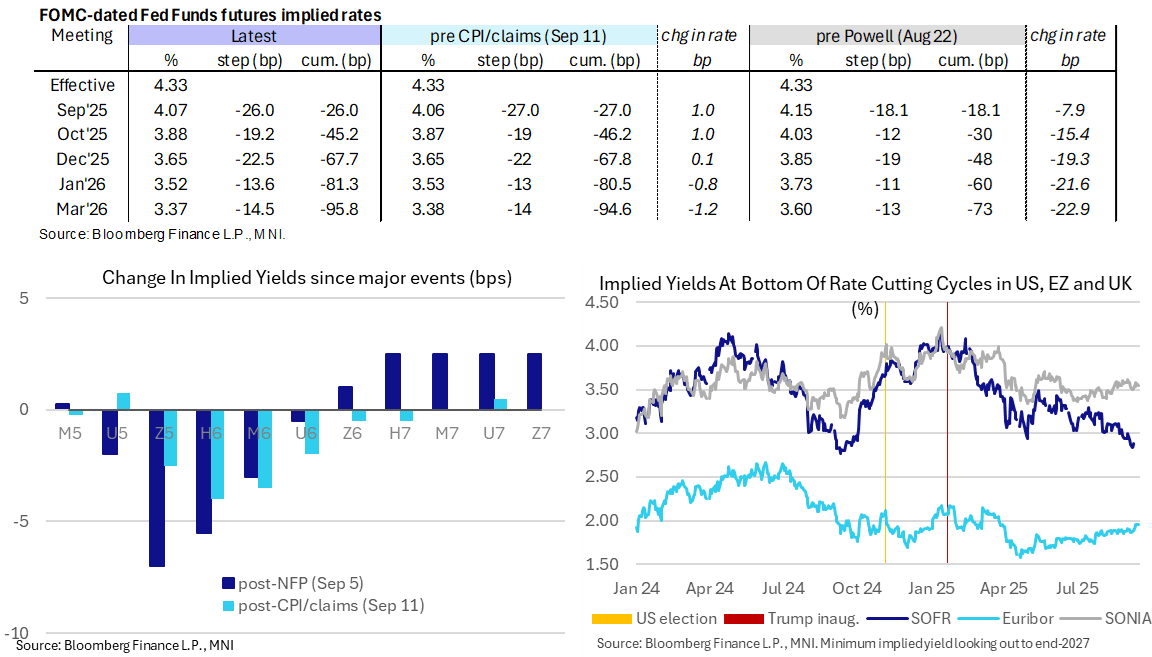

US STIR: Dec 2025 Fed Funds Implied Rate Almost Fully Reverses Claims Hit

- Fed Funds implied rates see the Dec’25 lead today’s increase, currently 2bp higher from Friday’s close to have almost fully reversed Thursday’s drop seen on a surprise uptick in initial jobless claims along with the broader US CPI report.

- It’s likely a positioning play, with the sole data being a surprisingly weak Empire manufacturing report.

- Cumulative cuts from 4.33% effective: 26bp for Wed, 46bp Oct, 68bp Dec, 81.5bp Jan and 95.5bp Mar.

- SOFR futures hold the session’s twist flattening, with U5 and Z5 1 tick lower vs gains of up to 2.5 ticks in U6 and Z6.

- The SOFR implied terminal yield of 2.915% (SFRH7, -1.5bp) meanwhile is unchanged from when US desks filtered in. It remains off last Monday's close of 2.84% (lowest since Sep 2024 and one of the lowest for the cycle) but still points to more than 140bp of cuts ahead.

- Still to come, Miran’s Senate confirmation vote (expected to pass having already passed the Banking Committee 13-11). The cloture vote is at ~1730ET before the full confirmation vote ~2000ET.

- We also expect at some point to hear a ruling in the ongoing Trump-Cook case on whether the court will grant a stay on the decision that allowed Cook to remain in her job for now (and thus attend this week’s FOMC meeting starting tomorrow before the decision on Wed).

