CHINA: Key Local News Highlights - PPI Highest in 4-Years

Below is a selection of key recent onshore media highlights for China ICYMI :

Growth (Xinhua): China sees consumption recovery, robust growth in emerging industries

https://english.news.cn/20260609/0658ba9dcf2044be9b4761180657deec/c.html

Trade (Yicai): China’s Trade Beats Forecasts Again in May on Global AI Investment Boom

Economic Outlook (Yicai): Yicai Chief Economists Confidence Index Falls to 49.9 Amid Cautious Economic Outlook

China EU Relations (Global Times): China, EU to discuss establishing trade and investment consultation mechanism: source

https://www.globaltimes.cn/page/202606/1363052.shtml

China Brazil Relations (Global Times): China, Brazil commit to deepening financial cooperation

https://www.globaltimes.cn/page/202606/1363149.shtml

Trade (China Securities Network); Foreign trade grew by 15.3% in the first five months, showing a positive trend.

https://www.cs.com.cn/xwzx/01/2026/06/10/detail_2026061010017162.html

China's 15th Five-Year Plan (China Daily): Next leap for industrial system

https://www.chinadaily.com.cn/a/202606/10/WS6a289651a310d6866eb4d521.html

Trade (China Daily): Demand, policies fuel foreign trade

https://www.chinadaily.com.cn/a/202606/10/WS6a289d0aa310d6866eb4d54c.html

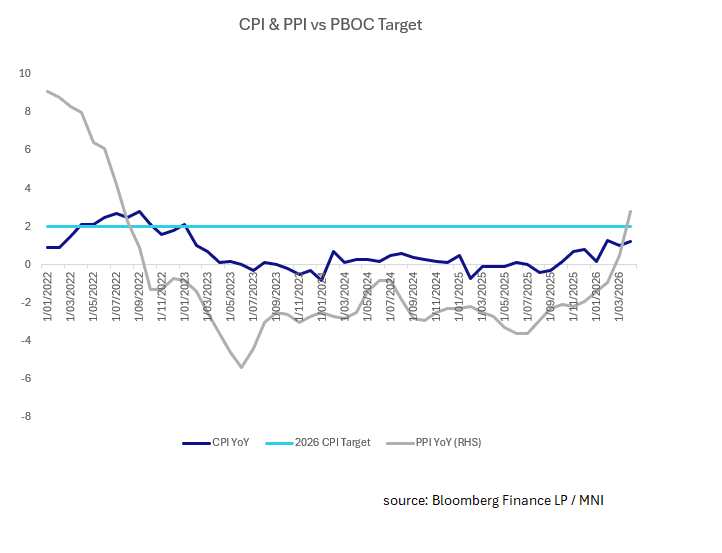

PPI (RTRS): China's May producer inflation highest in nearly 4 years, consumer prices also rise

PPI (CNBC): China May wholesale inflation hits near 4-year high on Iran war, AI costs; CPI misses

MNI China Press Digest June 10: Trade, Stablecoins, LNG Ships

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSTRALIA: Higher Commodity Prices Likely To Drive Better Deficit Profile

The Federal budget for FY27 is announced on Tuesday 12 May with expected improvements in the deficit forecasts due to higher commodity prices. There have been headlines around what it will include and how it is likely to work against the RBA's goals of reducing demand and inflation. According to local press reports, it will contain plans to increase defence & health spending, increase business tax relief, and change disability spending, capital gains tax and negative gearing.

- Governor Bullock said following the May decision to hike that capacity pressures mean that governments should be thinking about not adding to them and thus inflation and that help for households “makes it harder to dampen demand”.

- Given concerns about inflationary pressures, an income-tax offset is likely to be delayed until 2027 but announced in this budget. The drop in fuel excise on April 1 should weigh on tax revenue estimates.

- Westpac estimates that the budget position may improve around $27bn over the four years to FY29 mainly due to higher commodity prices. Higher global energy prices have boosted the petroleum resource rent tax intake. New policies could add $2bn to the deficit to FY29.

- Tax increases are likely to include the 50% capital gains tax discount replaced by inflation indexation for all asset classes. Negative gearing will only be allowed for new homes built and family trust distributions will be taxed at a flat 30%.

- There was speculation that a gas export tax would be introduced but the PM has denied those reports.

- $3bn is to be saved by reducing the private health rebate for over 65s.

- According to The Australian, the R&D tax credit cap will rise to $150mn and the SME asset write off will become permanent and businesses will be able to offset losses against the previous year’s profit.

CHINA: PPI Confirms Structural Shift Towards Reflation

China's April CPI and PPI data shows China's exit from factory-gate deflation is looking like a structural shift toward reflation.

After snapping 41 consecutive months of decline in March rising +0.5%, April PPI topped forecasts at +2.8% YoY. Factory-gate prices have been bolstered by surging global energy costs and the government's "anti-involution" policies designed to curb destructive price competition. This was the highest print since July 2022 and feeds into the narrative around ongoing improvements in industrial margins - which may provide a tailwain for the CSI 300 industrials and materials sector in Q3.

April CPI topped forecasts of +0.9% to rise +1.2% YoY (from prior month's 1.0%) with core prices up 1.2% YoY also.

For markets, the PPI beat suggests that China's economy is now providing modest inflationary pulses to the region rather than deflationary pressures - a note of caution for bond investors.

This data is consistent with the PBOC's current liquidity approach which suggests that not only is there is limited need for significant liquidity injections, but also that the remaining hopes for rate cuts has faded. Look for bond yields this week to potentially drift modestly higher.

MNI: CHINA APR CPI +1.2% Y/Y VS MEDIAN +0.8%; MAR +1.0%: NBS

- CHINA APR CPI +1.2% Y/Y VS MEDIAN +0.8%; MAR +1.0%: NBS

- CHINA APR CPI +0.3% M/M VS -0.7% M/M MAR

- CHINA APR FOOD PRICES -1.6% Y/Y VS +0.3% Y/Y MAR

- CHINA APR NON-FOOD PRICES +1.8% Y/Y VS +1.2% Y/Y MAR

- CHINA APR PPI +2.8% Y/Y VS MEDIAN +1.8%; MAR +0.5%: NBS

- CHINA APR PPI +1.7% M/M VS +1.0% M/M MAR