NORWAY: June CPI: Surprise Unlikely To Shift Norges Bank Cut Expectations

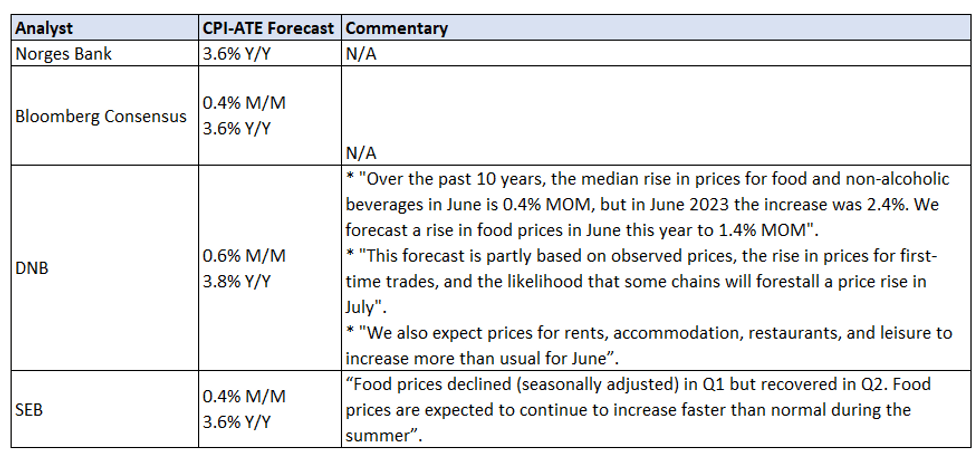

Norwegian June inflation is due at 07:00BST / 8:00CET. Consensus and the Norges Bank see CPI-ATE at 3.6% Y/Y (vs 4.1% prior).

- Following the more hawkish than expected June Norges Bank decision, current consensus is split between a first rate cut in December ‘24 (which would be dovish relative to the Norges Bank’s June rate path) and March ‘25 (more consistent with the rate path).

- We think that any surprise to CPI-ATE this morning will need to be taken alongside the July inflation data (due August 9) before meaningfully altering market expectations for the first cut.

- Nonetheless, a higher-than-expected reading would see the 20-day EMA at 11.4373 in EURNOK as the first support, with initial resistance at 11.5679 (50% retracement of the May 1 – June 21 sell-off).

- Looking at the breakdown of the Bloomberg consensus, Danske Bank expect a 3.5% Y/Y CPI-ATE reading while Citi (3.7% Y/Y) and DNB (3.8% Y/Y) hold above-consensus views. See below for DNB and SEB’s commentary ahead of the release:

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EURGBP TECHS: Impulsive Break Lower

- RES 4: 0.8621 High May 9 and a key short-term resistance

- RES 3: 0.8593 1.0% 10-dma envelope

- RES 2: 0.8541 High May 31

- RES 1: 0.8525 20-day EMA

- PRICE: 0.8555 @ 06:48 BST Jun 10

- SUP 1: 0.8454 76.4% of the Mar 7 - Sep 26 ‘23 bull phase

- SUP 2: 0.8408 Low Aug 24 2023

- SUP 3: 0.8388 Low Aug 17 2022

- SUP 4: 0.8366 2.236 proj of the Apr 23 - 30 - May 9 price swing

EURGBP has started the week on a bearish note and has cleared support at 0.8484, the May 29 low and bear trigger. This confirms a resumption of the downtrend and signals scope for a continuation lower near-term. Sights are on 0.8408 next, the Aug 24 ‘23 low. 0.8453, the 76.4% retracement of the Mar 7 ‘22 - Sep 26 ‘22 bull cycle has been tested, a break would reinforce the bearish theme. Resistance is at 0.8525, the 20-day EMA.

EUROZONE T-BILL ISSUANCE: W/C June 10, 2024

Germany, France, Spain, Belgium and Italy are all due to sell bills this week. We expect issuance to be E22.2bln in first round operations, down from E24.1bln last week.

- This morning, Germany will look to sell E2bln of the 3-month Sep 18, 2024 bubill and E2bln of the 9-month Mar 19, 2025 bubill.

- This afternoon, France will come to the market to sell up to E7.5bln of 13/14/26/49-week BTFs. On offer will be E3.2-3.6bln of the new 13-week Sep 11, 2024 BTF, E0.2-0.6bln of the 14-week Sep 18, 2024 BTF, E1.4-1.8bln of the 26-week Dec 11, 2024 BTF and E1.1-1.5bln of the 49-week May 21, 2025 BTF.

- Tomorrow morning, Spain will look to sell the 3-month Sep 6, 2024 letras and the 9-month Mar 7, 2025 letras. Details on size to be confirmed today.

- Also tomorrow morning, Belgium will look to issue an indicative E1.2bln (E1.0-1.4bln) of the 11-month May 8, 2025 TC.

- Finally, on Wednesday, Italy will come to the market to sell E7.5bln of the new 12-month June 13, 2025 BOT.

For more on future auctions see the full MNI Eurozone/UK T-bill auction calendar here.

SCHATZ TECHS: (U4) Bearish Trend Structure

- RES 4: 105.625 High May 17

- RES 3: 105.572 76.4% retracement of the May 15 - 24 bear leg

- RES 2: 105.484 61.8% retracement of the May 15 - 24 bear leg

- RES 1: 105.460 High Jun 4 and key short-term resistance

- PRICE: 105.215 @ 06:15 BST Jun 10

- SUP 1: 105.175 Low Jun 7

- SUP 2: 105.110 Low May 24 and the bear trigger

- SUP 3: 105.000 Round number support

- SUP 4: 104.855 1.00 projection of the May 15 - 24 - Jun 4 price swing

The trend condition in Schatz futures remains bearish and recent short-term gains are considered corrective. Moving average studies are in a bear-mode set-up, highlighting bearish market sentiment. Resistance to watch is 105.460, the Jun 4 and 5 high. For bears, a continuation lower would refocus attention on key support and the bear trigger at 105.110, the May 24 low. A break would resume the downtrend.