FX: US Dollar Grinding Lower Ahead of Busy Economic Calendar

US STOCKS: Indices Inch Off All-Time Highs, Alphabet Joins The $3tn Club

- ESZ5 at 6671.25 (+0.4%) is holding onto solid gains for the day having eased only slightly off fresh all-time highs of 6681.25, with gains at the time extended by Trump suggesting a move to semi-annual reporting for corporates.

- Next resistance is seen at 6685.25 (1.00 proj of Aug 1-15-20 price swing) after which lies the round 6700. Support meanwhile isn’t seen until 6546 (20-day EMA).

- Some of the large idiosyncratic moves at play have been pared, with gains becoming a little more broad-based compared to two hours ago. That includes Tesla (+3.0%, gains pared having been 7.5% at one point) after Musk bought ~$1bn of shares, Alphabet (+3.4%) extending trend gains after a recent antitrust ruling with it today becoming the fourth company with a market cap in excess of $3trn and Oracle (+2.1%) attributed to data center construction expectations along with Seagate Technology up 7.2%. Other notable gains include Amazon (+1.5%) and Apple (+0.9%).

- Nvidia is back in the red (-0.4%) having clawed back to flat after receiving an intraday boost following a lack of fresh headlines at the China trade delegation press conference after Bessent-He talks. It had dragged pre-market and earlier in the session after China said it violated antitrust regulations with its acquisition of Mellanox.

- Leaders: Communication services (+2.0%), consumer discretionary (+0.9%) and IT (+0.6%).

- Laggards: Consumer staples (-1.0%), health care (-0.9%) and materials (-0.8%).

- The tech-heavy nature of day’s gains unsurprisingly sees NDQ outperform at +0.7% (20 pts off earlier all-time highs of 24274.80). The Russell 2000 also performs well (+0.4%) whilst the Dow Jones lags (+0.1%).

COMMODITIES: Gold Hits Fresh All-Time High, WTI Crude Climbs

- Gold has rallied to a fresh all-time high on Monday amid broad dollar weakness ahead of Wednesday's FOMC meeting, when a 25bp rate cut is widely expected. Bullion may also be benefitting from continued Fed independence concerns after President Trump called again for rates to be cut.

- Spot gold has risen by a further 1.0% to $3,680.2/oz at typing (off a new high of $3,685.6), taking total gains this month to almost 6%.

- Gold remains in a clear bull cycle, with the break higher confirming a resumption of the primary uptrend. Above here, attention turns to round number resistance at the $3,700 handle, followed by $3,716.5, a Fibonacci projection.

- Similarly, silver has also rallied by 0.9% to $42.6/oz.

- Trend signals in silver remain bullish, with today’s move piercing resistance at $42.606, a Fibonacci projection. Above here, next resistance is seen at $42.974, the 2.382 projection of the Jul 31 - Aug 14 - 20 price swing, followed by $43.000 round number resistance.

- Meanwhile, WTI crude is also trading higher, with the market weighing the impacts of further Ukrainian drone attacks on Russian energy infrastructure.

- WTI Oct 25 is up by 0.9% at $63.3/bbl.

- Despite the move, a bear cycle in WTI futures remains intact and short-term gains are considered corrective.

- Initial resistance to watch is $66.03, the Sep 2 high. Initial support is at $61.29, the Aug 13 low and the bear trigger.

MNI Reports

MNI FED PREVIEW: A Reluctant Return To Easing

The Federal Reserve is set to resume its easing cycle at the September 16-17 meeting with a 25bp cut to the funds rate range to 4.00-4.25%. The decision to cut after a 5-meeting pause was well-telegraphed by Chair Powell, whose Jackson Hole speech described a “shifting balance of risks” toward a weaker labor market that “may warrant adjusting our policy stance”. The updated quarterly projections aren’t likely to bring many changes to the macroeconomic variables, but as usual the signal sent from the Fed rate “Dot Plot” will garner attention. A Committee split between expecting one or two further cuts this year is likely, keeping each of the remaining meetings of 2025 “live”.

MNI NORGES BANK PREVIEW: Another Close Call

At the start of the month, analyst and market expectations were fairly comfortably in favour of a 25bp Norges Bank cut on September 18th. However, domestic data released over the past two weeks have made the decision a much closer call. We currently lean against consensus in favour of a hold at 4.25% - a risk we thought markets were underappreciating even before the recent run of domestic data.

