EU CONSUMER STAPLES: Keurig Dr Pepper: Fitch on Updated Financing

Nov-21 12:18

(KDP/pro-forma: Baa1*-/BBB*-/exp. BBB-)

(JDEPNA; Baa3/BBB-/BBB)

Still expects BBB- stable at close as it sees updated financing reducing leverage by 0.25x to 5.2x at close. The treatment of the $7b package and associated limited deleveraging is in-line with S&P (-0.3x) and Moody's comments.

- $3b in preferred stock will be given 50% equity credit

- $4b JV (KDP to hold 51%) is treated as full equity but with cash distributions taken out of earnings (capped at $255m/yr (6.375%) over first 5 years)

- Notes company targets for each standalone entity is 0.4-0.5x lower than at close and may require more active deleveraging (company has flagged asset sales as potential).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSY FUTURES: BLOCK: Dec'25 30Y Ultra Bond Buy

Oct-22 12:13

- +1,500 WNZ5 124-08, buy through 124-07 post time offer at 0801:34ET, DV01 $290,700.

- The 30Y ultra contract trades 124-03 last (+10) after climbing to 124-10 high recently

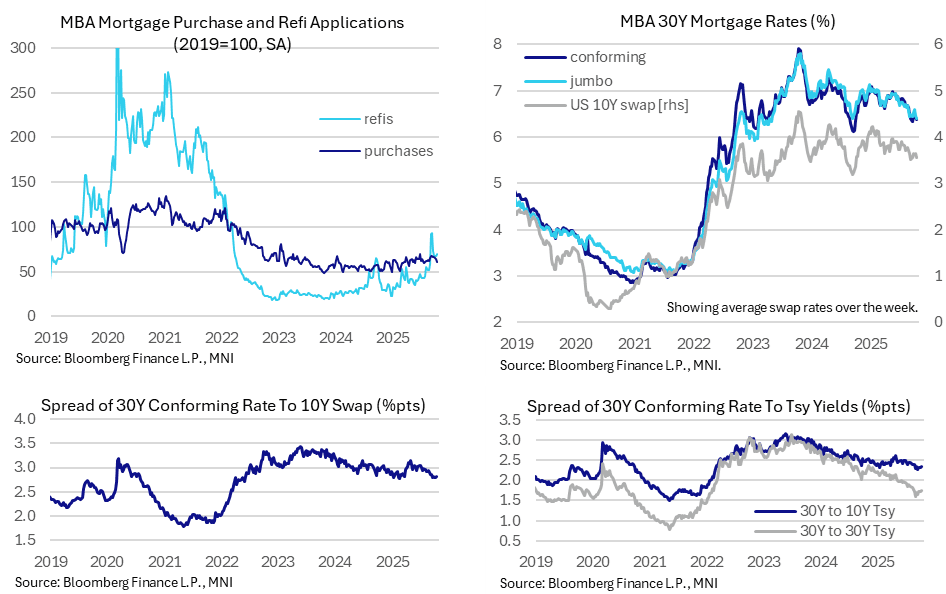

US DATA: Purchase Mortgage Applications Fall By Most Since July

Oct-22 12:13

MBA mortgage applications were little changed last week, with a lift in refis offsetting a sizeable drop in new purchase applications. Mortgage rate spreads ticked higher after declines had slowed in recent weeks, offering a diminished tailwind for applications.

- MBA composite mortgage applications dipped -0.3% (sa) last week, essentially unchanged having fallen a cumulative 19% since late September after a refi-driven 42% jump in the first half of September.

- There were conflicting drivers on the week, with new purchases sliding -5.2% (the largest drop since late July) vs refis increasing 4.0% (largest increase since mid-Sept).

- For context, composite applications are at 67% of 2019 levels, with 61% for new purchases (a recent high of 67%) and 70% for refis (recent high of 93%).

- The 30Y conforming mortgage rate eased another 5bps to 6.37%, close to the 6.34% in mid-Sept at what was the lowest since Sep 2024 on Fed easing expectations at the time.

- The 30Y jumbo rate meanwhile dipped 8bps to 6.39%, taking the two rates back close to each other after some disjointed weekly moves saw the jumbo rate trade as much as 17bp higher in early October for its most in nearly a year.

- Mortgage spreads were little changed to swaps but widened a touch to Treasury yields, in the past an area Bessent has wanted to see them lower. The 30Y mortgage rate to 10Y swaps held around 280bps, below the 300+/-5bp seen for some time since reciprocal tariff announcements in April and below the 285bp averaged in Q1. The 30Y to 10Y Tsy yield spread meanwhile lifted ~5bps to 235bps for its highest since August but remains close to lows since Mar 2022.

SOFR OPTIONS: BLOCK/Screen Update: Mar'26 SOFR Put Spread Buy

Oct-22 12:07

- Total 30,500 SFRH6 96.31/96.37 put spds, 1.5 vs. 96.625 to -.64/0.06%