MNI UK DATA PREVIEW: September 2025 CPI and Labour Release

Both labour market data and CPI data will have already been released to MPC members this morning, and both data releases are important for future monetary policy despite markets pricing in only around a 1/3 probability of a rate cut this year (and not fully pricing a 25bp cut until April 2026). We think that both Governor Bailey and Deputy Governor Ramsden are very much focused on the labour market print (probably a little more so than inflation). Along with Breeden, all three members are likely needed on board in order for another rate cut this year to materialize. We think that the market focus will switch back to AWE private regular pay data. Both the median and mean estimate from the previews that we have read is that this will fall to 4.65%Y/Y in the 3-months to July.

CANADA (MNI): Headline CPI Seen Higher Y/Y, But Core Measures Steadying Out (1/3)

August's inflation report is expected to show a slight pickup in headline CPI vs July when measured on a Y/Y basis, but flat on a sequential non-seasonally-adjusted basis. More importantly the Bank of Canada's preferred measures of core inflation are seen remaining steady, with risks perceived to be slightly to the downside.

CANADA (MNI): Core Goods, Non-Shelter Services Eyed (2/3)

Core goods are seen remaining relatively steady, having printed 2.0% Y/Y in both June and July in a steadying out after a 1.1pp rise in the previous 2 months.

CANADA (MNI): Analysts Unsure CPI Would Impact BOC Decision (3/3)

Some analyst expectations for the August inflation report. While analysts aren't convinced that the report will have much bearing on the BOC decision on Wednesday, due in large part to the fact that the rate deliberations will have all but concluded by Tuesday, a few have noted that there may be an impact if there is a significant surprise.

Upcoming Data and Events Calendar

| Date | GMT/Local | Impact | Country | Event |

| 16/09/2025 | 0600/0700 | *** | Labour Market - AWE & Unemployment | |

| 16/09/2025 | 0600/0700 | *** | Labour Market - Payrolls & Claimants | |

| 16/09/2025 | 0800/1000 | *** | HICP (f) | |

| 16/09/2025 | 0900/1100 | *** | ZEW Current Expectations Index | |

| 16/09/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 16/09/2025 | 0900/1100 | ** | EZ Industrial Production | |

| 16/09/2025 | 1215/0815 | ** | CMHC Housing Starts | |

| 16/09/2025 | 1230/0830 | *** | CPI | |

| 16/09/2025 | 1230/0830 | *** | Retail Sales | |

| 16/09/2025 | 1230/0830 | ** | Import/Export Price Index | |

| 16/09/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 16/09/2025 | 1315/0915 | *** | Industrial Production | |

| 16/09/2025 | 1400/1000 | * | Business Inventories | |

| 16/09/2025 | 1400/1000 | ** | NAHB Home Builder Index | |

| 16/09/2025 | 1700/1300 | ** | US Treasury Auction Result for 20 Year Bond | |

| 17/09/2025 | 0600/0800 | ** | Unemployment | |

| 17/09/2025 | 0600/0700 | *** | Consumer inflation report | |

| 17/09/2025 | 0730/0930 | ECB Lagarde at ECB Annual Research Conference | ||

| 17/09/2025 | 0800/1000 | ECB Cipollone At Associazione Bancaria Italiana EC Meeting | ||

| 17/09/2025 | 0900/1100 | *** | EZ HICP Final | |

| 17/09/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 17/09/2025 | 1115/1315 | ECB Cipollone Speaks at Netherlands Central Bank Resilience Conference | ||

| 17/09/2025 | 1230/0830 | * | International Canadian Transaction in Securities | |

| 17/09/2025 | 1230/0830 | *** | Housing Starts | |

| 17/09/2025 | 1345/0945 | *** | Bank of Canada Policy Decision | |

| 17/09/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 17/09/2025 | 1430/1030 | BOC press conference | ||

| 17/09/2025 | 1430/1030 | ** | US DOE Petroleum Supply | |

| 17/09/2025 | 1800/1400 | *** | FOMC Statement | |

| 18/09/2025 | 2245/1045 | *** | GDP |